Archive

Collapse At Hand

-

Republished with permission from Dr. Roberts | Institute for Political Economy

[Charts inserted by editor]

Collapse At Hand

By Dr. Paul Craig Roberts | June 5, 2012

Ever since the beginning of the financial crisis and quantitative easing, the question has been before us: How can the Federal Reserve maintain zero interest rates for banks and negative real interest rates for savers and bond holders when the US government is adding $1.5 trillion to the national debt every year via its budget deficits? Not long ago the Fed announced that it was going to continue this policy for another 2 or 3 years. Indeed, the Fed is locked into the policy. Without the artificially low interest rates, the debt service on the national debt would be so large that it would raise questions about the US Treasury’s credit rating and the viability of the dollar, and the trillions of dollars in Interest Rate Swaps and other derivatives would come unglued.

Ever since the beginning of the financial crisis and quantitative easing, the question has been before us: How can the Federal Reserve maintain zero interest rates for banks and negative real interest rates for savers and bond holders when the US government is adding $1.5 trillion to the national debt every year via its budget deficits? Not long ago the Fed announced that it was going to continue this policy for another 2 or 3 years. Indeed, the Fed is locked into the policy. Without the artificially low interest rates, the debt service on the national debt would be so large that it would raise questions about the US Treasury’s credit rating and the viability of the dollar, and the trillions of dollars in Interest Rate Swaps and other derivatives would come unglued.

In other words, financial deregulation leading to Wall Street’s gambles, the US government’s decision to bail out the banks and to keep them afloat, and the Federal Reserve’s zero interest rate policy have put the economic future of the US and its currency in an untenable and dangerous position. It will not be possible to continue to flood the bond markets with $1.5 trillion in new issues each year when the interest rate on the bonds is less than the rate of inflation. Everyone who purchases a Treasury bond is purchasing a depreciating asset. Moreover, the capital risk of investing in Treasuries is very high. The low interest rate means that the price paid for the bond is very high. A rise in interest rates, which must come sooner or later, will collapse the price of the bonds and inflict capital losses on bond holders, both domestic and foreign.

The question is: when is sooner or later? The purpose of this article is to examine that question.

Let us begin by answering the question: how has such an untenable policy managed to last this long?

A number of factors are contributing to the stability of the dollar and the bond market. A very important factor is the situation in Europe. There are real problems there as well, and the financial press keeps our focus on Greece, Europe, and the euro. Will Greece exit the European Union or be kicked out? Will the sovereign debt problem spread to Spain, Italy, and essentially everywhere except for Germany and the Netherlands?

Will it be the end of the EU and the euro? These are all very dramatic questions that keep focus off the American situation, which is probably even worse.

The Treasury bond market is also helped by the fear individual investors have of the equity market, which has been turned into a gambling casino by high-frequency trading.

High-frequency trading is electronic trading based on mathematical models that make the decisions. Investment firms compete on the basis of speed, capturing gains on a fraction of a penny, and perhaps holding positions for only a few seconds. These are not long-term investors. Content with their daily earnings, they close out all positions at the end of each day.

High-frequency trades now account for 70-80% of all equity trades. The result is major heartburn for traditional investors, who are leaving the equity market. They end up in Treasuries, because they are unsure of the solvency of banks who pay next to nothing for deposits, whereas 10-year Treasuries will pay about 2% nominal, which means, using the official Consumer Price Index, that they are losing 1% of their capital each year. Using John Williams’ (shadowstats.com) correct measure of inflation, they are losing far more. Still, the loss is about 2 percentage points less than being in a bank, and unlike banks, the Treasury can have the Federal Reserve print the money to pay off its bonds. Therefore, bond investment at least returns the nominal amount of the investment, even if its real value is much lower. (For a description of High-frequency trading, see: http://en.wikipedia.org/wiki/High_frequency_trading )

The presstitute financial media tells us that flight from European sovereign debt, from the doomed euro, and from the continuing real estate disaster into US Treasuries provides funding for Washington’s $1.5 trillion annual deficits. Investors influenced by the financial press might be responding in this way. Another explanation for the stability of the Fed’s untenable policy is collusion between Washington, the Fed, and Wall Street. We will be looking at this as we progress.

Unlike Japan, whose national debt is the largest of all, Americans do not own their own public debt. Much of US debt is owned abroad, especially by China, Japan, and OPEC, the oil exporting countries. This places the US economy in foreign hands. If China, for example, were to find itself unduly provoked by Washington, China could dump up to $2 trillion in US dollar-dominated assets on world markets. All sorts of prices would collapse, and the Fed would have to rapidly create the money to buy up the Chinese dumping of dollar-denominated financial instruments.

The dollars printed to purchase the dumped Chinese holdings of US dollar assets would expand the supply of dollars in currency markets and drive down the dollar exchange rate. The Fed, lacking foreign currencies with which to buy up the dollars would have to appeal for currency swaps to sovereign debt-troubled Europe for euros, to Russia, surrounded by the US missile system, for rubles, to Japan, a country over its head in American commitment, for yen, in order to buy up the dollars with euros, rubles, and yen.

These currency swaps would be on the books, unredeemable and making additional use of such swaps problematical. In other words, even if the US government can pressure its allies and puppets to swap their harder currencies for a depreciating US currency, it would not be a repeatable process. The components of the American Empire don’t want to be in dollars any more than do the BRICS.

However, for China, for example, to dump its dollar holdings all at once would be costly as the value of the dollar-denominated assets would decline as they dumped them. Unless China is faced with US military attack and needs to defang the aggressor, China as a rational economic actor would prefer to slowly exit the US dollar. Neither do Japan, Europe, nor OPEC wish to destroy their own accumulated wealth from America’s trade deficits by dumping dollars, but the indications are that they all wish to exit their dollar holdings.

