When you own gold you're fighting every central bank in the world: Jim Rickards Gold is not money: Ben Shalom Bernanke, Federal Reserve Board of Governors Chairman

5 days ago saw the 150th year anniversary of an event so historic that a very select few even noticed: the birth of US fiat. Bloomberg was one of the few who commemorated the birth of modern US currency: “On April 2, 1862, the first greenback left the U.S. Treasury, marking the start of a new era in the American monetary system…. The greenbacks were originally intended to be a temporary emergency-financing measure. Almost bankrupt, the Treasury needed money to pay suppliers and troops. The plan was to print a limited supply of United States notes to meet the crisis and then have people convert the currency into Treasury bonds. But United States notes grew in popularity and continued to circulate.” The rest, as they say is history.

In the intervening 150 years, the greenback saw major transformations: from being issued by the Treasury and backed by gold, it is now printed, mostly in electronic form, by an entity that in its own words, is “set up similarly to private corporations, but operated in the public interest.” Of course, when said public interest is not the primary driver of operation, the entity, also known as the Federal Reserve is accountable to precisely nobody. Oh, and the fiat money, which is now just a balance sheet liability of a private corporation, and thus just a plug to the Fed’s deficit monetization efforts, is no longer backed by anything besides the “full faith and credit” of a country that is forced to fund more than half of its spending through debt issuance than tax revenues.

At the start of the Civil War, the U.S. didn’t have a national paper currency. Instead, the money supply consisted of U.S. coins and a collection of paper notes issued by private banks. Technically, the federal government began issuing its own paper currency in 1861. That year, the Lincoln administration issued $60 million in demand notes, a variant of a Treasury note that was redeemable “on demand” for gold coins at the Treasury or any sub-Treasury.

These notes were overshadowed in 1862 by the issue of $150 million in a new fiat currency officially known as United States notes and popularly known as greenbacks or legal tenders. By the end of the war, close to $450 million worth of greenbacks were in circulation.

The name greenbacks referred to the reverse of the notes, which were printed in green. The name legal-tender notes referred to the text that originally appeared on the back, which began, “This note is legal tender for all debts, public and private.” This provision made the currency a valid form of payment on par with gold and silver, which was a very controversial action at the time. It made the United States note a fiat currency — meaning its value was established by law alone and wasn’t based on some other unit of value, such as gold, silver or land.

Many Americans during and after the Civil War believed the creation of a fiat currency was unconstitutional. The Constitution explicitly stated that only gold and silver could be considered legal tender. In 1871, in the case of Knox v. Lee, the Supreme Court settled the matter by declaring that making United States notes legal tender was indeed constitutional.

By this time, the greenback was at the center of a countrywide debate on monetary policy. When the post-Civil War economic boom ended in the panic and depression of 1873, many people, especially farmers, blamed the Treasury’s policy of contracting the currency — that is, removing United States notes from circulation in an attempt to go back to the gold standard, which would require that a $1 note could be redeemed for $1 in gold.

As a consequence, there was a call for the expansion of United States note circulation or an inflation of the currency. This belief became joined with a political ideology that opposed big business and banking interests, resulting in the birth of the Greenback Party in 1874.

Opposing the Greenbackers were more conservative interests, sometimes known as “gold bugs,” who found support in the Republican Party and in elements of the Democratic Party. Gold interests proved the stronger contestant in the debate and in 1878, the total circulation of United States notes was fixed at a little over $346 million and the notes eventually became redeemable in gold (at least until 1933, when this provision was removed).

During the 20th century, United States notes became ever less important in the nation’s money supply, though Congress supported their continued circulation. They were increasingly replaced by currency issued by the Federal Reserve System, which came to look almost identical to the United States note. The Federal Reserve note thus became the new greenback.

In 1966, Congress allowed the Treasury to start removing United States notes from circulation. The last delivery of the notes by the Bureau of Engraving and Printing to the Treasury was made in 1971. In 1994, the Riegle Community Development and Regulatory Improvement Act eliminated the issuance of the notes altogether.

So instead of real money, America has an impostor “which came to look almost identical to the United States note” with the full complicity of everyone in charge, just so that when needed, any and all untenable debt burdens can be inflated away. And while the latter is a topic of a whole different discussion, we present another chart which, unlike the 150th anniversary of fiat, should be something discussed far more broadly… Because in a fiat world superpower status is always relative.

-

[Active updates: Developing stories] The South Carolina Treasurer’s Office, acting upon a directive from the state legislature, has recently published a report on the advisability of investing in gold and silver. Basically, the state legislature wanted to know if it’s wise to invest public funds under it’s custody in gold & silver.

Here’s what the Treasurer’s Office has to say about itself:

Our mission is to serve the citizens of South Carolina by providing the most efficient banking, investment and financial management service for South Carolina State Government. Our commitment is to safeguard our State’s financial resources and to maximize return on our State’s investments.

This is a tall order, hence we can assume that the report must be well researched and credible. It concluded that it is not advisable to invest public funds in gold & silver because:-

There’s escalating market speculation

Current value (I think they mean price) is too high

Market possibly in a bubble

South Carolina Code of Laws states that the Treasurer has “ full power to invest” in debt instruments of the US government and corporations, but makes no mention of investments in derivatives of gold & silver. Hence investing in gold & silver derivatives may “create a legal conflict”

While the timestamp of the document was 27 Feb 2012, it can be assumed that the report was prepared soon after the end of September 23, 2011 due to this inclusion. From the perspective of a short term investment, that was a pretty good call, considering the fact that gold and silver have been taken down to $1624 and $31.40 respectively as I write.

However, this piece is not about how good the Treasurer’s Office was at making an investment call based on price. Neither is it about whether gold & silver is in a bubble. These conclusions (2) & (3) are opinions of the Treasurer’s Office, which are subjective. Of greater interest are the facts revealed in the body of the report.

Regular readers of this blog would have noticed that there are several key issues that are repeatedly discussed or highlighted here (through news feeds or third party contributions). They include:-

Gold & silver prices are being suppressed

Central Banks & major bullion banks are suppressing their prices

Naked short selling is one of the price suppression mechanism

Bullion Banks and exchanges practice fractional reserve bullion banking

Stay out of gold or silver bank accounts, ETFs, Certificates, and all forms of derivatives

The safest way to own gold & silver is to hold physical gold & silver

Items (1) to (4) are often disputed by the mainstream media and investors, sometimes referring to them as conspiracy theories. Hence, it is most interesting to see what this government published report has to say about these 6 issues.

Price Suppression is Real

In one short paragraph, this report confirms in no uncertain terms the truth behind the so called “conspiracy theories”. Not only does it confirm the existence of price suppression, it discloses the WHOs and the HOWs!

Risks of holding gold through ETFs, Certificates, Bank Accounts & other Derivatives

It has been repeatedly emphasized here that the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system. Anything else is a derivative - a paper or electronic representation of the real thing.

This report explains the nature of these derivatives and lists the risks associated with each, together with reasons why the Treasury’s Office advised against investing in them.

The full report in pdf is available for download at the South Carolina Treasurer’s website. Text from relevant sections is reproduced below with comments related to the 6 items above highlighted. Most of the remarks are self explanatory. There are, however, two groups of comments that warrant some discussion.

1. Allocated & Unallocated Accounts

Ways to Invest: Certificates

Unallocated gold certiñcates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. Allocated gold certificates should be correlated with speciñc numbered bars, however it is difficult to prove whether a bank is improperly allocating a single bar to more than one investor.

Ways to Invest: Accounts

One of the most important differences between accounts is whether the gold is held on an allocated or unallocated basis. Another major difference is the strength of the account holder’s claim on the gold, in the event that the account administrator faces gold-denominated liabilities, asset forfeiture, or bankruptcy.

The above describes two products offered by banks to clients who want to invest in gold (or silver) without having to deal with the physical metals. For example, when a bank accepts $2,000 from a customer and issues a gold certificate or credits the customer’s gold account under the unallocated system, the bank is not obliged to buy and store 1.2 oz (at current price) of gold on behalf of the customer. It holds only a tiny portion of that amount in gold. Hence when many of its the customers decide to redeem their certificates at the same time, the bank will not have sufficient gold to deliver. This is what’s referred to as a “run on the bank’s gold on deposit”. The same applies when depositing cash in your bank. The practice of keeping only a tiny fraction of what’s rightfully belonging to the customers (gold or cash) is referred to as fractional reserve banking.

When selling allocated gold products, the bank is legally required to hold 100% of the customers deposit in physical metal. For example, if a customer deposits sufficient cash to own a 400 oz gold bar and is assigned a bar bearing serial No: AGR Matthey 156571, how can one be sure that the same bar or a portion thereof is not assigned to another customer at the same time? That’s the issue raised by the report - and the risk is real.

This brings us back to “the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system”. If you have to use a third party to store your metals, use specialized private vaults instead, because banks operate on a fractional reserve banking system.

There are many companies outside the banking system that offer secure vaulting services. Generally, they have very high transparency, including publishing audited client holdings on the web for public scrutiny (without any login required). Of course clients’ ID are anonymous, and known only to the operator and the client.

2. Reason for not investing in physical gold & silver

The report listed 5 ways to invest in gold & silver - ETPs, Certificates, Accounts, Derivatives and physical coins & bars. Notice how it highlights & explains all the risks associated with ETPs, Certificates, Accounts and Derivatives and the reasons why it is not advisable for the Treasury to invest in these.

Notice also that there are NO risk associated with physical metals. The only reason given for not investing in coins and bars is “South Carolina does not have the capacity to store or funding to secure gold and silver bullion”.

Proviso 89.145 GP:

Gold & Silver Investments

Office of State Treasurer

-

GOLD AND SILVER AS AN INVESTMENT:

Historically, investors have purchased gold as a hedge against an economic, a political, or a currency crisis. A decline in investment markets, a growing national debt, a weak currency, increasing inflation, military conflicts and social unrest are the most common reasons for investment in gold. Currently, gold and silver are at historic highs leading many expert investors to conclude that a bubble has been created in the precious metals market. Since the US recession began, the value of gold and silver has increased as investment markets perform poorly, troublesome economic news is announced, and when uncertainty in international markets intensifies.

Similar to other commodities, the value of gold and silver is determined by supply and demand, as well as speculation. The Federal Reserve, The London Bullion Market Association, JP Morgan Chase, and HSBC Holdings have practiced fractional-reserve banking and engaged in naked short selling causing artiñcial price suppression.

There are several ways to invest in gold and silver: bars, coins, ETP’s, certificates, accounts, and derivatives. If a state were to choose to invest in gold (and silver), it would likely choose to invest by:

1. ETP’s-Exchange Traded Products. This allows the stakeholder to invest in bullion without having to store bars and coins. The ñrst gold ETF (Exchange Traded Fund) was created in 2003 and has been viewed largely as a success, but has also been compared to investing in mortgagebacked securities. The annual expenses of the fund (storage, insurance, and management fees) are charged by selling a small amount of gold represented by each certificate, so the amount of gold in each certificate will gradually decline over time. ETF’s are investment companies that are legally classified as open-end companies or Unit Investment Trusts (UIT), but differ from traditional open-end companies and U]T’s. The main differences are that ETF’s do not sell directly to investors and they issue their shares in what are called Creation Units. Also, the Creation Units may not be purchased with cash but a basket of securities that mirrors the ETF‘s portfolio. The Usually, the Creation Units are split up and re-sold on a secondary market.

2. Certificates- allow investors to avoid the risks and costs associated with the transfer and storage of bullion by taking on a set of risks and costs associated with the certificate itself. Banks may issue gold certificates for gold which is allocated (non-fungible) or unallocated (fungible). Unallocated gold certiñcates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. Allocated gold certificates should be correlated with speciñc numbered bars, however it is difficult to prove whether a bank is improperly allocating a single bar to more than one investor. The US ñrst authorized the use of gold certificates in 1863. By the early l930’s the US placed restrictions on private gold ownership and therefore, the gold certificates stopped circulating as money, but certificates are still issued by gold pool programs for investment purposes.

3. Accounts- Many banks offer gold accounts where gold can be instantly bought or sold just like any foreign currency on a fractional reserve (non-allocated, fungible) basis. Pool accounts, facilitate highly liquid, but unallocated claims on gold owned by the company. Digital gold currency systems operate like pool accounts and additionally allow the direct transfer of fungible gold between members of the service. Different accounts impose varying types of intermediation between the client and their gold. One of the most important differences between accounts is whether the gold is held on an allocated or unallocated basis. Another major difference is the strength of the account holder’s claim on the gold, in the event that the account administrator faces gold-denominated liabilities, asset forfeiture, or bankruptcy.

4. Derivatives- The product symbol for gold futures is GC, and it is traded in a standard contract

size of 100 troy ounces. In the US, gold futures are primarily traded on the New York Commodities Exchange (COMEX). As of 2009 holders of COMEX gold futures have experienced problems taking delivery of their metal. Along with chronic delivery delays, some investors have received delivery of bars not matching their contract in serial number and weight. Because of these problems, there are concerns that COMEX may not have the gold inventory to back its existing warehouse receipts.

ADVISABILITY: There is no statute preventing the State from investing in gold and silver. The various methods of investment in gold and silver each carry different and often significant risks, the foremost being speculation. As the US has experienced the recent bursts in the housing and tech bubbles, it is important to take caution when contemplating an unconventional investment. Taxpayer money (state funds and state pension) across the US has not typically been used to invest in gold or silver bullion.

Recently, with the uncertainty in global markets, the devaluation of the dollar, rising inflation, and a flat US economy, there has been a renewed interest in either moving back to a gold standard, investing in gold or both. The value of gold and silver has significantly increased in the last decade, meaning it would cost a great deal to invest at this time.

Risks: 1. Bars and coins-South Carolina does not have the capacity to store or funding to secure gold and silver bullion. For these reasons the State Treasurer’s Office does not advise investing in gold and silver bars and coins.

2. ETP’s- The armual expenses and costs associated with this type of investment are high. In recent years there have been issues surrounding gold ETP’s. The purchase price provides the investor with a fluctuating amount (in weight) of the metal. Over time, as value increases and more investors participate in the fund, the amount of metal owner by the investor decreases. ETP’s can also be split and sold on the secondary market. For these reasons the State Treasurer’s Ofñce does not advise investing in ETP’s for gold and silver.

3. Certificates- Certificates for allocated gold present an accountability problem. Allocated gold certificates are supposed to be correlated with speciñc numbered bars; however, it is difficult to verify whether a bank is improperly allocating a single bar to more than one investor. Also, unallocated gold certificates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. This is in conflict with S.C. Code of Laws 1976 SECTION 11-9-660. For these reasons, the State Treasurer’s Office cannot advise investing in gold and silver certificates.

4. Accounts- Similar to the risks associated with gold and silver certificates, allocated and unallocated metals held in accounts produce similar accountability problems. The strength of the account holder’s claim on metals is subject to the account administrators liabilities, assets, and/or solvency. Per S.C. Code of Laws 1976 SECTION 11-9-660, the State Treasurer’s Office cannot advise investing in gold and silver accounts.

5. Derivatives- Over the last three years, gold futures traded on the New York Commodities Exchange (COMEX) have encountered significant accountability problems. Holders of COMEX gold ñltures have frequently experienced delivery delays of their metals. Once delivered, there have been many reports of inaccurate weights and serial numbers on bars that do not match the holder’s contract. For these reasons the State Treasurer’s Office does not advise investing in gold and silver derivatives.

-

Gold: April 2012

-

Having read the above, it may now be easier to make sense of the sharp price decline for both gold & silver over the past 2 days. Lets now ask some questions. Was the price action due to:

Market forces or Price Suppression in action?

Falling Demand or Naked Short Selling?

Human Traders or High Frequency Traders (HFTs)?

Historically, investors have purchased gold as a hedge against an economic, a political, or a currency crisis. A decline in investment markets, a growing national debt, a weak currency, increasing inflation, military conflicts and social unrest are the most common reasons for investment in gold

Have any of the issues above that formed the rationale for purchasing gold (and silver) been resolved?

Recently, with the uncertainty in global markets, the devaluation of the dollar, rising inflation, and a flat US economy, there has been a renewed interest in either moving back to a gold standard, investing in gold or both.

The mainstream media attributed this week’s sharp price decline to improving economy, low inflation and no imminent QE announcements following the release of the latest FOMC meeting minutes. Given that the above statement was published just 5 weeks before the FOMC minutes, who is lying?

- Developing Stories

12 Apr: Jason Hommel explains what Blythe Masters actually meant by “the underlying client position that we’re hedging”.

11 Apr:

Ted Butler, the pioneer of silver manipulation investigation finally broke his silence over the Blythe Masters denial video clip. By far, this is THE best, most level-headed, objective rebuttal to Masters’ famous words that they are “not running a large directional position”. Read “JPM’s TV appearance” posted at Silverseek.com.

Keiser Report on the same subject. His solution is the Silver Liberation Army (SLA)

-

7 Apr: Mike Maloney on RT discussing gold & silver manipulation, Blythe Masters denial of JPM’s role in price manipulation, “First government admission of price suppression” & High Frequency Sheering. Must Watch!

Shortly after BuySilverMalaysia.com launched its webstore on Feb 2, I learnt from its proprietor that he has received numerous emails asking if he would offer buyback as part of the service. “It seems like Malaysians’ concern is about selling back their silver”, he lamented. You’ll notice that it is one of only two dealers amongst those reviewed here without a buyback service.

This is one of the tell-tale signs that many Malaysians who have recently caught wind of the gold & silver story are erroneously looking at gold & silver as speculative investments. They are interested in making a quick buck by buying these metals with the hope of selling them back to their dealers when prices move up in short order. Some are even excited about gold or silver savings accounts offered by various banks and are happy to invest in paper gold or silver. To get an idea of the general sentiment, check out some lively threads at the Lowyat forum (start here, here or here).

Meanwhile, over in the US, it has been reported that bullion dealers who’ve been serving their customers for decades see very little buybacks. Their long term customers have been accumulating these metals, buying when prices are rising and buying even more when there’s a price dip. How is that so?

In a recent interview by SGTreport, Andy Hoffman of Miles Franklin said:

There are no buy-backs. Customers are not selling anything. They haven’t been selling any gold & silver back to Miles Franklin or any of our competitors for years, and they’re never going to. So don’t ever ever think that when you see a big smash in gold or silver that it’s people selling. It has nothing to do with it. It is the gold cartel naked shorting paper, and it’s only a matter of time before they completely and uterly are destroyed as they were in 1968 with the London Gold Pool, and as they have been every single time in history when they attempt to subvert the forces of real money with paper.

You’re not even investing, you’re just owning real money… and you’re doing it for defense. We’re here to protect ourselves.

People should not think of silver & gold as investments. They are savings.

There you have it. They buy gold & silver for different reasons. Not for speculation. Not even as an investment. They buy whenever they wanted to convert their savings from one form of money into another. It is like someone having more confidence in the SGD than RM looking for opportunities to buy more SGD whenever exchange rates are favorable. They buy and hold gold and silver as savings because they know that these monetary metals store value (retain purchasing power) much better than paper currencies. Most importantly, they own gold & silver fully aware that these are political metals, whose prices are actively managed or manipulated by central banks.

[Note: It may appear from the paragraph above that Americans are astute investors or savers. Far from it. Retail ownership of gold & silver on a per capita basis is much higher in India and many Asian countries than in the US. The "they" refers to a very tiny group of well informed Americans who understand gold & silver for what they are.]

For a better understanding of the issues discussed above, listen to SGTreport’s interview with Andy Hoffman discussing a range of topics including Price Manipulation using High Frequency Trading (HFT), Quantifiable Criminality, Exponentially off-the-chart Methods of Attacking, Silver Subsidies, Gold Silver Ratio (GSR), and more. -

Part 1

High Frequency Trading (HFT) is now something like 75% of all NYSE trading as well as a big percentage of COMEX trading.

Goldman Sach is trading 1 out of every 6 trades on the NYSE everyday, which is basically the government controlling the market.

Avoid all paper investments. The only way you can beat them is with physical gold & silver that’s not margined.

Computers have taken over the market.

Part 2

Back in 2008, when silver was knocked down [to] $8 or $9 an ounce, the real price never got lower than $17 or $18 and most people don’t realise that.

You’re not even investing, you’re just owning real money… and you’re doing it for defense. We’re here to protect ourselves.

People should not think of silver & gold as investments. They are savings.

Silver sales in dollars is pretty darn close to gold sales in dollars.

In the news article featured here in September 2011, the Dutch glassworkers pension fund (SPVG) was ordered by De Nederlandsche Bank (DNB, or the equivalent of the Dutch central bank) to sell the bulk of its gold assets. News is out that the “Order” has been overturned by the court, and the pension fund is now claiming damages amounting to €10m - the difference between the current gold price and the price when the gold was sold a year ago.

Court overturns Dutch regulator’s order to slash gold allocation

NETHERLANDS – A Rotterdam court has overturned the Dutch pensions regulator’s recent demand that SPVG – the pension fund for glass manufacturers – divest more than three-quarters of its 13% gold allocation.

The regulator is now facing a claim for damages, estimated at €10m-11m – the difference between the current gold price and the price when the gold was sold a year ago, according to Rob Daamen, the scheme’s deputy secretary.

The court said it was not convinced the regulator had fully taken into account the scheme’s specific conditions, or the entirety of its investment portfolio.

It also concluded that interpretation of the so-called ‘prudent person’ rule should be the sole prerogative of the pension fund, and that the regulator’s task was simply to ascertain whether this standard had been applied correctly.

“[The regulator] has not made clear in any way why a gold allocation of 13% is not in conformity with the prudent person rule, and that an allocation of 3% is,” the court said.

It also dismissed the watchdog’s reference to the drop in the gold price in 1980, or its standard deviation estimate of 33.7%.

Instead, it pointed to the scheme’s statement that the gold price had increased steadily over the last 10 years, and that the standard deviation between 2000 and 2010 had been no more than 13.1%.

In its verdict, the court said it would re-open the investigation before it delivered a verdict on the damages.

Spokesman Cees Verhagen said the regulator would look over the verdict closely before deciding whether to appeal the ruling.

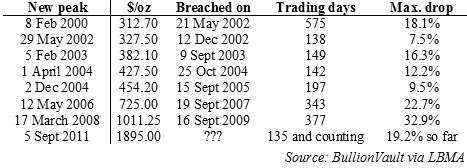

It’s now 6 months since gold hit its current all-time high. How long ’til the next…?

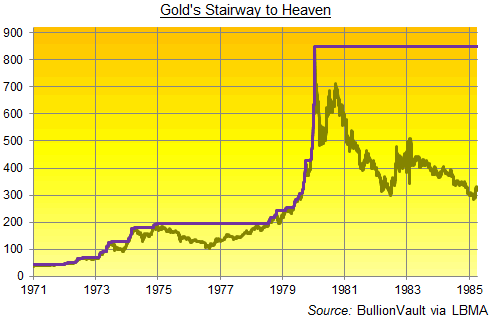

Thanks to hindsight, the bull market in gold which followed Richard Nixon unpegging the US Dollar, and therefore the rest of the world, from its last pretence of a Gold Standard sounds as inevitable today as Jimmy Page’s solo in Stairway to Heaven, also a 1971 classic.

But the gold price’s rise from $35 per ounce to $850 in less than a decade hardly ran that smooth at the time.

Hitting a new record high of $70 per ounce within a year of floating free from the Dollar, gold took 6 months to reach and breach that high again. The gold price then took a further six months to break the next July’s top at $127…then almost 7 months to break spring 1974′s high at $179.50…and then more than three years to top that winter’s peak of $195.25 per ounce.

Knowing not to sell but hang tight wasn’t easy. Not least because US investors had only just got in at the top. Nixon’s successor as US president, Gerald Ford made buying gold legal for the first time in three decades on the last day of 1974. But planning ahead, international bullion dealers had already pushed the price to that peak of $195 per ounce just 1 day earlier. So come the middle of 1976, America’s earliest buyers had lost 45% before costs.

Who could have said for sure that they would recover not only that loss, but make a further 355% gain on top, when gold finally peaked at the start of 1980 - the same year Zeppelin broke up? And who could have guessed that second peak would then prove gold’s ultimate climax - way up there, as high as heaven itself - for nearly three decades, longer even than a live Jimmy Page solo?

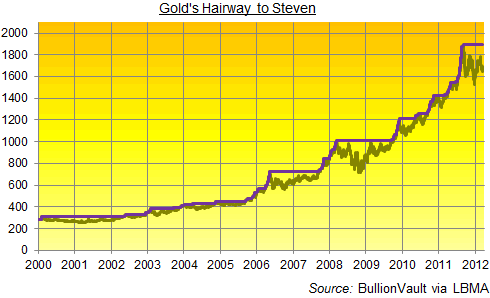

Fast forward to spring 2012, and it’s now six months since gold hit what remains, for now, its latest all-time peak - a London Gold Fix on 5 Sept. 2011 of $1895 per ounce.

Just how long might gold owners wait to see it get there again? To date, the 21st century bull market has enjoyed seven breathers longer than this one so far. Ignore the first (it took the gold price very nearly back to 1999′s two-decade low beneath $253), and the average wait in these extended pauses has been nearly 11 months.

As you can see, higher prices are harder work to recover. The one before this - which began the day Bear Stearns imploded - took the gold price one-third lower for US investors. Its next peak (if not its final crescendo) came 180% higher from there.

Think of it more as Hairway to Steven than Stairway to Heaven. Because like the Butthole Surfers, investors either love gold or hate it, and the vast majority don’t get it at all. It makes one hell of a racket, terrifying and surprising those who dare to go near it, pounding onwards and upwards, right until the moment it falters and stops.

“Eventually, there will be a crisis of such magnitude that the political winds change direction, and become blustering gales forcing us onto the course of fiscal sustainability,” says Dylan Grice, strategist at Société Générale in his new Popular Delusions report for clients.

“Until it does, the temptation to inflate will remain, as will economists with spurious mathematical rationalisations as to why such inflation will make everything OK…Until [then], the outlook will remain favorable for gold. But eventually, majority opinion will accept the painful contractionary medicine because it will have to. That will be the time to sell gold.”

In the meantime, investors and savers cannot know that they are buying an uptrend instead of the top. Gold took very nearly 28 years to recover the big top of Jan. 1980 - way up there at $850 per ounce. That topped the 25-year recovery in US stocks after 1929′s Great Crash. We won’t know if Japan sets a new record pause with its stocks and real estate until November 2017. But the 30-year bull market in US Treasury bonds is sure to leave a heavenly high-water mark when interest rates turn upwards from today’s all-time historic lows.

Some are even excited about gold or silver savings accounts offered by various banks and are happy to invest in paper gold or silver. To get an idea of the general sentiment, check out some lively threads at the Lowyat forum (start

Some are even excited about gold or silver savings accounts offered by various banks and are happy to invest in paper gold or silver. To get an idea of the general sentiment, check out some lively threads at the Lowyat forum (start  Jim Puplava, president of FPS, discusses the hot topic of Silver Manipulation with four prominent players in the silver market.

Jim Puplava, president of FPS, discusses the hot topic of Silver Manipulation with four prominent players in the silver market. NETHERLANDS – A Rotterdam court has overturned the Dutch pensions regulator’s recent demand that SPVG – the pension fund for glass manufacturers – divest more than three-quarters of its 13% gold allocation.

NETHERLANDS – A Rotterdam court has overturned the Dutch pensions regulator’s recent demand that SPVG – the pension fund for glass manufacturers – divest more than three-quarters of its 13% gold allocation.

More Charts: 1-Month, 1-Year, 5-Year, 10-Year

More Charts: 1-Month, 1-Year, 5-Year, 10-Year More Charts: 1-Month, 1-Year, 5-Year, 10-Year

More Charts: 1-Month, 1-Year, 5-Year, 10-Year

Government admission of price suppression: Report by South Carolina State Treasurer’s Office

-

[Active updates: Developing stories] The South Carolina Treasurer’s Office, acting upon a directive from the state legislature, has recently published a report on the advisability of investing in gold and silver. Basically, the state legislature wanted to know if it’s wise to invest public funds under it’s custody in gold & silver.

Here’s what the Treasurer’s Office has to say about itself:

This is a tall order, hence we can assume that the report must be well researched and credible. It concluded that it is not advisable to invest public funds in gold & silver because:-

While the timestamp of the document was 27 Feb 2012, it can be assumed that the report was prepared soon after the end of September 23, 2011 due to this inclusion. From the perspective of a short term investment, that was a pretty good call, considering the fact that gold and silver have been taken down to $1624 and $31.40 respectively as I write.

However, this piece is not about how good the Treasurer’s Office was at making an investment call based on price. Neither is it about whether gold & silver is in a bubble. These conclusions (2) & (3) are opinions of the Treasurer’s Office, which are subjective. Of greater interest are the facts revealed in the body of the report.

Regular readers of this blog would have noticed that there are several key issues that are repeatedly discussed or highlighted here (through news feeds or third party contributions). They include:-

Items (1) to (4) are often disputed by the mainstream media and investors, sometimes referring to them as conspiracy theories. Hence, it is most interesting to see what this government published report has to say about these 6 issues.

Price Suppression is Real

In one short paragraph, this report confirms in no uncertain terms the truth behind the so called “conspiracy theories”. Not only does it confirm the existence of price suppression, it discloses the WHOs and the HOWs!

Risks of holding gold through ETFs, Certificates, Bank Accounts & other Derivatives

It has been repeatedly emphasized here that the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system. Anything else is a derivative - a paper or electronic representation of the real thing.

This report explains the nature of these derivatives and lists the risks associated with each, together with reasons why the Treasury’s Office advised against investing in them.

The full report in pdf is available for download at the South Carolina Treasurer’s website. Text from relevant sections is reproduced below with comments related to the 6 items above highlighted. Most of the remarks are self explanatory. There are, however, two groups of comments that warrant some discussion.

1. Allocated & Unallocated Accounts

The above describes two products offered by banks to clients who want to invest in gold (or silver) without having to deal with the physical metals. For example, when a bank accepts $2,000 from a customer and issues a gold certificate or credits the customer’s gold account under the unallocated system, the bank is not obliged to buy and store 1.2 oz (at current price) of gold on behalf of the customer. It holds only a tiny portion of that amount in gold. Hence when many of its the customers decide to redeem their certificates at the same time, the bank will not have sufficient gold to deliver. This is what’s referred to as a “run on the bank’s gold on deposit”. The same applies when depositing cash in your bank. The practice of keeping only a tiny fraction of what’s rightfully belonging to the customers (gold or cash) is referred to as fractional reserve banking.

When selling allocated gold products, the bank is legally required to hold 100% of the customers deposit in physical metal. For example, if a customer deposits sufficient cash to own a 400 oz gold bar and is assigned a bar bearing serial No: AGR Matthey 156571, how can one be sure that the same bar or a portion thereof is not assigned to another customer at the same time? That’s the issue raised by the report - and the risk is real.

This brings us back to “the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system”. If you have to use a third party to store your metals, use specialized private vaults instead, because banks operate on a fractional reserve banking system.

There are many companies outside the banking system that offer secure vaulting services. Generally, they have very high transparency, including publishing audited client holdings on the web for public scrutiny (without any login required). Of course clients’ ID are anonymous, and known only to the operator and the client.

Try these links:

GoldMoney bar list and BullionVault client holdings. Their reviews can be found here.

Learn more about private vaulting services, including issues like ownership, custody, bailment, counter-party risks, and performance risks.

2. Reason for not investing in physical gold & silver

The report listed 5 ways to invest in gold & silver - ETPs, Certificates, Accounts, Derivatives and physical coins & bars. Notice how it highlights & explains all the risks associated with ETPs, Certificates, Accounts and Derivatives and the reasons why it is not advisable for the Treasury to invest in these.

Notice also that there are NO risk associated with physical metals. The only reason given for not investing in coins and bars is “South Carolina does not have the capacity to store or funding to secure gold and silver bullion”.

What a lame excuse! Do they not know that in April last year, “The University of Texas Investment Management Co., the second-largest U.S. academic endowment, took delivery of almost $1 billion in gold bullion“?

-

Proviso 89.145 GP:

Gold & Silver Investments

Office of State Treasurer

-

GOLD AND SILVER AS AN INVESTMENT:

Historically, investors have purchased gold as a hedge against an economic, a political, or a currency crisis. A decline in investment markets, a growing national debt, a weak currency, increasing inflation, military conflicts and social unrest are the most common reasons for investment in gold. Currently, gold and silver are at historic highs leading many expert investors to conclude that a bubble has been created in the precious metals market. Since the US recession began, the value of gold and silver has increased as investment markets perform poorly, troublesome economic news is announced, and when uncertainty in international markets intensifies.

Similar to other commodities, the value of gold and silver is determined by supply and demand, as well as speculation. The Federal Reserve, The London Bullion Market Association, JP Morgan Chase, and HSBC Holdings have practiced fractional-reserve banking and engaged in naked short selling causing artiñcial price suppression.

There are several ways to invest in gold and silver: bars, coins, ETP’s, certificates, accounts, and derivatives. If a state were to choose to invest in gold (and silver), it would likely choose to invest by:

1. ETP’s-Exchange Traded Products. This allows the stakeholder to invest in bullion without having to store bars and coins. The ñrst gold ETF (Exchange Traded Fund) was created in 2003 and has been viewed largely as a success, but has also been compared to investing in mortgagebacked securities. The annual expenses of the fund (storage, insurance, and management fees) are charged by selling a small amount of gold represented by each certificate, so the amount of gold in each certificate will gradually decline over time. ETF’s are investment companies that are legally classified as open-end companies or Unit Investment Trusts (UIT), but differ from traditional open-end companies and U]T’s. The main differences are that ETF’s do not sell directly to investors and they issue their shares in what are called Creation Units. Also, the Creation Units may not be purchased with cash but a basket of securities that mirrors the ETF‘s portfolio. The Usually, the Creation Units are split up and re-sold on a secondary market.

2. Certificates- allow investors to avoid the risks and costs associated with the transfer and storage of bullion by taking on a set of risks and costs associated with the certificate itself. Banks may issue gold certificates for gold which is allocated (non-fungible) or unallocated (fungible). Unallocated gold certiñcates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. Allocated gold certificates should be correlated with speciñc numbered bars, however it is difficult to prove whether a bank is improperly allocating a single bar to more than one investor. The US ñrst authorized the use of gold certificates in 1863. By the early l930’s the US placed restrictions on private gold ownership and therefore, the gold certificates stopped circulating as money, but certificates are still issued by gold pool programs for investment purposes.

3. Accounts- Many banks offer gold accounts where gold can be instantly bought or sold just like any foreign currency on a fractional reserve (non-allocated, fungible) basis. Pool accounts, facilitate highly liquid, but unallocated claims on gold owned by the company. Digital gold currency systems operate like pool accounts and additionally allow the direct transfer of fungible gold between members of the service. Different accounts impose varying types of intermediation between the client and their gold. One of the most important differences between accounts is whether the gold is held on an allocated or unallocated basis. Another major difference is the strength of the account holder’s claim on the gold, in the event that the account administrator faces gold-denominated liabilities, asset forfeiture, or bankruptcy.

4. Derivatives- The product symbol for gold futures is GC, and it is traded in a standard contract

size of 100 troy ounces. In the US, gold futures are primarily traded on the New York Commodities Exchange (COMEX). As of 2009 holders of COMEX gold futures have experienced problems taking delivery of their metal. Along with chronic delivery delays, some investors have received delivery of bars not matching their contract in serial number and weight. Because of these problems, there are concerns that COMEX may not have the gold inventory to back its existing warehouse receipts.

ADVISABILITY:

There is no statute preventing the State from investing in gold and silver. The various methods of investment in gold and silver each carry different and often significant risks, the foremost being speculation. As the US has experienced the recent bursts in the housing and tech bubbles, it is important to take caution when contemplating an unconventional investment. Taxpayer money (state funds and state pension) across the US has not typically been used to invest in gold or silver bullion.

Recently, with the uncertainty in global markets, the devaluation of the dollar, rising inflation, and a flat US economy, there has been a renewed interest in either moving back to a gold standard, investing in gold or both. The value of gold and silver has significantly increased in the last decade, meaning it would cost a great deal to invest at this time.

Risks:

1. Bars and coins- South Carolina does not have the capacity to store or funding to secure gold and silver bullion. For these reasons the State Treasurer’s Office does not advise investing in gold and silver bars and coins.

2. ETP’s- The armual expenses and costs associated with this type of investment are high. In recent years there have been issues surrounding gold ETP’s. The purchase price provides the investor with a fluctuating amount (in weight) of the metal. Over time, as value increases and more investors participate in the fund, the amount of metal owner by the investor decreases. ETP’s can also be split and sold on the secondary market. For these reasons the State Treasurer’s Ofñce does not advise investing in ETP’s for gold and silver.

3. Certificates- Certificates for allocated gold present an accountability problem. Allocated gold certificates are supposed to be correlated with speciñc numbered bars; however, it is difficult to verify whether a bank is improperly allocating a single bar to more than one investor. Also, unallocated gold certificates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. This is in conflict with S.C. Code of Laws 1976 SECTION 11-9-660. For these reasons, the State Treasurer’s Office cannot advise investing in gold and silver certificates.

4. Accounts- Similar to the risks associated with gold and silver certificates, allocated and unallocated metals held in accounts produce similar accountability problems. The strength of the account holder’s claim on metals is subject to the account administrators liabilities, assets, and/or solvency. Per S.C. Code of Laws 1976 SECTION 11-9-660, the State Treasurer’s Office cannot advise investing in gold and silver accounts.

5. Derivatives- Over the last three years, gold futures traded on the New York Commodities Exchange (COMEX) have encountered significant accountability problems. Holders of COMEX gold ñltures have frequently experienced delivery delays of their metals. Once delivered, there have been many reports of inaccurate weights and serial numbers on bars that do not match the holder’s contract. For these reasons the State Treasurer’s Office does not advise investing in gold and silver derivatives.

-

Gold: April 2012

-

Having read the above, it may now be easier to make sense of the sharp price decline for both gold & silver over the past 2 days. Lets now ask some questions. Was the price action due to:

The mainstream media attributed this week’s sharp price decline to improving economy, low inflation and no imminent QE announcements following the release of the latest FOMC meeting minutes. Given that the above statement was published just 5 weeks before the FOMC minutes, who is lying?

-

Developing Stories

12 Apr:

Jason Hommel explains what Blythe Masters actually meant by “the underlying client position that we’re hedging”.

11 Apr:

Ted Butler, the pioneer of silver manipulation investigation finally broke his silence over the Blythe Masters denial video clip. By far, this is THE best, most level-headed, objective rebuttal to Masters’ famous words that they are “not running a large directional position”. Read “JPM’s TV appearance” posted at Silverseek.com.

10 Apr:

-

7 Apr:

Mike Maloney on RT discussing gold & silver manipulation, Blythe Masters denial of JPM’s role in price manipulation, “First government admission of price suppression” & High Frequency Sheering. Must Watch!

-

6 Apr:

Further Reading:

-

Rate this:

Share this:

Like this: