Archive

Collapse At Hand

-

Republished with permission from Dr. Roberts | Institute for Political Economy

[Charts inserted by editor]

Collapse At Hand

By Dr. Paul Craig Roberts | June 5, 2012

Ever since the beginning of the financial crisis and quantitative easing, the question has been before us: How can the Federal Reserve maintain zero interest rates for banks and negative real interest rates for savers and bond holders when the US government is adding $1.5 trillion to the national debt every year via its budget deficits? Not long ago the Fed announced that it was going to continue this policy for another 2 or 3 years. Indeed, the Fed is locked into the policy. Without the artificially low interest rates, the debt service on the national debt would be so large that it would raise questions about the US Treasury’s credit rating and the viability of the dollar, and the trillions of dollars in Interest Rate Swaps and other derivatives would come unglued.

Ever since the beginning of the financial crisis and quantitative easing, the question has been before us: How can the Federal Reserve maintain zero interest rates for banks and negative real interest rates for savers and bond holders when the US government is adding $1.5 trillion to the national debt every year via its budget deficits? Not long ago the Fed announced that it was going to continue this policy for another 2 or 3 years. Indeed, the Fed is locked into the policy. Without the artificially low interest rates, the debt service on the national debt would be so large that it would raise questions about the US Treasury’s credit rating and the viability of the dollar, and the trillions of dollars in Interest Rate Swaps and other derivatives would come unglued.

In other words, financial deregulation leading to Wall Street’s gambles, the US government’s decision to bail out the banks and to keep them afloat, and the Federal Reserve’s zero interest rate policy have put the economic future of the US and its currency in an untenable and dangerous position. It will not be possible to continue to flood the bond markets with $1.5 trillion in new issues each year when the interest rate on the bonds is less than the rate of inflation. Everyone who purchases a Treasury bond is purchasing a depreciating asset. Moreover, the capital risk of investing in Treasuries is very high. The low interest rate means that the price paid for the bond is very high. A rise in interest rates, which must come sooner or later, will collapse the price of the bonds and inflict capital losses on bond holders, both domestic and foreign.

The question is: when is sooner or later? The purpose of this article is to examine that question.

Let us begin by answering the question: how has such an untenable policy managed to last this long?

A number of factors are contributing to the stability of the dollar and the bond market. A very important factor is the situation in Europe. There are real problems there as well, and the financial press keeps our focus on Greece, Europe, and the euro. Will Greece exit the European Union or be kicked out? Will the sovereign debt problem spread to Spain, Italy, and essentially everywhere except for Germany and the Netherlands?

Will it be the end of the EU and the euro? These are all very dramatic questions that keep focus off the American situation, which is probably even worse.

The Treasury bond market is also helped by the fear individual investors have of the equity market, which has been turned into a gambling casino by high-frequency trading.

High-frequency trading is electronic trading based on mathematical models that make the decisions. Investment firms compete on the basis of speed, capturing gains on a fraction of a penny, and perhaps holding positions for only a few seconds. These are not long-term investors. Content with their daily earnings, they close out all positions at the end of each day.

High-frequency trades now account for 70-80% of all equity trades. The result is major heartburn for traditional investors, who are leaving the equity market. They end up in Treasuries, because they are unsure of the solvency of banks who pay next to nothing for deposits, whereas 10-year Treasuries will pay about 2% nominal, which means, using the official Consumer Price Index, that they are losing 1% of their capital each year. Using John Williams’ (shadowstats.com) correct measure of inflation, they are losing far more. Still, the loss is about 2 percentage points less than being in a bank, and unlike banks, the Treasury can have the Federal Reserve print the money to pay off its bonds. Therefore, bond investment at least returns the nominal amount of the investment, even if its real value is much lower. (For a description of High-frequency trading, see: http://en.wikipedia.org/wiki/High_frequency_trading )

The presstitute financial media tells us that flight from European sovereign debt, from the doomed euro, and from the continuing real estate disaster into US Treasuries provides funding for Washington’s $1.5 trillion annual deficits. Investors influenced by the financial press might be responding in this way. Another explanation for the stability of the Fed’s untenable policy is collusion between Washington, the Fed, and Wall Street. We will be looking at this as we progress.

Unlike Japan, whose national debt is the largest of all, Americans do not own their own public debt. Much of US debt is owned abroad, especially by China, Japan, and OPEC, the oil exporting countries. This places the US economy in foreign hands. If China, for example, were to find itself unduly provoked by Washington, China could dump up to $2 trillion in US dollar-dominated assets on world markets. All sorts of prices would collapse, and the Fed would have to rapidly create the money to buy up the Chinese dumping of dollar-denominated financial instruments.

The dollars printed to purchase the dumped Chinese holdings of US dollar assets would expand the supply of dollars in currency markets and drive down the dollar exchange rate. The Fed, lacking foreign currencies with which to buy up the dollars would have to appeal for currency swaps to sovereign debt-troubled Europe for euros, to Russia, surrounded by the US missile system, for rubles, to Japan, a country over its head in American commitment, for yen, in order to buy up the dollars with euros, rubles, and yen.

These currency swaps would be on the books, unredeemable and making additional use of such swaps problematical. In other words, even if the US government can pressure its allies and puppets to swap their harder currencies for a depreciating US currency, it would not be a repeatable process. The components of the American Empire don’t want to be in dollars any more than do the BRICS.

However, for China, for example, to dump its dollar holdings all at once would be costly as the value of the dollar-denominated assets would decline as they dumped them. Unless China is faced with US military attack and needs to defang the aggressor, China as a rational economic actor would prefer to slowly exit the US dollar. Neither do Japan, Europe, nor OPEC wish to destroy their own accumulated wealth from America’s trade deficits by dumping dollars, but the indications are that they all wish to exit their dollar holdings.

Unlike the US financial press, the foreigners who hold dollar assets look at the annual US budget and trade deficits, look at the sinking US economy, look at Wall Street’s uncovered gambling bets, look at the war plans of the delusional hegemon and conclude: “I’ve got to carefully get out of this.”

US banks also have a strong interest in preserving the status quo. They are holders of US Treasuries and potentially even larger holders. They can borrow from the Federal Reserve at zero interest rates and purchase 10-year Treasuries at 2%, thus earning a nominal profit of 2% to offset derivative losses. The banks can borrow dollars from the Fed for free and leverage them in derivative transactions. As Nomi Prins puts it, the US banks don’t want to trade against themselves and their free source of funding by selling their bond holdings. Moreover, in the event of foreign flight from dollars, the Fed could boost the foreign demand for dollars by requiring foreign banks that want to operate in the US to increase their reserve amounts, which are dollar based.

I could go on, but I believe this is enough to show that even actors in the process who could terminate it have themselves a big stake in not rocking the boat and prefer to quietly and slowly sneak out of dollars before the crisis hits. This is not possible indefinitely as the process of gradual withdrawal from the dollar would result in continuous small declines in dollar values that would end in a rush to exit, but Americans are not the only delusional people.

The very process of slowly getting out can bring the American house down. The BRICS-Brazil, the largest economy in South America, Russia, the nuclear armed and energy independent economy on which Western Europe (Washington’s NATO puppets) are dependent for energy, India, nuclear armed and one of Asia’s two rising giants, China, nuclear armed, Washington’s largest creditor (except for the Fed), supplier of America’s manufactured and advanced technology products, and the new bogyman for the military-security complex’s next profitable cold war, and South Africa, the largest economy in Africa-are in the process of forming a new bank. The new bank will permit the five large economies to conduct their trade without use of the US dollar.

In addition, Japan, an American puppet state since WWII, is on the verge of entering into an agreement with China in which the Japanese yen and the Chinese yuan will be directly exchanged. The trade between the two Asian countries would be conducted in their own currencies without the use of the US dollar. This reduces the cost of foreign trade between the two countries, because it eliminates payments for foreign exchange commissions to convert from yen and yuan into dollars and back into yen and yuan.

Moreover, this official explanation for the new direct relationship avoiding the US dollar is simply diplomacy speaking. The Japanese are hoping, like the Chinese, to get out of the practice of accumulating ever more dollars by having to park their trade surpluses in US Treasuries. The Japanese US puppet government hopes that the Washington hegemon does not require the Japanese government to nix the deal with China.

Now we have arrived at the nitty and gritty. The small percentage of Americans who are aware and informed are puzzled why the banksters have escaped with their financial crimes without prosecution. The answer might be that the banks “too big to fail” are adjuncts of Washington and the Federal Reserve in maintaining the stability of the dollar and Treasury bond markets in the face of an untenable Fed policy.

Let us first look at how the big banks can keep the interest rates on Treasuries low, below the rate of inflation, despite the constant increase in US debt as a percent of GDP-thus preserving the Treasury’s ability to service the debt.

The imperiled banks too big to fail have a huge stake in low interest rates and the success of the Fed’s policy. The big banks are positioned to make the Fed’s policy a success. JPMorgan Chase and other giant-sized banks can drive down Treasury interest rates and, thereby, drive up the prices of bonds, producing a rally, by selling Interest Rate Swaps (IRSwaps).

A financial company that sells IRSwaps is selling an agreement to pay floating interest rates for fixed interest rates. The buyer is purchasing an agreement that requires him to pay a fixed rate of interest in exchange for receiving a floating rate.

The reason for a seller to take the short side of the IRSwap, that is, to pay a floating rate for a fixed rate, is his belief that rates are going to fall. Short-selling can make the rates fall, and thus drive up the prices of Treasuries. When this happens, as these charts illustrate, there is

“U.S. Treasury Bond Teetering Tower Of Babel, Fed Stuck At 0% Forever” Jim Willie

“U.S. Treasury Bond Teetering Tower Of Babel, Fed Stuck At 0% Forever” Jim Willie

a rally in the Treasury bond market that the presstitute financial media attributes to “flight to the safe haven of the US dollar and Treasury bonds.” In fact, the circumstantial evidence (see the charts in the link above) is that the swaps are sold by Wall Street whenever the Federal Reserve needs to prevent a rise in interest rates in order to protect its otherwise untenable policy. The swap sales create the impression of a flight to the dollar, but no actual flight occurs. As the IRSwaps require no exchange of any principal or real asset, and are only a bet on interest rate movements, there is no limit to the volume of IRSwaps.

This apparent collusion suggests to some observers that the reason the Wall Street banksters have not been prosecuted for their crimes is that they are an essential part of the Federal Reserve’s policy to preserve the US dollar as world currency. Possibly the collusion between the Federal Reserve and the banks is organized, but it doesn’t have to be. The banks are beneficiaries of the Fed’s zero interest rate policy. It is in the banks’ interest to support it. Organized collusion is not required.

Let us now turn to gold and silver bullion. Based on sound analysis, Gerald Celente and other gifted seers predicted that the price of gold would be $2000 per ounce by the end of last year. Gold and silver bullion continued during 2011 their ten-year rise, but in 2012 the price of gold and silver have been knocked down, with gold being $350 per ounce off its $1900 high.

In view of the analysis that I have presented, what is the explanation for the reversal in bullion prices? The answer again is shorting. Some knowledgeable people within the financial sector believe that the Federal Reserve (and perhaps also the European Central Bank) places short sales of bullion through the investment banks, guaranteeing any losses by pushing a key on the computer keyboard, as central banks can create money out of thin air.

Insiders inform me that as a tiny percent of those on the buy side of short sells actually want to take delivery on the gold or silver bullion, and are content with the financial money settlement, there is no limit to short selling of gold and silver. Short selling can actually exceed the known quantity of gold and silver.

Some who have been watching the process for years believe that government-directed short-selling has been going on for a long time. Even without government participation, banks can control the volume of paper trading in gold and profit on the swings that they create. Recently short selling is so aggressive that it not merely slows the rise in bullion prices but drives the price down. Is this aggressiveness a sign that the rigged system is on the verge of becoming unglued?

In other words, “our government,” which allegedly represents us, rather than the powerful private interests who elect “our government” with their multi-million dollar campaign contributions, now legitimized by the Republican Supreme Court, is doing its best to deprive us mere citizens, slaves, indentured servants, and “domestic extremists” from protecting ourselves and our remaining wealth from the currency debauchery policy of the Federal Reserve. Naked short selling prevents the rising demand for physical bullion from raising bullion’s price.

Jeff Nielson explains another way that banks can sell bullion shorts when they own no bullion. (See, http://www.gold-eagle.com/editorials_08/nielson102411.html) Nielson says that JP Morgan is the custodian for the largest long silver fund while being the largest short-seller of silver. Whenever the silver fund adds to its bullion holdings, JP Morgan shorts an equal amount. The short selling offsets the rise in price that would result from the increase in demand for physical silver. Nielson also reports that bullion prices can be suppressed by raising margin requirements on those who purchase bullion with leverage. The conclusion is that bullion markets can be manipulated just as can the Treasury bond market and interest rates.

How long can the manipulations continue? When will the proverbial hit the fan?

If we knew precisely the date, we would be the next mega-billionaires.

Here are some of the catalysts waiting to ignite the conflagration that burns up the Treasury bond market and the US dollar:

A war, demanded by the Israeli government, with Iran, beginning with Syria, that disrupts the oil flow and thereby the stability of the Western economies or brings the US and its weak NATO puppets into armed conflict with Russia and China. The oil spikes would degrade further the US and EU economies, but Wall Street would make money on the trades.

An unfavorable economic statistic that wakes up investors as to the true state of the US economy, a statistic that the presstitute media cannot deflect.

An affront to China, whose government decides that knocking the US down a few pegs into third world status is worth a trillion dollars.

More derivate mistakes, such as JPMorgan Chase’s recent one, that send the US financial system again reeling and reminds us that nothing has changed.

The list is long. There is a limit to how many stupid mistakes and corrupt financial policies the rest of the world is willing to accept from the US. When that limit is reached, it is all over for “the world’s sole superpower” and for holders of dollar-denominated instruments.

Financial deregulation converted the financial system, which formerly served businesses and consumers, into a gambling casino where bets are not covered. These uncovered bets, together with the Fed’s zero interest rate policy, have exposed Americans’ living standard and wealth to large declines. Retired people living on their savings and investments, IRAs and 401(k)s can earn nothing on their money and are forced to consume their capital, thereby depriving heirs of inheritance. Accumulated wealth is consumed.

As a result of jobs offshoring, the US has become an import-dependent country, dependent on foreign made manufactured goods, clothing, and shoes. When the dollar exchange rate falls, domestic US prices will rise, and US real consumption will take a big hit. Americans will consume less, and their standard of living will fall dramatically.

The serious consequences of the enormous mistakes made in Washington, on Wall Street, and in corporate offices are being held at bay by an untenable policy of low interest rates and a corrupt financial press, while debt rapidly builds. The Fed has been through this experience once before. During WW II the Federal Reserve kept interest rates low in order to aid the Treasury’s war finance by minimizing the interest burden of the war debt. The Fed kept the interest rates low by buying the debt issues. The postwar inflation that resulted led to the Federal Reserve-Treasury Accord in 1951, in which agreement was reached that the Federal Reserve would cease monetizing the debt and permit interest rates to rise.

Fed chairman Bernanke has spoken of an “exit strategy” and said that when inflation threatens, he can prevent the inflation by taking the money back out of the banking system. However, he can do that only by selling Treasury bonds, which means interest rates would rise. A rise in interest rates would threaten the derivative structure, cause bond losses, and raise the cost of both private and public debt service. In other words, to prevent inflation from debt monetization would bring on more immediate problems than inflation. Rather than collapse the system, wouldn’t the Fed be more likely to inflate away the massive debts?

Eventually, inflation would erode the dollar’s purchasing power and use as the reserve currency, and the US government’s credit worthiness would waste away. However, the Fed, the politicians, and the financial gangsters would prefer a crisis later rather than sooner. Passing the sinking ship on to the next watch is preferable to going down with the ship oneself. As long as interest rate swaps can be used to boost Treasury bond prices, and as long as naked shorts of bullion can be used to keep silver and gold from rising in price, the false image of the US as a safe haven for investors can be perpetuated.

However, the $230,000,000,000,000 in derivative bets by US banks might bring its own surprises. JPMorgan Chase has had to admit that its recently announced derivative loss of $2 billion is more than that. How much more remains to be seen. According to the Comptroller of the Currency http://www.occ.treas.gov/topics/capital-markets/financial-markets/trading/derivatives/dq411.pdf the five largest banks hold 95.7% of all derivatives. The five banks holding $226 trillion in derivative bets are highly leveraged gamblers. For example, JPMorgan Chase has total assets of $1.8 trillion but holds $70 trillion in derivative bets, a ratio of $39 in derivative bets for every dollar of assets. Such a bank doesn’t have to lose very many bets before it is busted.

Assets, of course, are not risk-based capital. According to the Comptroller of the Currency report, as of December 31, 2011, JPMorgan Chase held $70.2 trillion in derivatives and only $136 billion in risk-based capital. In other words, the bank’s derivative bets are 516 times larger than the capital that covers the bets.

It is difficult to imagine a more reckless and unstable position for a bank to place itself in, but Goldman Sachs takes the cake. That bank’s $44 trillion in derivative bets is covered by only $19 billion in risk-based capital, resulting in bets 2,295 times larger than the capital that covers them.

Bets on interest rates comprise 81% of all derivatives. These are the derivatives that support high US Treasury bond prices despite massive increases in US debt and its monetization.

US banks’ derivative bets of $230 trillion, concentrated in five banks, are 15.3 times larger than the US GDP. A failed political system that allows unregulated banks to place uncovered bets 15 times larger than the US economy is a system that is headed for catastrophic failure. As the word spreads of the fantastic lack of judgment in the American political and financial systems, the catastrophe in waiting will become a reality.

Everyone wants a solution, so I will provide one. The US government should simply cancel the $230 trillion in derivative bets, declaring them null and void. As no real assets are involved, merely gambling on notional values, the only major effect of closing out or netting all the swaps (mostly over-the-counter contracts between counter-parties) would be to take $230 trillion of leveraged risk out of the financial system. The financial gangsters who want to continue enjoying betting gains while the public underwrites their losses would scream and yell about the sanctity of contracts. However, a government that can murder its own citizens or throw them into dungeons without due process can abolish all the contracts it wants in the name of national security. And most certainly, unlike the war on terror, purging the financial system of the gambling derivatives would vastly improve national security.

-

About The Author

Paul Craig Roberts has had careers in scholarship and academia, journalism, public service, and business. He is chairman of The Institute for Political Economy. Dr. Roberts was awarded the Treasury Department’s Meritorious Service Award for “his outstanding contributions to the formulation of United States economic policy.” In 1987 the French government recognized him as “the artisan of a renewal in economic science and policy after half a century of state interventionism” and inducted him into the Legion of Honor.

Further Reading:

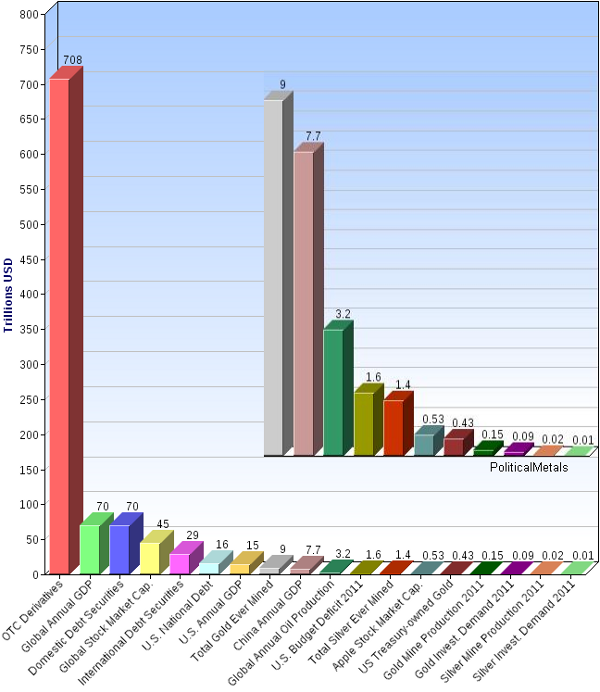

Explore this chart to see The BIG Picture of Derivatives

Mouse over each bar for details. Click on bars for data source.

-

Like this:

The Bottoms Debate

-

With last Friday’s historic largest single daily gain in gold on a COMEX close basis (up almost 4%), many analysts are calling this the bottom for PMs. It’s refreshing therefore to hear a contrarian (not bear) view on this. David Bond, editor of The Wallace Street Journal at silverminers.com, argues that

We may well see $18 silver and $1,200 gold and a 66.6-to-1 silver:gold ratio before the bloodiest is over.

As always, this site attempts to dig out stories from both sides of the coin for your analysis and due diligence before taking any actions. Enjoy this read…

-

This Ain’t The Bottom (But you can see it from here)

By David Bond | The Wallace Street Journal at silverminers

Wallace, Idaho – Bernard Baruch famously said: “Don’t try to buy at the bottom and sell at the top. It can’t be done except by liars.” Good advice. So many ersatz experts are calling this the bottom for silver and gold that it absolutely cannot be the actual bottom. It may be so close that we can see it, but we’re willing to ride this elevator down a few more floors before we hit that big red STOP button.

At the last bottom, in 2008, Hecla was a buck and Teck was only $5 ahead of it. If you read Jeff Clark’s article at Casey Research, read it again. If you haven’t, return to Go.

But smugness is the enemy. Until you feel panic in your loins – and you don’t feel it now, just yet – stand pat. Not that you’re going to be burned, buying just now, but the fire sale is ahead.

Our own crystal balls – Paul Sarnoff told us that prognosticators don’t have crystal balls, they just walk like then –tell us that we will see a massive sell-off in silver, down to the $18 level.

(Paul first brought to this writer’s attention what Clark’s article drives home: that decreasing open interest during a price trend signals a price trend reversal. If the price of gold keeps going up, but fewer and fewer people are jumping in, then jump out. The converse is true: If the price of silver and gold are going down, and fewer and fewer players enter the markets every day, then the price is headed northward.) Watch the open interest. If prices rise and more people jump in, that is the end of the bottom.

Three events will transpire this year that will send us and our little silver mining camp, temporarily, cratering. They haven’t happened, yet:

First, the pretender now occupying the White House will be defeated, which will incite riots by feral adolescents in every major U.S. city. (He might also prevail, in which case the same conditions will apply.)

Second, the young man who got the best of that fight with Trayvon Williams, will be acquitted on facts. This again will incite riots by feral adolescents in every major U.S. city.

Third, the Euro will collapse, which will incite government workers, feral whites and feral Muslims in the European capitals to tear down what’s left of the decent places there. What the Czars and the Nazis could not accomplish, Paris’ own recently-imported citizens will obtain the destruction of that magnificent city – in the harmless name of diversity, one supposes. Last chance to walk the fairarrondissements of the City of Light along the Seine without having to look over your shoulder. (What has been built on faith is easily destroyed on the altar of nihilism – just like fiat currency.)

These three events will drive the U$D up to record high levels as the Euro collapses. Probably happen late summer, early fall. The flight to the U$D will momentarily suck the wind out of the gold and silver sectors. The crash will be hard. We may well see $18 silver and $1,200 gold and a 66.6-to-1 silver:gold ratio before the bloodiest is over.

It will happen and it is going to suck. But it will be temporary.

Then, sometime late this year of early next year, a few bright people will discover that the U$Dollar has no meaning, no value, other than its reputation as a pledge of the “full faith and credit” of the United Snakes. But there is scant credit to obtain from this nation of debtors. We are not a country of farm-owners, of factory-owners, or even property owners or free men. We’re just renters without equity, and there is nothing to secure our debt.

I fear there will be violence at the portals of our great mines. Unlike the Mine Wars of a century ago, which pitted management against workers, this violence will pit Us against Them. Either Obama or Romney will need to seize ownership of our mines in order to secure the debt of these United Snakes. Our miners will be conscripted, and paid a barely meaningful wage – but enough to keep the cable TV turned on and the NFL package live.

If you are a shareholder in one of these mines, your future is secure. After all, even slaves need to be fed, and dividends will be paid as promised. Corporations and their shareholders are whores: if they’re paid, they’re fine.

Some things we have recently noted:

National Public Radio’s muppets are encouraging a U.S. military involvement in Syria. One supposes they would encourage Obama to enter into a third regional conflict, one more than He inherited, and blame it on Bush;

California will increase its cigarette tax by $10 per carton, on the heels of the Messiah’s tax increase of $10 federal tax per carton upon his inauguration. Having run out of Germans, Russians and Blacks to despise, the government is turning the hatred inward. What’s next? A call for school children to snitch off parents who do smoke?

The federal drumbeat to inform authorities of any suspicious activities on the part of one’s neighbors, no matter how harmless they really might be. My mother told me not to be a tattle-tale.

The continued irradiation and groping of people boarding airplanes. (Back when I was a child, you could just walk out onto the ramp, meet the pilots, extinguish a cigarette if they were refuelling. If you were polite they’d let you board and maybe even fly jump-seat for the next leg without a ticket. Nobody but your uncle took a picture. Try that now and you will be shot tazered or shot.

Imagine, if in 2021, a small group of screwed-up Americans hi-jacked an airplane and flew it into the Burj Al-Arab tower in Dubai, UAE. Imagine if then the United Arab Emirates spent the next decade invading Canada and torturing its citizens, leaving 8 million dead. Get the picture? Or am I being subtle?

Welcome to the Nazification of Amerika, land of the fleeced: We have ring-side seats to the planet’s greatest calamity, the death of its largest-ever Republic. Guilty until proven innocent – that’s our way. Gold and silver are no longer just a good investment. They will be the only way out of this snake-infested hole.

-

Related Articles:

-

JP Morgan Chase for Dummies

-

Breaking News:

JP Morgan sent out a notice at 4:30 p.m. that it would be holding a conference call at 5 p.m. which will include CEO James Dimon.

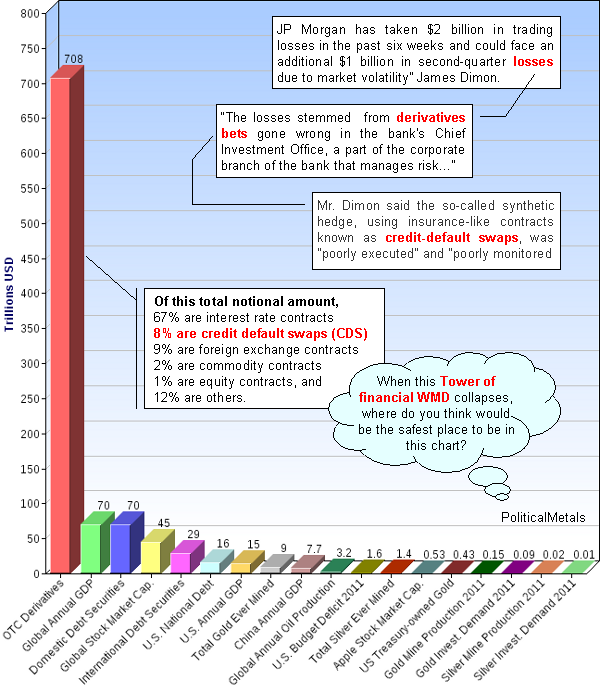

At the conference call, as reported by WSJ, Jamie announced that the the largest US bank has “taken $2 billion in trading losses in the past six weeks and could face an additional $1 billion in second-quarter losses due to market volatility”.

Here’s a Dummy trying to make sense of Wallstreet speak.

The losses stemmed from derivatives bets gone wrong in the bank’s Chief Investment Office, a part of the corporate branch of the bank that manages risk… Jamie announced.

So they lost $2 billion in 6 weeks and possibly another $1 billion over the next month. But what exactly are these derivative bets? Isn’t betting associated with gambling? Did the largest bank in the US take some of their bailout money, went gambling and now calling a press conference to announce their losses?

Mr. Dimon said the so-called synthetic hedge, using insurance-like contracts known as credit-default swaps, was “poorly executed” and “poorly monitored.” He said the bank has an extensive review underway of what went wrong, and that there were “many errors,” “sloppiness” and “bad judgment” on the bank’s part.

Ah… it’s not gambling, it’s actually a “synthetic hedge”. But I don’t even understand what’s a hedge, never mind the difference between synthetic and real! All I know up to this point is they lost big time through derivatives bets, which is a synthetic hedge, also known as credit-default-swaps. That’s quite a mouthful for a mere mortal.

What then are these credit-default swaps?

I know what’s a swap. You give me something, I give you another. But they’re swapping “credit-default” for something else? That sounds like a weird thing to be swapping. Fortunately I have good ole Wikipedia to the rescue:

A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a loan default or other credit event. The buyer of the CDS makes a series of payments (the CDS “fee” or “spread”) to the seller and, in exchange, receives a payoff if the loan defaults.

Oh, how could I have missed something so obvious! Didn’t Mr. Dimon say it’s an “insurance-like” contract? Now I get it, so I’ll just call it an insurance. JP Morgan sells insurance and receives an insurance premium. It works something like this: You lend me money, then buy an insurance policy from JPM saying that if I fail to repay your loan when it becomes due, they will pay you for the sum insured.

But insurance companies do payouts all the time. What’s the big deal? Then I recall that when there’s a major disaster - like the recent Christchurch earthquake, the payout was so big that AMI, the insurer, went under and had to be bailed out by the government to the tune of NZ$1 billion.

Now it begins to make sense why the conference call was made in such a haste. I recall that Greece defaulted in their debt triggering a payout around a figure of $3.5 billion, and I know JP Morgan is one of the major insurers and major holders of other types of “insurance contracts” collectively known as OTC Derivatives.

But how big exactly is JPM’s potential liability to these kinds of bets?

According to the Bank of International Settlements (BIS), which is the Central Bank of all national Central Banks, the total outstanding OTC Derivatives is $708 Trillion. Of this total notional amount,

- 67% are interest rate contracts,

- 8% are credit default swaps (CDS),

- 9% are foreign exchange contracts,

- 2% are commodity contracts,

- 1% are equity contracts, and

- 12% are others.

Since CDS makes up only 8% of the total OTC Derivatives, and a relatively minor default by Greece caused such a significant loss for JPM, imagine what will happen to JPM and the likes of JPM when the other PIGS countries ( Portugal, Italy, Greece and Spain) actually go into default. Also imagine what will happen when the interest rate contracts, comprising the bulk of OTC Derivatives actually triggered?

There must be good reasons why derivatives are referred to as Financial Weapons of Mass Destruction (WMD). Trying to time the explosion or implosion of this WMD is futile. Preparing for its consequences is vital. Take a look at the chart below, and see if you can spot where in this crazy world of finance is the safest place to be.

Mouse over each bar for details. Click to read data source

Updates:

- J.P. Morgan Chase fell 9.2%, its biggest percent drop since August

- Federal Reserve Officials investigating JPM’s losses

- Bernanke’s speech on May 10 “Conditions in the banking system-and the financial sector more broadly-have improved significantly in the past few years..”

- Derivatives: The $600 Trillion Time Bomb That’s Set to Explode

- Double or Nothing: How Wall Street is Destroying Itself (using Martingale system)

- Jim Willie explains JPM’s precarious position, new global financial system & why the USA will be a 3rd world state going forward

-

Featured Reviews

16Oct: Jeff Clark (Casey Research)

$2,300 gold by January 2014

05Sep: Bill Murphy (GATA)

$50 silver by year end

13Aug: James Turk (GoldMoney)

We won’t see $1580 gold & $27 silver again

12Aug: Bill Murphy's source

We could see a 100% increase in 90 days.

03Aug: HSBC Analysts

Gold to rally above $1,900 by end 2012

05June: David Bond (SilverMiners)

Gold & Silver may bottom at $1,200 & $18

02June: Don Coxe (Coxe Advisors)

Europe to issue Gold-backed Euro Bonds within the next 3 months

21May: Gene Arensberg (GotGoldReport)

Gold and Silver are very close to a bottom, if one has not already been put in last week

>> More forecasts & forecast accuracy

Daily GOLD US$/oz

Daily SILVER US$/oz

More Gold Charts: 1 Month to 660 Years

More Silver Charts: 1 Month to 660 Years

Gold/Silver Ratio: 1 Month to 660 Years

Gold & Silver Priced in BitCoins

Click to enlarge.

BitCoin donation welcomed.

1NQ4LqE8yL6rfAqikDU8wLhHSm5fntsWxk

Gold & Silver Interviews (KWN)

Gold & Silver Interviews (KWN)

- Hear Is Why Gold & Silver Are Set To Explode Going Forward October 28, 2012

- Here Is What Will Fuel The Move Higher In Hard Assets October 27, 2012

- Greyerz - Two Absolutely Incredible & Key Gold Charts October 26, 2012

- Celente - It’s Not Just Germany’s Gold That’s Missing October 26, 2012

- What To Expect With Gold Assaulting $1,700 & Silver At $32 October 26, 2012

- James Turk - The Entire German Gold Hoard Is Gone October 25, 2012

- KWN Update - Here Is A Huge Key To The Markets October 25, 2012

- Currency Wars Continue To Rage & This Is Positive For Gold October 25, 2012

Finance & Economics

- On The Fullness And Boldness Of QE's Manipulation Of American's Behavior October 28, 2012 Tyler Durden

- YouNG FRaNKeNSToRM... October 28, 2012 williambanzai7

- The Bread Aisle In Manhattan's Upper West Side Is Now Empty October 28, 2012 Tyler Durden

- Some Follow-Up Questions For The Bundesbank, And Its Gold October 28, 2012 Tyler Durden

- New York Mayor Orders Evacuation Of "Zone A" Residents October 28, 2012 Tyler Durden

- Guest Post: The Burden Of Government Debt October 28, 2012 Tyler Durden

- On Europe's Three Year Insolvency Anniversary - The Definitive Interactive Infographic October 28, 2012 Tyler Durden

- In Advance Of Frankenstorm Sandy, NYC Suspending All Transit Services At 7:00 PM Sunday Through Wednesday October 28, 2012 Tyler Durden

Silver Bomb

-

Paper silver prices have been subjected to severe downward pressure lately. If you identify yourself with the chap who wrote “I purchased my physical silver at $45.88/oz“ and viewed your silver purchases as an investment rather than a store of wealth, this interview may help calm your nerves.

-

This chart helps to put into perspective some of the key points discussed above.

-

The BIG Picture (Where is Gold & Silver in the global financial landscape)

Mouse over each bar for details. Click on bars for data source.

Share this:

Like this: