The Politics of Gold

Submitted by Adrian Ash | BullionVault

Wednesday, 10 October 2012

Putting on My Top Hat

Hardly nice while it lasted, austerity is running out of friends fast…

IT’S A COMMON MYTH that the Labour government in power when the Great Depression went global in 1931 was forced to resign by a banker’s ramp, writes Adrian Ash at BullionVault.

The British prime minister, Ramsay Macdonald, denied it at the time. Close academic study has since found evidence lacking, too. But the idea of millionaires in top hats conspiring to weaken both the Pound and British debt (then consuls, now gilts) still lingers.

By demanding gold for their paper at the Bank of England, these interwar illuminati effectively handed a direct demand to London, ordering a cut in welfare payments so severe that Labour politicians – elected by the “working man” – had no choice but to stand down. Or so the narrative runs. That left an emergency coalition led by the top-hatted Conservatives to impose those same cuts with impunity.

So who’s playing the top-hatted villain today – and where has gold gone?

First, step forward the IMF. Founded on the monetary rubble of WWII, the International Monetary Fund has since come to represent the monied interest in debt resolution worldwide. It finds default intolerable. Repayment in full – if not now, then years into the future – can be the only choice if a country wants IMF money to finance current spending when the markets refuse.

Today the IMF is most famous for bossing Asia about in the late 1990s. Those tigers learnt their lesson, building war-chests of foreign currency – and seeking to block inflows of “hot” money from Western speculators – all through the 21st century thus far. Thailand, South Korea and the rest learnt their lesson so well, in fact, that the global financial crisis, and the Eurozone catastrophe in particular, arrived just in time. Because after scolding wayward spenders like an English aristo’s nanny for 60 years, the IMF found its own finances shot through by the start of 2008. Thanks on one hand to a lack of business, plus an over-staffed bureaucracy on the other. Praise be for Greece!

The IMF has been busy dispensing budget advice to pretty much all other Western governments too, whether they want it or not. Sometimes they do, sometimes they don’t. It depends on domestic concerns – meaning which way domestic voters are blowing on government spending themselves. Back in Britain, for instance, today’s Conservative-led coalition – taking power in 2010 after Labour yet again screwed things up – was only too happy to cite the IMF’s advice as support for its package of lower spending, higher taxes.

The stated aim was to fix the mess left by Labour. But to what end? The Conservatives actually denied having a bigger agenda, of aiming to shrink the state for good. So why bother in the short run? Because this couldn’t go on.

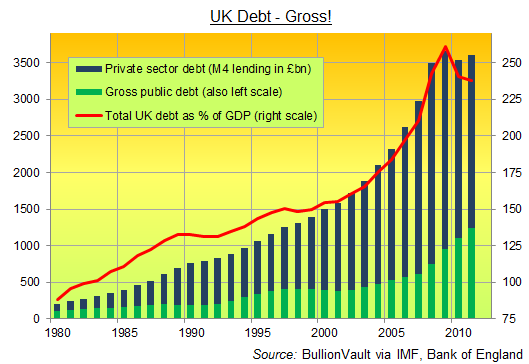

Our chart shows gross UK debt – gross as in like grody to the max. Public debt has more than doubled since 2007. Private-sector debt couldn’t keep pace, but starting from a much higher base it’s now worth 156% of the UK’s annual economic output all by itself. Swelling above £2.7 trillion as the financial crisis really kicked in, it even proved too much for Britain’s insatiable consumers to swallow. They have actually raised their savings and cut their debt from the record levels of spring 2010, just before the Conservative-led coalition took power, closing the shortfall between savings and debt by £119bn in two and a half years.

That’s equal to 2.9% of GDP each and every year – and it’s what makes this no ordinary recession, as Nomura economist Richard Koo constantly reminds us.

A large portion of the private sector is actually minimizing debt…[and] when the private sector deleverages in spite of zero interest rates, the economy enters a deflationary spiral.

Keep smiling! Consumers will no longer consume more than they earn, whether or not interest rates are at zero, the central bank prints money, or commercial lenders will actually lend them more money. Such household austerity chimed with the Conservatives’ election platform of spring 2010, or at least chimed enough to give the Tories enough of the vote to invite the Lib-Democrats to play muggins in coalition. So did the IMF’s po-faced advice…as well as raw common sense…and the entire history of out-sized debt since France and England tried and failed to continue spending when already bust at the start of the 18th century.

Richard Koo, however, keeps at it:

This is no time to embark on fiscal consolidation. Such measures must wait until it is certain the private sector has finished deleveraging and is ready to borrow and spend the savings that would be left un-borrowed by the government under an austerity program.

The logic is plain. For all I know he may well be right. And besides, sticking the course is hard, as Angela Merkel said in Athens this week, before dodging the riots and getting back on her plane to fly home to Germany. It’s hard even for international policy wonks hoping to get a senior banking job if not academic tenure when all this blows over.

“The International Monetary Fund has moved a step closer to withdrawing its support for the UK’s economic strategy,” reports the top-hats’ former favorite daily, the Financial Times“, advising the government to redraw its fiscal tightening plan if growth disappoints in the coming quarters.

“The IMF said in its Fiscal Monitor report, published on Tuesday, that Britain should relax its fiscal consolidation strategy, aimed at cancelling the UK’s structural deficit by 2017, if the economy remained weak.” The IMF used to think austerity would be its own reward, with Britain’s GDP quietly recovering its pre-crisis levels as the government cut spending and raised taxes. But the UK economy won’t play along – most obviously, everyone now thinks, because the government cut spending and raised taxes. True or not doesn’t matter, and we’ll never get to find out anyway. Because even though UK households still have a further gap of £66 billion to close between their aggregate savings and debt, the consensus on austerity – or what passed for it – is starting to crack. Which brings us back to gold.

Today, just as in the 1930s, anyone choosing to Buy Gold with at least a chunk of their savings will first need to have savings to defend. What they don’t need is formal evening dress and a monocle. Just a little – or a lot – stashed away. Such people don’t usually vote for higher taxes or bigger government deficits. Because both are bad for your wealth, the first by eating it directly, the second by inviting later governments to eat it through inflation.

We don’t know any UK gold investors who voted Labour in 2010, for instance. We doubt there are many in the US who’ll be voting for Obama next month either. (That doesn’t mean they’ll bring themselves to vote Romney.) Yet in both economies, gold has gone AWOL from the debate. Gold remains oddly absent from the Eurozone debt crisis too, even though the single currency zone is the world’s heaviest holder as a portion of central-bank reserves outside the almighty United States.

Ron Paul’s exit from the White House race has kept gold off the Republican platform. Gold still only tips up in UK politics when the Tory press feels the urge to remind everyone how stupid, arrogant and utterly lacking in historical sense former Labour chancellor and then prime minister Gordon Brown was when he sold half the UK’s bullion reserves at what proved the very bottom of a 20-year bear market. Yet for die-hard gold bugs, such Labourite or “liberal” policies (in the US sense) as helped get us all into this mess are plainly good for gold prices. Because they encourage other savers to fear for their money, and rightly so.

Seeking refuge outside currency and outside debt, gold buyers helps push Gold Prices higher. So too – we fear – will voting for any political party in Europe, the UK or US this decade. Not voting won’t save the Western economies either, of course. But rolling back state spending, and cutting back state deficits, is proving beyond the British Tories. It’s proving too tough for even the International Monetary Fund. The top hats look ready to quit the field.

Picture the chart above with deficit state spending on top. Now picture UK gilt prices and the value of Sterling five years ahead.

-

Adrian Ash is head of research at BullionVault – the secure, low-cost gold and silver market for private investors online, where you can buy physical gold today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

Leave a Reply

Featured Reviews

05Sep: Bill Murphy (GATA)

$50 silver by year end

13Aug: James Turk (GoldMoney)

We won’t see $1580 gold & $27 silver again

12Aug: Bill Murphy's source

We could see a 100% increase in 90 days.

03Aug: HSBC Analysts

Gold to rally above $1,900 by end 2012

05June: David Bond (SilverMiners)

Gold & Silver may bottom at $1,200 & $18

02June: Don Coxe (Coxe Advisors)

Europe to issue Gold-backed Euro Bonds within the next 3 months

21May: Gene Arensberg (GotGoldReport)

Gold and Silver are very close to a bottom, if one has not already been put in last week

9May: Eric Sprott (Sprott Asset)

Gold over $2000, Silver over $50 by year end

>> More forecasts & forecast accuracy

Daily GOLD US$/oz

Daily SILVER US$/oz

More Gold Charts: 1 Month to 660 Years

More Silver Charts: 1 Month to 660 Years

Gold & Silver Interviews (KWN)

Gold & Silver Interviews (KWN)

- Exclusive - Riots & Money Fleeing The Euro Into Gold & Silver October 13, 2012

- Art Cashin - We Are At Risk Of A Frightening Hyperinflation October 12, 2012

- Fleckenstein - Gold & Insane Central Banks Printing Trillions October 12, 2012

- Embry - This War In Gold & Shorts Getting Overrun October 12, 2012

- The $2 Trillion European Bailout Package Is Coming October 11, 2012

- Turk - Expect A Massive Short Squeeze In Gold & Silver October 11, 2012

- Lost Confidence Can’t Be Restored & Gold’s Final Move October 11, 2012

- Europe & The Major Breakout For Gold Is Still In Front Of Us October 10, 2012

Finance & Economics

- Beta Testing QE 4 - "Large Amount " Of $100 Bills Stolen From Federal Reserve October 13, 2012 Tyler Durden

- Guest Post: The Problem With Centralization October 13, 2012 Tyler Durden

- The US Fiscal 'Moment': Cliff, Slope, Or Wile E. Coyote? October 13, 2012 Tyler Durden

- German Self-Immolates In Front Of Reichstag October 13, 2012 Tyler Durden

- On China's Transition October 13, 2012 Tyler Durden

- Forget 666; 808 Is The Number Of This Market's Beast October 13, 2012 Tyler Durden

- Blame Isn't a Platform October 13, 2012 Phoenix Capital Research

- Europe, For One, Welcomes Its New Asian Overlords October 13, 2012 Tyler Durden