Unlike the US financial press, the foreigners who hold dollar assets look at the annual US budget and trade deficits, look at the sinking US economy, look at Wall Street’s uncovered gambling bets, look at the war plans of the delusional hegemon and conclude: “I’ve got to carefully get out of this.”

US banks also have a strong interest in preserving the status quo. They are holders of US Treasuries and potentially even larger holders. They can borrow from the Federal Reserve at zero interest rates and purchase 10-year Treasuries at 2%, thus earning a nominal profit of 2% to offset derivative losses. The banks can borrow dollars from the Fed for free and leverage them in derivative transactions. As Nomi Prins puts it, the US banks don’t want to trade against themselves and their free source of funding by selling their bond holdings. Moreover, in the event of foreign flight from dollars, the Fed could boost the foreign demand for dollars by requiring foreign banks that want to operate in the US to increase their reserve amounts, which are dollar based.

I could go on, but I believe this is enough to show that even actors in the process who could terminate it have themselves a big stake in not rocking the boat and prefer to quietly and slowly sneak out of dollars before the crisis hits. This is not possible indefinitely as the process of gradual withdrawal from the dollar would result in continuous small declines in dollar values that would end in a rush to exit, but Americans are not the only delusional people.

The very process of slowly getting out can bring the American house down. The BRICS-Brazil, the largest economy in South America, Russia, the nuclear armed and energy independent economy on which Western Europe (Washington’s NATO puppets) are dependent for energy, India, nuclear armed and one of Asia’s two rising giants, China, nuclear armed, Washington’s largest creditor (except for the Fed), supplier of America’s manufactured and advanced technology products, and the new bogyman for the military-security complex’s next profitable cold war, and South Africa, the largest economy in Africa-are in the process of forming a new bank. The new bank will permit the five large economies to conduct their trade without use of the US dollar.

In addition, Japan, an American puppet state since WWII, is on the verge of entering into an agreement with China in which the Japanese yen and the Chinese yuan will be directly exchanged. The trade between the two Asian countries would be conducted in their own currencies without the use of the US dollar. This reduces the cost of foreign trade between the two countries, because it eliminates payments for foreign exchange commissions to convert from yen and yuan into dollars and back into yen and yuan.

Moreover, this official explanation for the new direct relationship avoiding the US dollar is simply diplomacy speaking. The Japanese are hoping, like the Chinese, to get out of the practice of accumulating ever more dollars by having to park their trade surpluses in US Treasuries. The Japanese US puppet government hopes that the Washington hegemon does not require the Japanese government to nix the deal with China.

Now we have arrived at the nitty and gritty. The small percentage of Americans who are aware and informed are puzzled why the banksters have escaped with their financial crimes without prosecution. The answer might be that the banks “too big to fail” are adjuncts of Washington and the Federal Reserve in maintaining the stability of the dollar and Treasury bond markets in the face of an untenable Fed policy.

Let us first look at how the big banks can keep the interest rates on Treasuries low, below the rate of inflation, despite the constant increase in US debt as a percent of GDP-thus preserving the Treasury’s ability to service the debt.

The imperiled banks too big to fail have a huge stake in low interest rates and the success of the Fed’s policy. The big banks are positioned to make the Fed’s policy a success. JPMorgan Chase and other giant-sized banks can drive down Treasury interest rates and, thereby, drive up the prices of bonds, producing a rally, by selling Interest Rate Swaps (IRSwaps).

A financial company that sells IRSwaps is selling an agreement to pay floating interest rates for fixed interest rates. The buyer is purchasing an agreement that requires him to pay a fixed rate of interest in exchange for receiving a floating rate.

The reason for a seller to take the short side of the IRSwap, that is, to pay a floating rate for a fixed rate, is his belief that rates are going to fall. Short-selling can make the rates fall, and thus drive up the prices of Treasuries. When this happens, as these charts illustrate, there is

“U.S. Treasury Bond Teetering Tower Of Babel, Fed Stuck At 0% Forever” Jim Willie

“U.S. Treasury Bond Teetering Tower Of Babel, Fed Stuck At 0% Forever” Jim Willie

a rally in the Treasury bond market that the presstitute financial media attributes to “flight to the safe haven of the US dollar and Treasury bonds.” In fact, the circumstantial evidence (see the charts in the link above) is that the swaps are sold by Wall Street whenever the Federal Reserve needs to prevent a rise in interest rates in order to protect its otherwise untenable policy. The swap sales create the impression of a flight to the dollar, but no actual flight occurs. As the IRSwaps require no exchange of any principal or real asset, and are only a bet on interest rate movements, there is no limit to the volume of IRSwaps.

This apparent collusion suggests to some observers that the reason the Wall Street banksters have not been prosecuted for their crimes is that they are an essential part of the Federal Reserve’s policy to preserve the US dollar as world currency. Possibly the collusion between the Federal Reserve and the banks is organized, but it doesn’t have to be. The banks are beneficiaries of the Fed’s zero interest rate policy. It is in the banks’ interest to support it. Organized collusion is not required.

Let us now turn to gold and silver bullion. Based on sound analysis, Gerald Celente and other gifted seers predicted that the price of gold would be $2000 per ounce by the end of last year. Gold and silver bullion continued during 2011 their ten-year rise, but in 2012 the price of gold and silver have been knocked down, with gold being $350 per ounce off its $1900 high.

In view of the analysis that I have presented, what is the explanation for the reversal in bullion prices? The answer again is shorting. Some knowledgeable people within the financial sector believe that the Federal Reserve (and perhaps also the European Central Bank) places short sales of bullion through the investment banks, guaranteeing any losses by pushing a key on the computer keyboard, as central banks can create money out of thin air.

Insiders inform me that as a tiny percent of those on the buy side of short sells actually want to take delivery on the gold or silver bullion, and are content with the financial money settlement, there is no limit to short selling of gold and silver. Short selling can actually exceed the known quantity of gold and silver.

Some who have been watching the process for years believe that government-directed short-selling has been going on for a long time. Even without government participation, banks can control the volume of paper trading in gold and profit on the swings that they create. Recently short selling is so aggressive that it not merely slows the rise in bullion prices but drives the price down. Is this aggressiveness a sign that the rigged system is on the verge of becoming unglued?

In other words, “our government,” which allegedly represents us, rather than the powerful private interests who elect “our government” with their multi-million dollar campaign contributions, now legitimized by the Republican Supreme Court, is doing its best to deprive us mere citizens, slaves, indentured servants, and “domestic extremists” from protecting ourselves and our remaining wealth from the currency debauchery policy of the Federal Reserve. Naked short selling prevents the rising demand for physical bullion from raising bullion’s price.

Jeff Nielson explains another way that banks can sell bullion shorts when they own no bullion. (See, http://www.gold-eagle.com/editorials_08/nielson102411.html) Nielson says that JP Morgan is the custodian for the largest long silver fund while being the largest short-seller of silver. Whenever the silver fund adds to its bullion holdings, JP Morgan shorts an equal amount. The short selling offsets the rise in price that would result from the increase in demand for physical silver. Nielson also reports that bullion prices can be suppressed by raising margin requirements on those who purchase bullion with leverage. The conclusion is that bullion markets can be manipulated just as can the Treasury bond market and interest rates.

How long can the manipulations continue? When will the proverbial hit the fan?

If we knew precisely the date, we would be the next mega-billionaires.

Here are some of the catalysts waiting to ignite the conflagration that burns up the Treasury bond market and the US dollar:

A war, demanded by the Israeli government, with Iran, beginning with Syria, that disrupts the oil flow and thereby the stability of the Western economies or brings the US and its weak NATO puppets into armed conflict with Russia and China. The oil spikes would degrade further the US and EU economies, but Wall Street would make money on the trades.

An unfavorable economic statistic that wakes up investors as to the true state of the US economy, a statistic that the presstitute media cannot deflect.

An affront to China, whose government decides that knocking the US down a few pegs into third world status is worth a trillion dollars.

More derivate mistakes, such as JPMorgan Chase’s recent one, that send the US financial system again reeling and reminds us that nothing has changed.

The list is long. There is a limit to how many stupid mistakes and corrupt financial policies the rest of the world is willing to accept from the US. When that limit is reached, it is all over for “the world’s sole superpower” and for holders of dollar-denominated instruments.

Financial deregulation converted the financial system, which formerly served businesses and consumers, into a gambling casino where bets are not covered. These uncovered bets, together with the Fed’s zero interest rate policy, have exposed Americans’ living standard and wealth to large declines. Retired people living on their savings and investments, IRAs and 401(k)s can earn nothing on their money and are forced to consume their capital, thereby depriving heirs of inheritance. Accumulated wealth is consumed.

As a result of jobs offshoring, the US has become an import-dependent country, dependent on foreign made manufactured goods, clothing, and shoes. When the dollar exchange rate falls, domestic US prices will rise, and US real consumption will take a big hit. Americans will consume less, and their standard of living will fall dramatically.

The serious consequences of the enormous mistakes made in Washington, on Wall Street, and in corporate offices are being held at bay by an untenable policy of low interest rates and a corrupt financial press, while debt rapidly builds. The Fed has been through this experience once before. During WW II the Federal Reserve kept interest rates low in order to aid the Treasury’s war finance by minimizing the interest burden of the war debt. The Fed kept the interest rates low by buying the debt issues. The postwar inflation that resulted led to the Federal Reserve-Treasury Accord in 1951, in which agreement was reached that the Federal Reserve would cease monetizing the debt and permit interest rates to rise.

Fed chairman Bernanke has spoken of an “exit strategy” and said that when inflation threatens, he can prevent the inflation by taking the money back out of the banking system. However, he can do that only by selling Treasury bonds, which means interest rates would rise. A rise in interest rates would threaten the derivative structure, cause bond losses, and raise the cost of both private and public debt service. In other words, to prevent inflation from debt monetization would bring on more immediate problems than inflation. Rather than collapse the system, wouldn’t the Fed be more likely to inflate away the massive debts?

Eventually, inflation would erode the dollar’s purchasing power and use as the reserve currency, and the US government’s credit worthiness would waste away. However, the Fed, the politicians, and the financial gangsters would prefer a crisis later rather than sooner. Passing the sinking ship on to the next watch is preferable to going down with the ship oneself. As long as interest rate swaps can be used to boost Treasury bond prices, and as long as naked shorts of bullion can be used to keep silver and gold from rising in price, the false image of the US as a safe haven for investors can be perpetuated.

However, the $230,000,000,000,000 in derivative bets by US banks might bring its own surprises. JPMorgan Chase has had to admit that its recently announced derivative loss of $2 billion is more than that. How much more remains to be seen. According to the Comptroller of the Currency http://www.occ.treas.gov/topics/capital-markets/financial-markets/trading/derivatives/dq411.pdf the five largest banks hold 95.7% of all derivatives. The five banks holding $226 trillion in derivative bets are highly leveraged gamblers. For example, JPMorgan Chase has total assets of $1.8 trillion but holds $70 trillion in derivative bets, a ratio of $39 in derivative bets for every dollar of assets. Such a bank doesn’t have to lose very many bets before it is busted.

Assets, of course, are not risk-based capital. According to the Comptroller of the Currency report, as of December 31, 2011, JPMorgan Chase held $70.2 trillion in derivatives and only $136 billion in risk-based capital. In other words, the bank’s derivative bets are 516 times larger than the capital that covers the bets.

It is difficult to imagine a more reckless and unstable position for a bank to place itself in, but Goldman Sachs takes the cake. That bank’s $44 trillion in derivative bets is covered by only $19 billion in risk-based capital, resulting in bets 2,295 times larger than the capital that covers them.

Bets on interest rates comprise 81% of all derivatives. These are the derivatives that support high US Treasury bond prices despite massive increases in US debt and its monetization.

US banks’ derivative bets of $230 trillion, concentrated in five banks, are 15.3 times larger than the US GDP. A failed political system that allows unregulated banks to place uncovered bets 15 times larger than the US economy is a system that is headed for catastrophic failure. As the word spreads of the fantastic lack of judgment in the American political and financial systems, the catastrophe in waiting will become a reality.

Everyone wants a solution, so I will provide one. The US government should simply cancel the $230 trillion in derivative bets, declaring them null and void. As no real assets are involved, merely gambling on notional values, the only major effect of closing out or netting all the swaps (mostly over-the-counter contracts between counter-parties) would be to take $230 trillion of leveraged risk out of the financial system. The financial gangsters who want to continue enjoying betting gains while the public underwrites their losses would scream and yell about the sanctity of contracts. However, a government that can murder its own citizens or throw them into dungeons without due process can abolish all the contracts it wants in the name of national security. And most certainly, unlike the war on terror, purging the financial system of the gambling derivatives would vastly improve national security.

-

About The Author

Paul Craig Roberts has had careers in scholarship and academia, journalism, public service, and business. He is chairman of The Institute for Political Economy. Dr. Roberts was awarded the Treasury Department’s Meritorious Service Award for “his outstanding contributions to the formulation of United States economic policy.” In 1987 the French government recognized him as “the artisan of a renewal in economic science and policy after half a century of state interventionism” and inducted him into the Legion of Honor.

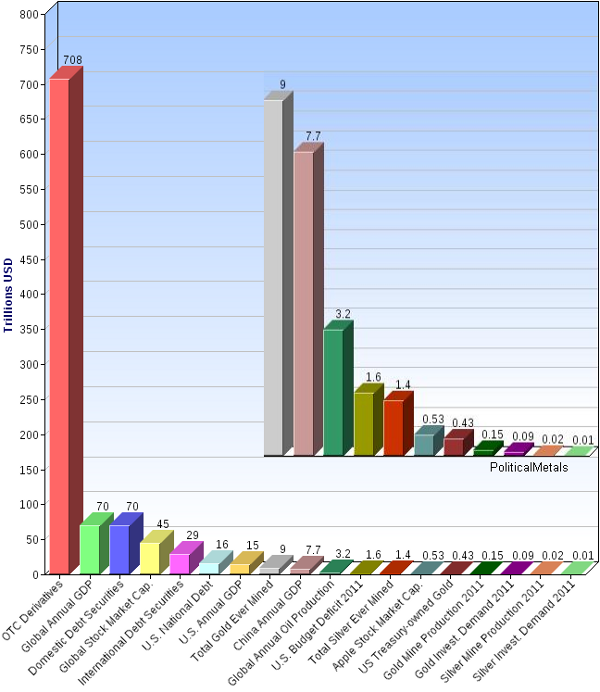

Further Reading:

Explore this chart to see The BIG Picture of Derivatives

Mouse over each bar for details. Click on bars for data source.

-

Like this:

JPM, Facebook, Gold … And The Potential of A Titanic Financial Market Event

Bill Murphy | LeMetropoleCafe

“The way I see it, if you want the rainbow, you gotta put up with the rain.” … Dolly Parton

GO GATA!!!

The reason for this rare, extra commentary over a weekend is to focus on a couple of points which really stand out in their particular significance and are worth pondering in terms of what is coming down the road for financial markets.

The first is what we jumped all over on PLANET GATA from the get-go about the JP Morgan hedge trade flap gone wrong. It made NO sense from the very beginning to any of us that such a commotion was made over a $2 billion loss on a trade, for whatever reason, when they had just reported yearly gains of $18 billion. Clearly, Mr. Dimon’s public pronouncement, that caught the attention of the entire investment world, was only paving the way for future announcements that will be much more dramatic. All he was doing when he inferred the losses MIGHT get worse was protecting himself, as best he could, by going on the record.

The latest news on JPM…

14:31 JPM JP Morgan Chase struggling to unwind ill-placed bets - WSJ

While breaking no real news, this story notes that the bank’s losses could eventually prove to be even bigger than the $5B some people familiar with the matter have been predicting (see linked comment). The losses could potentially deepen if the company sells its positions into a market that has turned against said positions.

The article notes that while the bank has said that it will take its time unwinding the positions, this does not necessarily guarantee smaller final losses than trying to close out the trades sooner, as the market could turn sharply against the bank in the near term.

Reference Link: Wall Street Journal

14:50 JPM CFTC latest federal agency to begin investigating JPMorgan Chase - NYT DealBook

NYT Dealbook reports, citing people briefed on the matter, that the Commodity Futures Trading Commission opened an enforcement case on Friday examining the bank’s trading loss. The CFTC joins the SEC and FBI in investigating possible wrongdoing at the bank. Gary Gensler, the agency’s chairman, is expected to disclose the investigation when he testifies on Tuesday before the Senate Banking Committee.

Dealbook says that the CFTC will potentially examine whether the bank’s trading affected the market for credit derivatives, for which it has jurisdiction.

Reference Link: NY Times

This latest investigation into JP Morgan might be a big deal for the GATA camp. This is actually quite complicated, but very intriguing. The CFTC has been investigating JPM’s role in the silver market manipulation scheme for what will be four years soon. FOUR YEARS! Good friends, like Dave from Denver, have nothing but loathsome talk about the CFTC, for good reason. GATA’s rationale (speaking for myself) about this ridiculous investigation is that the CFTC really has uncovered the scam, but because it is backed by the US Government, they are flabbergasted about what to do, so they do nothing.

The reason they have not closed the case is because they are petrified the silver market might blow up down the road. Think about if you were them. They want this to go away, but if the silver market does blow up, and there is some kind of “Force Majeure” declared in silver by JPM, the CFTC would not only look like fools, but, perhaps it might be said they were more than negligent. Thus, they have done nothing.

Well, all of a sudden, Lo and Behold a new factor enters the silver scam investigation, which directly affects Morgan’s constant claims to the CFTC that their huge silver short position is hedged. Ya mean like hedged in an economic sense as per their claims re the latest credit derivatives market trade was a hedge? This just might force the CFTC to demand JP Morgan prove their claims their silver short position is really a hedged one. This is what I suspect might occur due to the growing scrutiny over Morgan’s trading activities. The CFTC people, except for Bart “Elliot Ness” Chilton, are sycophants and have toed the company line … but there is a point when FEAR makes that no longer viable. They are not going to go to jail for taking one for the team. My guess is we are getting close to that Tipping Point.

As the JP Morgan hedged losses mount and become “official,” the heat on them is going to mount. They will be scrutinized every way imaginable. How can all the class action lawsuits against them, and blatant evidence against them via just what Andrew Maquire has sent to the CFTC via their role in the silver scam, be ignored?

We have already been informed, as of a week ago, that the Morgan losses on their “hedge trade” fiasco could be as high as $15 billion, or more. Already, even the WSJ is alluding that their losses are higher than $5 billion. This is MEGA! As we have discussed on PLANET GATA, this is not just about Morgan, but confidence in the entire financial system. If the $70 trillion derivatives book at Morgan goes NUCLEAR, we could have a financial market TITANIC event which might be right around the corner.

GOOD GRIEF!

Now, for the weekend edition, number two re the understandable, but nauseating, commotion over the Facebook IPO on Friday, which was heralded by CNBC all week.

First, the background…

*The Dow is going down day after day, not with any fanfare, but all rallies are sold. In very quiet and subdued selling, general investors inherently know something is wrong and are acting upon that instinct.

*Europe is falling apart we know, but little is being said about how the US financial system is in parallel with Europe. How bad is this? Just the state of California budget deficit goes from something like $8 billion to a staggering $16 billion and it creates almost no commotion. Huh?

Getting back into the GATA aspect of this is that the US financial markets are all about market manipulation. You need to go nowhere further on what the real deal about US financial markets than this headline…

Banks spend big to prop up Facebook shares on first day of trading

By GARETT SLOANE and MARK DECAMBRE

Last Updated: 8:15 AM, May 19, 2012

Posted: 11:34 PM, May 18, 2012It was another Wall Street bailout — but this time the banks had to cough up the cash. Facebook’s underwriters propped up the social-network’s trading debut yesterday, as the shares threatened to crash through the initial public offering price of $38. The banks working on the massive $16 billion IPO, including Morgan Stanley, JPMorgan Chase and Goldman Sachs, did their duty by buying up large blocks of Facebook stock toward the end of the day to support the price.

Facebook shares opened up 11 percent at $42.05, and traded as high as $45, before running out of steam, disappointing investors hoping for a big first-day pop. The shares closed up just 0.6 percent at $38.23.

Without the bank bailout, Facebook’s IPO would have been a loser on the day, Wall Street insiders said.

The heavy buying, however, cut into the banks’ already meager fees on the deal. The underwriters agreed to accept a smaller cut — just 1.1 percent of the $16 billion Facebook raised in the IPO — in order to land the high-profile assignment.

After splitting $176 million in fees, the firms likely spent more than they made in fees by buying the swooning stock. Sam Hamadeh, CEO of research firm Privco, believes the banks spent around $380 million on Facebook stock.

“On the heels of JPMorgan’s $2 billion ‘hedging’ trading loss, tThe underwriters have used up all the fees they made on the Facebook deal just to buy and prop up the stock to prevent a busted IPO,” said Hamadeh.

Another source said that the banks took a substantial hit yesterday, which started strong despite glitches that delayed Nasdaq trading in Facebook shares by 30 minutes past their 11 a.m. scheduled debut.

While there was plenty of finger-pointing yesterday, many blamed the bankers for setting the price too high to allow for upside. The IPO share priced at the high end of the $34 to $38 range, which had been raised from an initial range of $28 to $35.

The bankers were wary of pricing the shares too low, leaving money on the table and leading to an outrageous first-day pop. They were shooting for a modest first-day gain in the range of 5 percent to 10 percent.

Still, some observers heaped scorn on Facebook insiders who dumped their shares, saying it was a red flag that weighed on the stock.

Facebook had increased the number of shares being sold in the IPO by 25 percent, to 425 million, with most of the additional float coming from early investors looking to cash out.

The company’s sky-high valuation also made some investors queasy. At $38 a share, Facebook is valued at $104 billion — even though it only made $3.7 billion last year.

Facebook’s big day was a drag on other tech stocks. Trading in shares of Zynga was halted yesterday after a sharp drop, and the stock closed down 13.4 percent at $7.16. China’s social network RenRen was also down more than 20 percent, to $4.93.

[email protected]

My take on this, from my Behavioral Finance background on how our financial system really operates, is the effort to hold up the Facebook IPO was an effort to hold up the stock market as a whole. For the BF folks, perception is everything. That is why they do what they do. The Counterparty Risk Management Policy Group (do a Google if new to you), led by the same firms that held up the Facebook share price, does not exist for no reason. One of their mandates is to promote market stability and that is what they just did. That Group works closed with the Plunge Protection Team (Working Group on Capital Markets) to support the US stock market at various times.

What we saw in the price rises of gold and silver at the end of the week was stunning and totally out of the natural order of the gold/silver price manipulation scheme. It was a wowser! My smeller tells me, because the dramatic rally was so pronounced, that we are headed for some serious fireworks in the financial arena.

The Gold Cartel could be in deep trouble now because their honcho, JP Morgan, is in deepening trouble. This is no minor event in terms of the gold/silver market manipulation scandal.

All hands on deck to prepare for the financial market commotion that seems to be right around the corner!

-

Related Articles:

The only viable solution is to get government out of the money business permanently

The Fed: Mend It or End It?

-

Last week I held a hearing to examine the various proposals that have been put forth both to mend and to end the Fed. The purpose was to spur a vigorous and long-lasting discussion about the Fed’s problems, hopefully leading to concrete actions to rein in the Fed.

First, it is important to understand the Federal Reserve System. Some people claim it is a secret cabal of elite bankers, while others claim it is part of the federal government. In reality it is a bit of both. The Federal Reserve System is the collusion of big government and big business to profit at the expense of taxpayers. The Fed’s bailout of large banks during the financial crisis propped up poorly-run corporations that should have gone under, giving them a market-distorting advantage that no business in the United States should receive. The recent news about JP Morgan is a case in point. JP Morgan, a recipient of $25 billion in bailout money, recently announced it lost another $2 billion. If a corporation shows itself to be a bottomless money pit of “errors, sloppiness and bad judgment,” the Fed shouldn’t have expected $25 billion in free money to change that or teach anyone a lesson in fiscal discipline. But it determined that this form of deliberate capital destruction was preferable to one business suffering bankruptcy. Clearly, some changes need to be made.

Several reforms for the Fed were discussed at the hearing. One was a call for the full employment mandate to be repealed, in order to allow the Fed to focus solely on stable prices.

Another reform calls for changes to the composition of the Federal Open Market Committee. Still another proposal was for outright nationalization of the Fed or of its functions. But if what the Fed does now is bad and inflationary, allowing the Treasury to print and issue money at-will would be even worse, and could possibly lead to a Weimar-like hyperinflation.

The problems and advantages of the gold standard were discussed at the hearing. The era of the classical gold standard was undoubtedly one of the greatest eras in human history. For a period of several decades in the late 19th century, the West made enormous advances. However, the gold standard was still run by government. The temptation to suspend gold redemption reared its head again with the outbreak of World War I. Once the tie to gold was severed and fiscal restraint thrown to the wind, undoing the damage would have required great fiscal austerity. Instead, the Western world proceeded to set up a gold-exchange standard which lasted not even a decade before easy money led to the Great Depression.

While returning to the gold standard would certainly be far better than maintaining the current fiat paper system, as long as the government retains the power to go off gold we may end up repeating the same mistakes.

The only viable solution is to get government out of the money business permanently. The way to bring this about is through currency competition: allow parallel currencies to circulate without receiving any special recognition or favor from the government. Fiat paper monetary standards throughout history have always collapsed due to their inflationary nature, and our current fiat paper standard will be no different.

It is imperative that the American people be educated on the dangers of the Fed and the importance of restoring sound money. The laying of the groundwork must begin today, so that the American people will be prepared for the day when the mirage the Fed has created evaporates completely. The full hearing footage is available on my website and I would encourage every American to take a look.

-

Commodity Money and Fiat Money: A Bushel of Wheat for a Penny

A Bushel of Wheat for a Penny Part 1

by Steve Elwart, IDB Folio Specialist

Republished with permission from Koinonia House

-

This is Part 1 of a three-part series on money: where it comes from, how governments use it to control our lives, and how modern money policy makes the prophecies in the Book of Revelation seem very close to fulfillment.

Everyone reading this article is being robbed. We all use paper money and every day, governments are lowering its value. That value is being stolen from us. To understand how this is happening, we need to get to the basics of money. What is it?

Commodity Money

We learn in Genesis that Abram (renamed later by God to Abraham) was a rich man. How do we know? We are told that “he had sheep, and oxen, and he asses, and menservants, and maidservants, and she asses, and camels.”1 In Biblical times, these things were all media of exchange. No king decided this; he didn’t call in his magi to decide what the medium of ex-change would be. Ordinary people, or “the market” made the decision. Let’s say a king did decree that rocks could be used as money. Would anyone use them? Probably not, because they would not know the value of those rocks. Unless you are building a lot of things (or stoning a lot of adulterers), rocks fail to meet a standard for money: they have no intrinsic value.

If a civilization was to advance though, it had to come up with a convenient way to save and exchange value to buy things. Leather was used in ancient Rome. (Contrary to popular belief, Roman soldiers were not paid in salt. The term salary [from the Latin salārium] was money given to Roman soldiers to buy salt.2) Animal pelts, whiskey, and tobacco leaves were used in the former British Colonies, wampum (strings of beads) was used by the American Indians, dried fish were used in the Canadian maritime colonies, maize or corn was used in Mexico, and salt, iron and farming tools were used in Africa. These things are called “commodity money.” As civilizations became more complex, most forms of commodity money be-came very cumbersome. (Who would want to give or get 300 sheep to buy a car?) Another medium of exchange had to be found.

Over the centuries, the answer came to be the precious metals, gold and silver. These two metals became the basis for money in most of the world. Gold and silver were used as money for very specific reasons and they were chosen by “the market.” People decided that these two metals had all the qualities that made for a good medium of exchange:

- They were easily portable. They had high value to weight ratios. (So if you want to buy a car, you only have to bring 16 ounces of gold rather than 300 sheep.)

- They are fungible. Every ounce is like every other ounce no matter where they were mined. People didn’t have to worry about the quality of the pure metal.

- They are highly divisible. They can be divided into very small parts or coins. The term “pieces of eight” came from the practice of taking a Spanish dollar, a real de a ocho and breaking it up into eight pieces or reales to make change. Diamonds fail the test of being divisible because if you break up a gem-quality diamond, it loses its value. (For that matter, sheep aren’t easily divisible either unless you are very hungry.)

- They are highly durable; the thirty pieces of silver paid to Judas are still in existence today.

- They are naturally scarce. They can’t be multiplied.

Fiat Money

There is another type of money besides commodity money, called fiat money. (Fiat from the Latin fiat, meaning “let it be done.”) This is an item, usually paper or low value metal coins, that is decreed to have value by a government.

A government puts fiat money into circulation first by connecting it to a gold or silver standard, but then cuts the link and says that gold and paper are no longer convertible, making the piece of paper “legal tender for all debts public and private.” It is obvious that debtors would be very happy if the pa-per money lost its value because they could pay their debts with inflated currency. In a letter to Edward Carrington in 1788, Thomas Jefferson wrote, “Paper is poverty … it is only the ghost of money, and not money itself.” Jefferson died bankrupt because of the early United States money (monetary) pol-icy based on paper.

It is not that fiat currency is a new invention. Fiat currency actually made its appearance over 1,000 years ago. China was the first country to issue true paper money around the 10th century A.D. Although the notes were valued at a certain ex-change rate for gold, silver, or silk, conversion was never allowed in practice. The bills were supposed to be redeemed after three years in circulation, but as more bills were printed with the older notes being refused redemption, inflation became evident. Government measures to prop up the currency were unsuccessful and it fell out of favor.3

In Europe, fiat money came into being around the 12th century. Villagers would store their gold and other valuables in their lord’s castle for safekeeping. But during this time of the Crusades and other European Wars, noblemen were always strapped for cash. When times were particularly bad, the noblemen would confiscate the villagers’ gold and silver and issue notes for it, to be redeemed later. Needless to say, the notes weren’t always honored or if they were redeemed, the holder of the note received less of their gold back than what they were promised. This is an early case of price inflation.

Today, fiat money will always bring on inflation for two reasons: 1) Politicians like to induce inflation because it gives the people the illusion of prosperity and 2) its declared value is much higher than the cost of producing it. Whether it is a $1 or $100 bill in fiat money, it costs only 4 cents to produce. In today’s electronic age, the production cost for new money is zero since money creation is just a keystroke and an entry in cyber-space. On the other hand, in history, if you had a $20 gold piece, the cost of that gold piece, less the cost to produce it, was about $20.

The Gold Standard

If the relative value of gold is tracked over the years, one can see how fiat money loses its value over time.

By the 1400s, most countries that had complex trading systems were using gold and silver for transactions. Prices held relatively steady through the early 20th century, except for lo-cal shortages and wars. In the United States the price of gold and the things it bought held its value with exceptions for war-time when the government printed paper money to cover its war debts. After the emergencies and the country went back on the gold standard, prices went back to about where they were. During the First World War, most countries involved in the war suspended the gold standard so they could print enough money to pay for their involvement in the war. After the war, these countries went back to a modified form of the gold standard, but abandoned it during the “Great Depression.”

In 1941, most countries adopted the Bretton Woods system, which set the exchange value for all currencies in terms of gold. Countries that signed the Bretton Woods agreement were obligated to convert their currencies held by foreign countries into gold valued at $35 per ounce. However, many countries just pegged their currency to the U.S. dollar, thus making it the de facto world currency.

In the 1960s the United States had done something unprecedented in its history. The country fought two wars at once. The United States fought a war halfway around the world in Vietnam and a second war at home, the “War on Poverty.” To do this, the United States started to borrow massively and brought on double digit inflation. To curb the inflation, the United States government started to deflate the dollar. 1963 marked the entrance of the new Federal Reserve notes and the disappearance of the $1 silver certificate. This marked the point that no longer did the U.S. Government have to pay in “lawful money.” Finally, in late 1973, the U.S. government decoupled the value of the dollar from gold altogether and the price shot up to $120 per ounce in the free market.4 Since the United States went off the Gold Standard, a dollar is worth only one-sixth of what it was in 1973. (At this writing, gold is priced at $1,220 per ounce.5)

Inflation Always Follows Fiat Money

The history of price inflation in the United States is repeated in every country that uses paper money. Keep in mind, rising prices are not always bad. If a good becomes scarce, its price will go up and may provide the motivation to introduce a new, better product for the market. The reason petroleum became so popular so quickly was because of the rising cost of whale oil. If governments propped up the price of whale oil to keep whalers and whale oil processors employed, it would have taken decades for the world to embrace petroleum as a substitute. And someday, petroleum will go the way of whale oil as long as market forces dictate the transition.

When a government inflates its currency, it increases prices by reducing the purchasing power of the money. The short-term effects though, can seem to be positive. Like a drug addict, inflated money gives the illusion of prosperity, making people feel good. But like the addict, withdrawal follows the high.

At first, the surge of more money makes people feel good be-cause they can pay off their debts with cheaper money and they seem to have more disposable income. As prices catch up, people then find it more expensive to live. In addition, their tax burden goes up, since many government taxes are progressive in nature, meaning the percentage tax increases as in-come or asset values (houses, cars, etc.) increase. Eventually the market will try to correct itself and a depression will follow.

At this point, people start to feel the pinch of their money buying less. They demand that their government do some-thing. Since studies have shown that voters only have a memory of one year when it comes to politics, politicians will make sure that the economy is good in an election year.6 They will artificially stimulate the economy to give voters the illusion that times are good again and reelect the incumbents. This lasts only so long and inflation, with its problems kick in again. This cycle of increasing the currency supply and price inflation ultimately ends with the collapse of the currency, sometimes preceded by hyperinflation. (Hyperinflation and its cultural effects will be covered in Part 3 of this series.) Surprisingly, the country has not learned its lesson and the devalued fiat currency is replaced with yet another fiat currency. Greece is a perfect example of this cycle.

The Greek drachma was minted in gold and silver in ancient Greece and made its reappearance as a fiat currency in 1841. Since then, the value of the drachma decreased. During the German-Italian occupation of the country from 1941-1944, hyperinflation ravaged the country, ending with the issuance of 100,000,000,000 (100 billion)-drachma notes in 1944. After Greece was liberated from Germany, old drachmae were ex-changed for new ones at the rate of 50,000,000,000 to 1. Only paper money was issued, again a fiat currency. Greece then went on a program of deficit spending for social programs and inflation started once again.

In 1953, in an effort to halt inflation, Greece joined the Bretton Woods system and the drachma was revalued at a rate of 1000 old drachma to one new drachma. In 1973 the Bretton Woods System was abolished; over the next 25 years the official exchange rate gradually declined, from 30 drachmas to one U.S. dollar to a ratio of 400:1. On January 1, 2002, the Greek drachma was officially replaced as the circulating currency by the Euro (again a fiat currency).7

Today, Greece is once again is in trouble. After years of continued deficit spending and the government’s easy monetary policy, Greece’s financial situation was badly exposed when the global economic downturn struck. Very quickly, the government’s “creative accounting” practices were exposed. The national debt, put at €300 billion ($413.6 billion), is bigger than the country’s entire economy, with some estimates placing it at 120 percent of gross domestic product in 2010. The country’s deficit—how much more it spends than it takes in—is 12.7 percent.

This time though, Greece just can’t inflate their way out of the problem. Now that they are on the Euro (in the “Euro-zone”), they have little control over their monetary policy. All their loans are in Euros and they must pay back the loans in Euros. One way to balance the national books is to implement harsh and unpopular spending cuts. Another way is to default on their debt. This would seriously damage the Euro as other countries look at default as a way out of their financial problems. (In fact, financial experts are predicting the demise of the Euro in as early as five years.8) A third way out is to separate itself from the Euro, go back on the drachma (fiat currency again) and then set an exchange rate of the drachma to the Euro at an artificially high number. The cycle of fiat money would then begin again.

As long as a country is on a fiat currency, inflation is sure to follow. Using a fiat currency could well reduce a civilization to work an entire day for a “bushel of wheat.”

In Part 2 of this series we will look at central banking and how the banks can change a society.

Notes:

- Genesis 12:16b (KJV).

- “The American Heritage Dictionary of the English Language, 4th edition”. Answers.com. Retrieved 2010-06-05.

- Ramsden, Dave (2004). “A Very Short History of Chinese Paper Money.” James J. Puplava Financial Sense.

- History of the Gold Standard: http://useconomy.about.com/od/monetarypolicy/p/gold_history.htm

- Monex Precious Metals: http://www.monex.com/monex/controller?pageid=prices.

- “Voters Respond to Economic Woes” Economics and Public Policy: http://knowledge.wpcarey.asu.edu/article.cfm?articleid=1668.

- Greek Drachma, Wikipedia: http://en.wikipedia.org/wiki/Greek_drachma#First_modern_drachma.

- “Euro ‘will be dead in five years’”: http://www.telegraphic.com.uk/finance/financetopics/budget/7806065?Euro-will-be-dead-in-five-years.html

Like this:

Featured Reviews

16Oct: Jeff Clark (Casey Research)

$2,300 gold by January 2014

05Sep: Bill Murphy (GATA)

$50 silver by year end

13Aug: James Turk (GoldMoney)

We won’t see $1580 gold & $27 silver again

12Aug: Bill Murphy's source

We could see a 100% increase in 90 days.

03Aug: HSBC Analysts

Gold to rally above $1,900 by end 2012

05June: David Bond (SilverMiners)

Gold & Silver may bottom at $1,200 & $18

02June: Don Coxe (Coxe Advisors)

Europe to issue Gold-backed Euro Bonds within the next 3 months

21May: Gene Arensberg (GotGoldReport)

Gold and Silver are very close to a bottom, if one has not already been put in last week

>> More forecasts & forecast accuracy

Daily GOLD US$/oz

Daily SILVER US$/oz

More Gold Charts: 1 Month to 660 Years

More Silver Charts: 1 Month to 660 Years

Gold/Silver Ratio: 1 Month to 660 Years

Gold & Silver Priced in BitCoins

Click to enlarge.

BitCoin donation welcomed.

1NQ4LqE8yL6rfAqikDU8wLhHSm5fntsWxk

Gold & Silver Interviews (KWN)

Gold & Silver Interviews (KWN)

- Central Planners Greatest Fear, Possible Surprises & Gold October 24, 2012

- Nigel Farage - We Are Headed To A ‘One World Government’ October 24, 2012

- Richard Russell - The Bear Is Angry & Bernanke Wants Out October 24, 2012

- Household Name From Top Hedge Fund Caught Manipulating October 23, 2012

- People Are Getting Scared And Liquidating & Germany’s Gold October 23, 2012

- No More Exits, We Are Already Past The Point Of No Return October 23, 2012

- This Key Chart Continues To Worry The Gold & Silver Bears October 23, 2012

- Significant Monetary Change Is Likely Headed Our Way October 22, 2012

Finance & Economics

- Guest Post: Secession Fever Sweeping Europe Meaningless Without Debt Repudiation October 25, 2012 Tyler Durden

- It's Been A Wild Ride October 25, 2012 Tyler Durden

- Taxman Strips Exotic Dancers' Write-Down October 25, 2012 Tyler Durden

- Why Did The Bundesbank Secretly Withdraw Two-Thirds Of Its London Gold? October 25, 2012 Tyler Durden

- Three Chinese 'Surveillance' Vessels Enter Japanese Waters Around Senkaku Islands October 25, 2012 Tyler Durden

- The European Nash Dis-equilibrium Through The Eyes Of A Greek October 24, 2012 Tyler Durden

- Guest Post: Plutonocrits October 24, 2012 Tyler Durden

- Shooting From The Hip And Hitting Consumers: Protectionism In France October 24, 2012 testosteronepit

From Canada to NZ, and everywhere in between, people are waking up!

-

From Canada to NZ, and everywhere in between, people are waking up! Waking up to the fact that the existing global monetary & banking system is seriously flawed. Many would even go as far as saying it is a fraud. Unless governments the world over change the way national currencies are created and managed, it is a mathematical certainty the system will collapse like a house of cards. Here’s a small collection of voices explaining the flawed or fraudulent system together with their calls for change and your personal action.

If all this is new to you, it’ll do you good to study the materials in the order they are listed below.

-

Share this:

Like this: