Archive

My Last Forecast on Silver and Gold Prices

By Jeff Nielson | SilverGold Bull

-

It seems at the very least ironic that as I begin a new chapter in my own career as precious metals analyst for Silver Gold Bull, that simultaneously I’m writing my last chapter on one facet of that analysis. This will be my last effort at playing the increasingly irrelevant game of attempting to forecast gold and silver prices – in terms of the bankers’ paper.

It seems at the very least ironic that as I begin a new chapter in my own career as precious metals analyst for Silver Gold Bull, that simultaneously I’m writing my last chapter on one facet of that analysis. This will be my last effort at playing the increasingly irrelevant game of attempting to forecast gold and silver prices – in terms of the bankers’ paper.

Many readers will be aghast at this announcement. How can I “analyze” the gold and silver market without providing guidance on its (paper) prices? I would immediately reverse this proposition with a question of my own. How can anyone provide rational estimates for future prices of hard assets which are being priced in paper which is already effectively worthless?

Now it is the paper-peddlers who would be horrified by my stance. How dare I assert that the beloved fiat-currencies which they (and their propaganda machine) place in such high esteem are worthless? Here I have a host of arguments at my disposal, several of which I have used in the past.

There is the obvious analogy between paper currencies and the shares of a corporation. With nothing officially “backing” these paper currencies, our governments can only impute value in this paper as a claim against these sovereign entities which issue them. How much is a share worth in a bankrupt corporation? How much is a dollar worth, when it is issued by an obviously bankrupt debtor?

However we don’t need to go down that road, since it would inevitably lead to a debate between the phony, official numbers of the United State’s “national debt”, and the $200+ trillion in debts and liabilities which it would be forced to acknowledge if it had to follow the same accounting rules as all U.S. corporations are required by law to use.

There is a much simpler and more direct way to demonstrate the worthlessness of the U.S. dollar, one which is beyond any possible debate. As a tautology, anything which can be obtained in infinite quantities and produced at zero cost must be worthless. If this were not the case, then one would simply produce an infinite quantity of that item – and thenexchange it for all the goods (and services) in the entire world.

With most of our fiat currencies now being conjured into existence electronically, this is the ultimate example of an infinite quantity/zero cost item…with one exception. Since all of this funny-money is borrowed into existence, the bankers were previously able to claim that in fact this was not a “zero cost” item – because of the debt/interest attached to each currency unit.

However that argument, the only basis for claiming that the bankers’ fiat currency had any value whatsoever evaporated the day that the U.S. began its permanent era of 0% interest rates. On that day the U.S. dollar fully became a zero cost/infinite quantity item – and indisputably worthless as a basic proposition of logic.

Why do people think B.S. Bernanke attempted to peddle the myth of an “exit strategy” – i.e. an end to 0% interest rates – for nearly three years, before finally being forced to abandon that absurd pretense? Because he and the rest of the banking cabal are terrified that someone would stand up (as I have done on several occasions) and announce that “the Emperor is wearing no clothes.”

At the end of Tulipmania 400 years ago; one day a single tulip could be exchanged to buy a house. The next day that tulip was merely a flower. The tulip itself was unchanged. All that did change was that the mass delusion that tulips were items of considerable value suddenly and collectively evaporated. It is one of the reasons why every fiat currency ever created has gone to zero (or simply been removed from circulation before it hit zero). It is one of the reasons why they tend to go to zero very, very quickly – more commonly known as “hyperinflation”.

The moment we accept the logical fact that these fiat currencies are already worthless we see the absurdity of attempting to price valuable assets (like gold and silver) in paper which has no meaning. If I announce that in hyperinflation-ravaged Zimbabwe that an ounce of gold is “worth” $2.5 trillion Zimbabwe dollars, does that actually mean anything to anyone?

Sadly, we have collectively been so completely brainwashed (over the past century) that we are now almost incapable of conceiving a world which is not priced in paper. However, go back little more than a century (and for all the centuries preceding it throughout history) and we encounter a world virtually the mirror-opposite of our own.

In that world, everything was “priced” in gold and silver. The only way that mere paper could ever acquire value was as a certificate directly backed by gold or silver. The concept of a world where everything was “priced” in fiat paper which was backed by nothing (and effectively worthless) would have been a proposition much too ludicrous for any of our ancestors to consider – except during their own, brief, disastrous experiments with such paper.

As our fiat currencies begin their final descent into history’s dust-bin of failed paper, we are entering a period of transition and re-education. We must reintroduce into our minds the concept of once again pricing goods and services in terms of items of enduring value (i.e. real money).

There is no space here to explain (yet one more time) why gold and silver are “money” while our paper currencies are obviously not. Readers will have to refer to previous explanations of the definition of money. Once readers have completed this second step in their mental transition, they are ready to return to a world of real money – and rational “value”.

How many ounces of gold does a house cost? How many pairs of shoes could one purchase with an ounce of silver? When the “dimes” and “quarters” in our wallets once again contain actual silver (real money), we could once again buy a chocolate bar with a dime (as we could only a few decades ago) – and perhaps several.

This mental transition will naturally seem like a very intimidating concept to many, just as the Dutch couldn’t conceive of a world which was not “priced” in tulips – the day before Tulipmania ended. Here it’s important to make readers explicitly aware of the penalties for being one of the last to make the transition away from the bankers’ world of worthless, fraudulent paper.

If you were a Dutch resident who exchanged his/her tulips for items of real value before the day Tulipmania ended, you fully protected/insured your wealth. If you did not do so, you were completely wiped-out financially – with nothing to console you except a handful of pretty flowers.

If we exchange our dollars (or euros) for hard assets (i.e. silver and gold) now, before they inevitably suffer the same fate as the Zimbabwe dollar, we can still protect what is left of our wealth. If we attempt to exchange our paper the day after our own “Tulipmania” comes to an end we will find we are holding nothing but an inferior brand of toilet paper.

It is because the speed at which this final collapse will occur is so unpredictable that it has become a Fool’s Game attempting to guess short-term prices for silver and gold – and now even predicting longer term prices as well. Indeed, this is now so speculative that it only makes sense to do so in a “best-case scenario” for the bankers’ paper (i.e. where they are able to delay the collapse of their paper with the maximum amount of success). Obviously in their worst-case scenario the paper would be absolutely worthless, inferring infinite prices for gold, silver, and other hard assets.

Thus my worst-case scenario for the price of gold is a price of at least $5,000/oz within the next 2 – 5 years. Similarly, my prediction for the price of silver would be a minimum of $200/oz within that same 2 – 5 year time horizon. Some will accuse me of making a “prediction” so loose as to be useless. I make no apologies.

Read more: My Last Forecast on Silver and Gold Prices

Related Articles:

-

Bernanke Strikes Again!

Submitted by Ben Traynor | BullionVault

Thursday, 7 June 2012

-

Another big fall for gold as the Fed chairman appears before Congress…

SIX DAYS after they climbed back above $1600 an ounce, gold prices dropped back below that level on Thursday, as Federal Reserve chairman Ben Bernanke appeared before Congress at the Joint Economic Committee.

This is not the first time we’ve seen this. Back on February 29, gold fell $100 an ounce while Bernanke was testifying before the House Financial Services Committee. What on earth is the man saying to have such an adverse impact on gold prices?

Well, on the two occasions cited above, it wasn’t what he said, but what he failed to say that did the damage. In short, Bernanke failed to make any explicit promises of further Fed quantitative easing.

Last Friday, gold shot up 5% in Dollar terms, following disappointing US jobs and manufacturing data. Clearly, some traders were betting that the Fed would respond by announcing further stimulus, a bet that failed to pay off. Bernanke’s reticence in this regard is hardly surprising, though. It’s what central bankers do: they say as little as they can get away

with to keep as many options open as they can.

They also talk to each other, and it seems the major central bankers have agreed a common script, one which has as its central theme a focus on the failings of fiscal policymakers (i.e. politicians). Here is European Central Bank president Mario Draghi speaking on Wednesday:

Some of these problems in the Euro area have nothing to do with monetary policy. That is what we have to be aware of and I do not think it would be right for monetary policy to compensate for other institutions’ lack of action.

And here’s Bernanke a day later:

…under current policies and reasonable economic assumptions, the [Congressional Budget Office] projects that the structural budget gap and the ratio of federal debt to GDP will trend upward thereafter, in large part reflecting rapidly escalating health expenditures and the aging of the population. This dynamic is clearly unsustainable…fiscal policy must be placed on a sustainable path that eventually results in a stable or declining ratio of federal debt to GDP.

Translation: don’t look at us.

Central bankers are trying to put pressure on their political masters to deal with problems that are beyond the scope of monetary policy. It is these problems, they argue, that are at the root of the current crisis.

It was put to Bernanke by JEC vice chairman Kevin Brady that the Fed itself is encouraging political inaction by keeping QE3, a potential third round of quantitative easing, on the table.

In other words, the belief that the Fed is on standby to combat any crisis makes a crisis more likely, reducing as it does the incentive to take difficult preventative action.

The trouble is, the Fed and other central banks daren’t row too far back from talk of stimulus for fear that this will provoke a crisis. This is why Bernanke made it clear the option was on the table, while also saying “Look over there” and pointing at the so-called fiscal cliff – the combination of tax cut expiries and mandated spending cuts that await the US should lawmakers fail to reach agreements to prevent them (a genuine risk in an election year).

So we are at an impasse, meaning gold prices are susceptible to marginal sentiment and bets on what monetary policymakers will do next. This has been the case all year. For example, gold prices rallied in January after the Fed published projections showing its policymakers expected near-zero interest rates until late 2014. Gold also saw a jump in

March as Bernanke reiterated the need for accommodative policies.

The truth is, though, that there has been little rhyme or reason to these moves. If you look at what Bernanke actually said on each occasion, it is pretty much a rehash of what he’s said before. Fed statements since the start of the year have all broadly said this: “We’re not out of the woods, we’ll keep an eye on things, and we’ll do as we see fit.”

Details have changed, depending on the newsflow, but that’s all. Here’s an extract from Thursday’s testimony:

…the situation in Europe poses significant risks to the US financial system and economy and must be monitored closely. As always, the Federal Reserve remains prepared to take action as needed to protect the US financial system and economy in the event that financial stresses escalate.

Later on, Bernanke said there is “no justification” for fears that QE could spark inflation. Taking these comments together, one could make a case that the Fed are about to push the button marked ‘More Stimulus’. But of course, traders had already jumped to that conclusion last Friday, and so were forced to ‘unjump’.

The truth is, we don’t know when or if we will see more QE, and we doubt anyone at the Fed does either. QE is not about economic stimulus. Not really. It may be packaged as a way of boosting growth, but in our view its real aim is to fight rises in the banking sector.

This is where it gets difficult for gold investors. It may be that the Fed, along with other central banks, are holding fire until the banking stresses in Europe become really acute. As we saw last November and December, a banking crisis can be accompanied by sharp falls in gold prices, as gold is sold or leased to raise Dollars, increasing its immediate supply and putting downward pressure on prices.

Indeed, along with the disappointment that Bernanke was note more dovish following last week’s economic news, another possible explanation for gold’s fall this week is that uncertainty over QE raises the risk of a sudden funding crunch.

Another factor to bear in mind is inflation expectations. Bernanke said on Thursday that these are “quite well anchored”. But some argue that they are still too high to make QE an immediate prospect, with 5-Year breakeven rates – the difference in yield between inflation- linked and nominal debt – still too high:

There remains a significant chance we will yet see more Fed QE. But things may need to get quite a bit worse first. In the meantime, the only clues we are likely to get are those we can glean from the Orwellian radio static of central banker doublespeak.

Or, if you’re a long run investor, you could just ignore the noise being made by gold prices and crack open a beer…

Ben Traynor

BullionVault

Like this:

If you stop printing, another massive economic crash will occur

Robert Wenzel: Economic Policy Journal

My Speech Delivered at the New York Federal Reserve Bank

At the invitation of the New York Federal Reserve Bank, I spoke and had lunch in the bank’s Liberty Room. Below are my prepared remarks.

Thank you very much for inviting me to speak here at the New York Federal Reserve Bank.

Intellectual discourse is, of course, extraordinarily valuable in reaching truth. In this sense, I welcome the opportunity to discuss my views on the economy and monetary policy and how they may differ with those of you here at the Fed.

That said, I suspect my views are so different from those of you here today that my comments will be a complete failure in convincing you to do what I believe should be done, which is to close down the entire Federal Reserve System

My views, I suspect, differ from beginning to end. From the proper methodology to be used in the science of economics, to the manner in which the macro-economy functions, to the role of the Federal Reserve, and to the accomplishments of the Federal Reserve, I stand here confused as to how you see the world so differently than I do.

I simply do not understand most of the thinking that goes on here at the Fed and I do not understand how this thinking can go on when in my view it smacks up against reality.

Please allow me to begin with methodology, I hold the view developed by such great economic thinkers as Ludwig von Mises, Friedrich Hayek and Murray Rothbard that there are no constants in the science of economics similar to those in the physical sciences.

In the science of physics, we know that water freezes at 32 degrees. We can predict with immense accuracy exactly how far a rocket ship will travel filled with 500 gallons of fuel. There is preciseness because there are constants, which do not change and upon which equations can be constructed..

There are no such constants in the field of economics since the science of economics deals with human action, which can change at any time. If potato prices remain the same for 10 weeks, it does not mean they will be the same the following day. I defy anyone in this room to provide me with a constant in the field of economics that has the same unchanging constancy that exists in the fields of physics or chemistry.

And yet, in paper after paper here at the Federal Reserve, I see equations built as though constants do exist. It is as if one were to assume a constant relationship existed between interest rates here and in Russia and throughout the world, and create equations based on this belief and then attempt to trade based on these equations. That was tried and the result was the blow up of the fund Long Term Capital Management, a blow up that resulted in high level meetings in this very building.

It is as if traders assumed a given default rate was constant for subprime mortgage paper and traded on that belief. Only to see it blow up in their faces, as it did, again, with intense meetings being held in this very building.

Yet, the equations, assuming constants, continue to be published in papers throughout the Fed system. I scratch my head.

I also find curious the general belief in the Keynesian model of the economy that somehow results in the belief that demand drives the economy, rather than production. I look out at the world and see iPhones, iPads, microwave ovens, flat screen televisions, which suggest to me that it is production that boosts an economy. Without production of these things and millions of other items, where would we be? Yet, the Keynesians in this room will reply, “But you need demand to buy these products.” And I will reply, “Do you not believe in supply and demand? Do you not believe that products once made will adjust to a market clearing price?”

Further , I will argue that the price of the factors of production will adjust to prices at the consumer level and that thus the markets at all levels will clear. Again do you believe in supply and demand or not?

I scratch my head that somehow most of you on some academic level believe in the theory of supply and demand and how market setting prices result, but yet you deny them in your macro thinking about the economy.

You will argue with me that prices are sticky on the downside, especially labor prices and therefore that you must pump money to get the economy going. And, I will look on in amazement as your fellow Keynesian brethren in the government create an environment of sticky non-downward bending wages.

The economist Robert Murphy reports that President Herbert Hoover continually pressured businessmen to not lower wages.[1]

He quoted Hoover in a speech delivered to a group of businessmen:

In this country there has been a concerted and determined effort on the part of government and business… to prevent any reduction in wages.

He then reports that FDR actually outdid Hoover by seeking to “raise wages rates rather than merely put a floor under them.”

I ask you, with presidents actively conducting policies that attempt to defy supply and demand and prop up wages, are you really surprised that wages were sticky downward during the Great Depression?

In present day America, the government focus has changed a bit. In the new focus, the government attempts much more to prop up the unemployed by extended payments for not working. Is it really a surprise that unemployment is so high when you pay people not to work.? The 2010 Nobel Prize was awarded to economists for their studies which showed that, and I quote from the Nobel press release announcing the award:

One conclusion is that more generous unemployment benefits give rise to higher unemployment and longer search times.[2]

Don’t you think it would make more sense to stop these policies which are a direct factor in causing unemployment, than to add to the mess and devalue the currency by printing more money?

I scratch my head that somehow your conclusions about unemployment are so different than mine and that you call for the printing of money to boost “demand”. A call, I add, that since the founding of the Federal Reserve has resulted in an increase of the money supply by 12,230%.

I also must scratch my head at the view that the Federal Reserve should maintain a stable price level. What is wrong with having falling prices across the economy, like we now have in the computer sector, the flat screen television sector and the cell phone sector? Why, I ask, do you want stable prices? And, oh by the way, how’s that stable price thing going for you here at the Fed?

Since the start of the Fed, prices have increased at the consumer level by 2,241% [3]. that’s not me misspeaking, I will repeat, since the start of the Fed, prices have increased at the consumer level by 2,241%.

So you then might tell me that stable prices are only a secondary goal of the Federal Reserve and that your real goal is to prevent serious declines in the economy but, since the start of the Fed, there have been 18 recessions including the Great Depression and the most recent Great Recession. These downturns have resulted in stock market crashes, tens of millions of unemployed and untold business bankruptcies.

I scratch my head and wonder how you think the Fed is any type of success when all this has occurred.

I am especially confused, since Austrian business cycle theory (ABCT), developed by Mises, Hayek and Rothbard, has warned about all these things. According to ABCT, it is central bank money printing that causes the business cycle and, again you here at the Fed have certainly done that by increasing the money supply. Can you imagine the distortions in the economy caused by the Fed by this massive money printing?

According to ABCT, if you print money those sectors where the money goes will boom, stop printing and those sectors will crash. Fed printing tends to find its way to Wall Street and other capital goods sectors first, thus it is no surprise to Austrian school economists that the crashes are most dramatic in these sectors, such as the stock market and real estate sectors. The economist Murray Rothbard in his book America’s Great Depression [4] went into painstaking detail outlining how the changes in money supply growth resulted in the Great Depression.

On a more personal level, as the recent crisis was developing here, I warned throughout the summer of 2008 of the impending crisis. On July 11, 2008 at EconomicPolicyJournal.com, I wrote[5]:

SUPER ALERT: Dramatic Slowdown In Money Supply GrowthAfter growing at near double digit rates for months, money growth has slowed dramatically. Annualized money growth over the last 3 months is only 5.2%. Over the last two months, there has been zero growth in the M2NSA money measure.This is something that must be watched carefully. If such a dramatic slowdown continues, a severe recession is inevitable.

We have never seen such a dramatic change in money supply growth from a double digit climb to 5% growth. Does Bernanke have any clue as to what the hell he is doing?

I have previously noted that over the last two months money supply has been collapsing. M2NSA has gone from double digit growth to nearly zero growth .

A review of the credit situation appears worse. According to recent Fed data, for the 13 weeks ended June 25, bank credit (securities and loans) contracted at an annual rate of 7.9%.

There has been a minor blip up since June 25 in both credit growth and M2NSA, but the growth rates remain extremely slow.

If a dramatic turnaround in these numbers doesn’t happen within the next few weeks, we are going to have to warn of a possible Great Depression style downturn.

I would like to provide a brief update on the outlook for the economy and policy, beginning with the prospects for growth. Despite the unwelcome rise in the unemployment rate that was reported last week, the recent incoming data, taken as a whole, have affected the outlook for economic activity and employment only modestly. Indeed, although activity during the current quarter is likely to be weak, the risk that the economy has entered a substantial downturn appears to have diminished over the past month or so. Over the remainder of 2008, the effects of monetary and fiscal stimulus, a gradual ebbing of the drag from residential construction, further progress in the repair of financial and credit markets, and still-solid demand from abroad should provide some offset to the headwinds that still face the economy.

I believe the Great Recession that followed is still fresh enough in our minds so it is not necessary to recount in detail as to whose forecast, mine or the chairman’s, was more accurate.

I am also confused by many other policy making steps here at the Federal Reserve. There have been more changes in monetary policy direction during the Bernanke era then at any other time in the modern era of the Fed. Not under Arthur Burns, not under G. William Miller, not under Paul Volcker, not under Alan Greenspan have there been so many dramatically shifting Fed monetary policy moves. Under Chairman Bernanke there have been significant changes in direction of the money supply growth FIVE different times. Thus, for me, I am not at all surprised at the current stop and go economy. The current erratic monetary policy makes it exceedingly difficult for businessmen to make any long term plans. Indeed, in my own Daily Alert on the economy [8] I find it extremely difficult to give long term advice, when in short periods I have seen three month annualized M2 money growth go from near 20% to near zero, and then in another period see it go from 25% to 6% . [9]

I am also confused by many of the monetary programs instituted by Chairman Bernanke. For example, Operation Twist.

This is not the first time an Operation Twist was tried. an Operation Twist was tried in 1961, at the start of the Kennedy Administration [10] A paper [11] was written by three Federal Reserve economists in 2004 that, in part, examined the 1960′s Operation Twist

Their conclusion (My bold):

A second well-known historical episode involving the attempted manipulation of the term structure was so-called Operation Twist. Launched in early 1961 by the incoming Kennedy Administration, Operation Twist was intended to raise short-term rates (thereby promoting capital inflows and supporting the dollar) while lowering, or at least not raising, long-term rates. (Modigliani and Sutch 1966)…. The two main actions of Operation Twist were the use of Federal Reserve open market operations and Treasury debt management operations.. Operation Twist is widely viewed today as having been a failure, largely due to classic work by Modigliani and Sutch….

However, Modigliani and Sutch also noted that Operation Twist was a relatively small operation, and, indeed, that over a slightly longer period the maturity of outstanding government debt rose significantly, rather than falling…Thus, Operation Twist does not seem to provide strong evidence in either direction as to the possible effects of changes in the composition of the central bank’s balance sheet….

We believe that our findings go some way to refuting the strong hypothesis that nonstandard policy actions, including quantitative easing and targeted asset purchases, cannot be successful in a modern industrial economy. However, the effects of such policies remain quantitatively quite uncertain.

One of the authors of this 2004 paper was Federal Reserve Chairman Bernanke. Thus, I have to ask, what the hell is Chairman Bernanke doing implementing such a program, since it is his paper that states it was a failure according to Modigliani, and his paper implies that a larger test would be required to determine true performance.

I ask, is the Chairman using the United States economy as a lab with Americans as the lab rats to test his intellectual curiosity about such things as Operation Twist?

Further, I am very confused by the response of Chairman Bernanke to questioning by Congressman Ron Paul. To a seemingly near off the cuff question by Congressman Paul on Federal Reserve money provided to the Watergate burglars, Chairman Bernanke contacted the Inspector General’s Office of the Federal Reserve and requested an investigation [12]. Yet, the congressman has regularly asked about the gold certificates held by the Federal Reserve [13] and whether the gold at Fort Knox backing up the certificates will be audited. Yet there have been no requests by the Chairman to the Treasury for an audit of the gold.This I find very odd. The Chairman calls for a major investigation of what can only be an historical point of interest but fails to seek out any confirmation on a point that would be of vital interest to many present day Americans.

In this very building, deep in the underground vaults, sits billions of dollars of gold, held by the Federal Reserve for foreign governments. The Federal Reserve gives regular tours of these vaults, even to school children. [14] Yet, America’s gold is off limits to seemingly everyone and has never been properly audited. Doesn’t that seem odd to you? If nothing else, does anyone at the Fed know the quality and fineness of the gold at Fort Knox?

In conclusion, it is my belief that from start to finish the Fed is a failure. I believe faulty methodology is used, I believe that the justification for the Fed, to bring price and economic stability, has never been a success. I repeat, prices since the start of the Fed have climbed by 2,241% and there have been over the same period 18 recessions. No one seems to care at the Fed about the gold supposedly backing up the gold certificates on the Fed balance sheet. The emperor has no clothes. Austrian Business cycle theorists are regularly ignored by the Fed, yet they have the best records with regard to spotting overall downturns, and further they specifically recognized the developing housing bubble. Let it not be forgotten that in 2004, two economists here at the New York Fed wrote a paper [15] denying there was a housing bubble. I responded to the paper [16] and wrote:

The faulty analysis by [these] Federal Reserve economists… may go down in financial history as the greatest forecasting error since Irving Fisher declared in 1929, just prior to the stock market crash, that stocks prices looked to be at a permanently high plateau.

Data released just yesterday, now show housing prices have crashed to 2002 levels. [17]

I will now give you more warnings about the economy.

The noose is tightening on your organization, vast amounts of money printing are now required to keep your manipulated economy afloat. It will ultimately result in huge price inflation, or, if you stop printing, another massive economic crash will occur. There is no other way out.

Again, thank you for inviting me. You have prepared food, so I will not be rude, I will stay and eat.

Let’s have one good meal here. Let’s make it a feast. Then I ask you, I plead with you, I beg you all, walk out of here with me, never to come back. It’s the moral and ethical thing to do. Nothing good goes on in this place. Let’s lock the doors and leave the building to the spiders, moths and four-legged rats.

-

Footnotes

[1] http://www.amazon.com/Politically-Incorrect-Guide-Depression-Guides/dp/1596980966/ref=sr_1_1?ie=UTF8&qid=1335313972&sr=8-1

[2] http://www.nobelprize.org/nobel_prizes/economics/laureates/2010/press.html

[3] ftp://ftp.bls.gov/pub/special.requests/cpi/cpiai.txt

[4] http://www.amazon.com/Americas-Great-Depression-Murray-Rothbard/dp/146793481X/ref=sr_1_1?ie=UTF8&qid=1335314537&sr=8-1

[5] http://www.economicpolicyjournal.com/2008/07/super-alert-dramatic-slowdown-in-money.html

[6] http://www.economicpolicyjournal.com/2008/07/alert-collapsing-credit.html

[7] http://www.federalreserve.gov/newsevents/speech/bernanke20080609a.htm

[8] http://www.economicpolicyjournal.com/2009/04/announcing-epj-quarterly-economic.html

[9]http://www.economicpolicyjournal.com/2008/07/super-alert-dramatic-slowdown-in-money.html

[10] http://www.frbsf.org/publications/economics/letter/2011/el2011-13.html

[11] http://www.federalreserve.gov/pubs/feds/2004/200448/200448pap.pdf

[12] http://www.huffingtonpost.com/2012/04/03/federal-reserve-watergate-iraqi-weapons_n_1400645.html

[13] http://www.federalreserve.gov/releases/h41/Current/

[14] http://www.newyorkfed.org/aboutthefed/visiting.html

[15] http://fednewyork.org/research/epr/04v10n3/0412mcca.pdf

[16] http://www.economicpolicyjournal.com/2012/02/checkmate-new-york-fed-as-totally.html

[17] http://www.nytimes.com/2012/04/25/business/economy/survey-shows-us-home-prices-still-weak.html

Special thanks to the following, who helped me research and collect data for this paper: Stephen Davis, Bob English, Jon Lyons, Ash Navabi, Joseph Nelson, Nick Nero, Antony Zegers

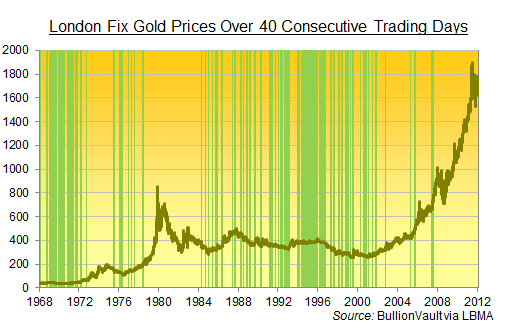

40 days and 40 nights of the quietest gold market since the crisis began…

Submitted by Ben Traynor | BullionVault

-

HOW COMMON is it for Gold Prices to be this range bound? asks Ben Traynor atBullionVault.

At Wednesday afternoon’s London Gold Fix, Dollar Gold Prices were $1648 an ounce. This marked the fortieth trading day in a row that gold fixed between $1600 and $1700.

The last PM Fix outside this range was on March 5 ($1705 an ounce). Spot GoldPrices did manage to poke their head above the $1700 mark later that same week, but since then gold has gone pretty much nowhere. Is it common to see such a protracted period of sideways trading?

One way of gauging how much (or indeed how little) Gold Prices have moved in that time is to calculate the coefficient of variation (CV) – simply the standard deviation divided by the mean average – and compare it with rolling 40 day periods.

The chart below does exactly that, going back to 1968, the year the London Gold Pool collapsed. The vertical green lines represent the final day of any 40 day period with a lower CV than the 40 trading days just gone, with the Gold Price shown over the top (left hand axis):

By the CV measure, gold has not had a quieter 40 days since mid-2007, right at the start of the financial crisis.

A block of six trading days – August 30 to September 6, 2007 – each marked the end of quieter 40-day periods than the one we have just had. There is a similar cluster of four days in July 2007.

As you can see from the chart, these days have tended to come in consecutive blocks – which makes sense since we are taking rolling statistical measures. This allows us to pick out specific quiet periods when Gold Prices were not really doing much.

Over the last 10 years, there have been only five 40-day periods quieter than the one we have just had – the two in 2007, another two in 2005, and one towards the end of 2002.

By contrast, the 1990s saw loads of periods quieter than the current one. So too did the late 1960s and early 1970s, as we would expect since gold was, until August 1971, still officially tied to the Dollar at $35 an ounce (though a two-tier market allowed for a fluctuating price for non-central bank transactions).

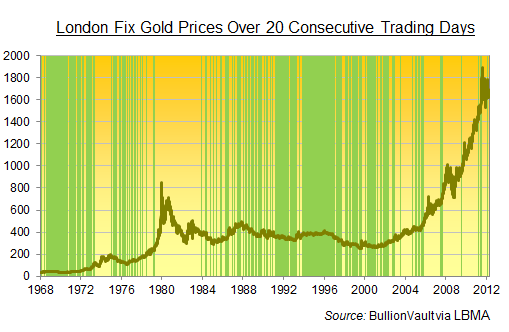

Of course, 40 trading days is a rather arbitrary span of time to pick. But similar patterns emerge when we look at other rolling periods.

Wednesday 2 May 2012 also marked the quietest 20 trading day period by the CV measure. Here’s the chart for rolling 20-day periods going back to 1968:

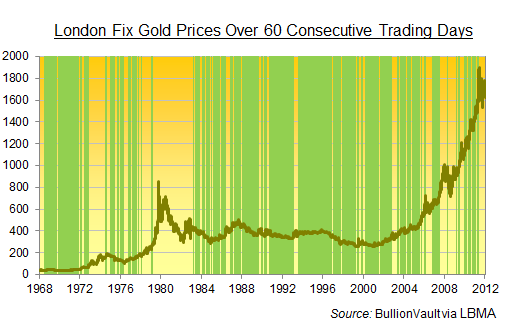

The quietest 60-day period so far this year was actually that ended on April 13. Nonetheless, for ease of comparison, here is the chart showing 60-day periods with lower CVs than the period ended Wednesday this week:

We can draw a few observations from the above:

- Gold Prices have rarely been this quiet since the current financial crisis began

- When the last bull market ended in 1980, it didn’t end quietly – hence the big gaps between the late 1970s and mid-1980s

- If history repeats, these relatively flat Gold Prices could be a precursor to the Big Move (as was the case in the mid-1970s), or they could herald a long, slow decline (see mid-to-late 1980s)

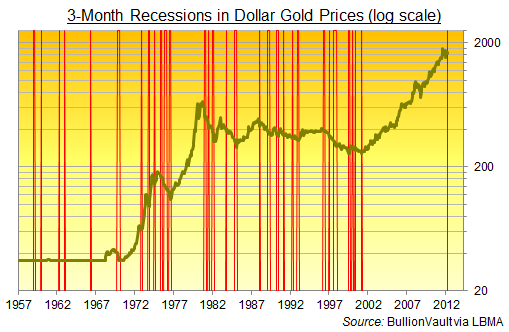

Something else happened this week. As my BullionVault colleague Adrian Ash notes, spot market Gold Prices on Monday ended a calendar month lower for the third month in a row – a rare event indeed in a bull market.

It is also worth checking out Adrian’s log scale chart (reproduced below), which shows that Gold Prices over the last ten years have made a much smaller proportionate gain (shown as the vertical distance moved) than they did in the ten years to 1980:

Putting this all together, both bulls and bears could make a case. The bulls might argue that it is just too quiet for this to be the beginning of a sustained downtrend, and that Gold Prices are taking a breather before making another move up.

Bears might counter that since this bull market has seen a gentler rise, it may well be followed by a gentler decline, which could be what we are seeing right now.

Ultimately, Gold Prices over the long run are determined by fundamentals. One of the key fundamentals is real interest rates i.e. nominal rates minus the rate of inflation. And the key central bank to watch is, of course, the Federal Reserve.

There have been signs in recent weeks that the US economy is picking up. This has dampened expectations of further quantitative easing, and has also raised the prospect that the Fed could raise its policy interest rate sooner than previously expected. Few would go so far as to declare the crisis over, but doubts have crept in about how accommodative the Fed will remain.

I believe this uncertainty is the main reason trading volumes have been low, and Gold Prices have been stuck in a range. It doesn’t help that we are headed towards summer, when the gold market tends to be much quieter (2011 notwithstanding).

If the tentative US recovery continues, more investors will likely surmise that QE will not happen, and that a rate hike will be sooner rather than later. On the other hand, if the recovery stalls, QE could shoot back up the agenda.

Sooner or later, Gold Prices will break out of this range. Whether it will a break higher or a break lower depends a great deal on the health of the US economy.

Buying Gold? Get the safest gold at the lowest prices with BullionVault…

Featured Reviews

16Oct: Jeff Clark (Casey Research)

$2,300 gold by January 2014

05Sep: Bill Murphy (GATA)

$50 silver by year end

13Aug: James Turk (GoldMoney)

We won’t see $1580 gold & $27 silver again

12Aug: Bill Murphy's source

We could see a 100% increase in 90 days.

03Aug: HSBC Analysts

Gold to rally above $1,900 by end 2012

05June: David Bond (SilverMiners)

Gold & Silver may bottom at $1,200 & $18

02June: Don Coxe (Coxe Advisors)

Europe to issue Gold-backed Euro Bonds within the next 3 months

21May: Gene Arensberg (GotGoldReport)

Gold and Silver are very close to a bottom, if one has not already been put in last week

>> More forecasts & forecast accuracy

Daily GOLD US$/oz

Daily SILVER US$/oz

More Gold Charts: 1 Month to 660 Years

More Silver Charts: 1 Month to 660 Years

Gold/Silver Ratio: 1 Month to 660 Years

Gold & Silver Priced in BitCoins

Click to enlarge.

BitCoin donation welcomed.

1NQ4LqE8yL6rfAqikDU8wLhHSm5fntsWxk

Gold & Silver Interviews (KWN)

Gold & Silver Interviews (KWN)

- Here Is What Will Fuel The Move Higher In Hard Assets October 27, 2012

- Greyerz - Two Absolutely Incredible & Key Gold Charts October 26, 2012

- Celente - It’s Not Just Germany’s Gold That’s Missing October 26, 2012

- What To Expect With Gold Assaulting $1,700 & Silver At $32 October 26, 2012

- James Turk - The Entire German Gold Hoard Is Gone October 25, 2012

- KWN Update - Here Is A Huge Key To The Markets October 25, 2012

- Currency Wars Continue To Rage & This Is Positive For Gold October 25, 2012

- Central Planners Greatest Fear, Possible Surprises & Gold October 24, 2012

Finance & Economics

- Guest Post: GDP - The Warning Signs From Exports October 28, 2012 Tyler Durden

- On Europe And The Future Of International Relations October 28, 2012 Tyler Durden

- Meanwhile In Japan... October 27, 2012 Tyler Durden

- Bundesbank's Official Statment On Where It's Gold Is (And Isn't) October 27, 2012 Tyler Durden

- A CRuSTY CRiTTER AND aN INTeRPLaNeTaRY BuLL SHiTTeR... October 27, 2012 williambanzai7

- As Thousands Of Italians March Against Austerity On "No Monti Day", Berlusconi Threatens To Scuttle Monti Government October 27, 2012 Tyler Durden

- "Go South, Young Man": The Africa Scramble October 27, 2012 Tyler Durden

- Too Much Rain Will Kill Ya October 27, 2012 Bruce Krasting

From Canada to NZ, and everywhere in between, people are waking up!

-

From Canada to NZ, and everywhere in between, people are waking up! Waking up to the fact that the existing global monetary & banking system is seriously flawed. Many would even go as far as saying it is a fraud. Unless governments the world over change the way national currencies are created and managed, it is a mathematical certainty the system will collapse like a house of cards. Here’s a small collection of voices explaining the flawed or fraudulent system together with their calls for change and your personal action.

If all this is new to you, it’ll do you good to study the materials in the order they are listed below.

-

Share this:

Like this: