Here’s a Question, an Answer & a Rebuttal over the mystery of the “Yamashita’s Gold”. If you’ve not researched the issue, this discourse might be a good place to start.

Question: ”Yamashita’s Gold”, What do you think?

Image via Wikipedia

“I know your are one of the world’s most studied experts on this subject, way ahead of me in knowledge, so I may not be

saying anything you haven’t already considered. I read the book ‘Yamashita’s Gold’ a couple of years ago. The quantities of gold written about stay in my mind. The information is all shadowy, of course. The idea that much of the Western world’s gold made its way to the Far East as payment for spices, silks, etc., also stays in my mind.

“That this gold was gathered up and moved around either before or during World War II also makes sense. It had to end up somewhere.

“Documentation is too thin to to be mainstream precious metals investment material, but where there’s smoke, there’s probably fire. So perhaps there is enough gold in the world to serve as backing for all the digital money that has been conjured up in recent years.

“Of course the powers that be do not want such golden shackles. I’ve seen the ‘mining statistics’-based analysis of how much gold should have been mined and should exist in stockpiles. It’s scholarly work, but there may be factors at work that haven’t been consider — such as that gold is now more plentiful on the earth’s surface than it was in early times.

H.M., thanks for your note and the compliment but I’m not at all such an expert. To the contrary, the gold world is a big mystery to me, and GATA’s contribution is simply to raise the possibility that it is also actually a mystery to most supposed experts as well.

and particularly the one contending that a vast stash of gold plundered from Asia by Japanese forces during World War II was secretly confiscated by the United States. I have always discounted the story, in part because of the collapse of the London Gold Pool in 1968

For if so much hidden gold was available to it, the United States would not have been so desperate to close the gold pool as its reserves were depleted. Nor would the U.S. government through the years since World War II been so insistent on preventing a free gold market from developing. Indeed, if gold was actually as common as the Yamashita stories maintain, the Federal Reserve, Treasury Department, and Bank of England already would have arranged for Louis d’Ors to be inserted as prizes in Cracker Jack and children’s cereal boxes.

After all, the way to devalue gold is to flood the world with it.

But what has the world been flooded with? Not real gold but “paper gold,” imaginary gold. This reliance on the imaginary and the ever-more-embarrassing secrecy imposed by Western central banks on their gold reserves and activities in the gold market argue for scarcity of the real thing rather than surplus.

They used to say on a popular television show that “the truth is out there.” More likely the truth is in there - in government files, like the files GATA pried open a little with the success of our recent federal Freedom of Information Act lawsuit against the Fed in U.S. District Court for the District of Columbia:

There are grounds for bringing more such lawsuits, and with sufficient financial support, GATA will undertake them. If it really had Yamashita’s gold, the U.S. government wouldn’t be fighting us so hard.

Unfortunately, GATA gets it wrong here. This is one of the reasons I decided to go off on my own and create the Road to Roota website. Don’t get me wrong, the work that GATA does is essential in our battle against the Banksters but to shut your eyes to the “conspiracy side” is to miss a large part of what is going on. But I get it. Chris and Bill have worked tirelessly building “credibility” and I understand why they try to stay away from the more controversial topics. That is why I went off on my own.

From my research I am more than convinced that Yamashita’s gold is real and has been used by the US shadow government for years to fund their covert operations. All you have to do is read the exhaustive work of Sterling and Peggy Seagrave on the subject and you will understand. The book is called ”Gold Warriors: America’s Secret Recovery of Yamashita’s Gold” and it is a must read for anybody who wants to understand what goes on behind the scenes of the mysterious gold market.

The GATA posting talks about the documentation that supports their position (which is excellent) but for as much official documentation GATA has the Seagraves have discovered 10 times more to back up the Yamashita’s Gold story. This documentation ranges from US Government documents to Federal Reserve documents to Grand Jury testimony to US Congressional testimony and on and on. There are also CD’s of dozens of scanned original documents supporting the Seagraves claims in the book.

The end result from my analysis was that Yamishita’s Gold is 100% real.

Kudo’s to Chris for pointing out that GATA is not the expert on the mysteries and conspiracies of the gold market but there are experts out there for anyone who wants to spend the time to do the research. Here’s a couple places to start:

“Gold Warriors: America’s Secret Recovery of Yamashita’s Gold” by Sterling & Peggy Seagrave

Once you fully research the Yamishita’s gold story you will come away with the same conclusion I did…That it is a true story and must be factored into the overall gold analysis.

But that it does not diminish the work of GATA or the fact that Gold (and Silver) are the best forms of money. They are far superior to the Quadrillions of paper and electronic monetary instruments being created that show no signs of “Production Slow-downs”. As a matter of fact, the GATA argument that if the Yamashita stories were true then the US would not go to the trouble of suppressing the price grossly underestimates the importance of Gold price suppression.

A better argument would be that the US deems Gold to be so important that they suppress the price IN SPITE of all the Yamashita’s gold available!

At the end of the day…Gold will continue to THRIVE even if they start putting gold coins in Cracker Jack boxes

Just because you hoard money or Gold Bullion, doesn’t mean you’re sick or wrong…

-

It disables the sufferer and those around them, presenting a health hazard as stuff piles up and the home turns into a trash can.

“Hoarding and anxiety go hand-in-hand,” says one struggling survivor. “For many people, including hoarders and non-hoarders, fear keeps us from letting go of objects we don’t need.” Beating fear is a tough ask, however, and “clean-up usually provokes intense anxiety,” says another report.

Anyone helping the hoarder – even a professional cleanup crew – should be gentle, always caring and encourage the person to deep breathe and relax.

Now, given these sensitivities – and seeing how the causes of hoarding include dementia, depression, and obsessive compulsive personality – you might expect people to be a bit nicer when trying to get hoarders to stop. But no.

“Companies’ growing cash piles are irking shareholders and stunting growth,” barked the Financial Times in late January. “Politicians and policymakers are going to have to ask the question,” declared David Bowers of Absolute Strategy Research in London – “How much longer are we going to allow companies to run themselves for cash?

Two weeks later, Martin Wolf was at it in the same pages. “Britain needs to whittle down corporate cash piles,” he announced, also quoting approvingly a London finance type, this time Andrew Smithers of Smithers & Co. “If the fiscal deficit is to disappear…there needs to be a mixture of lower profits, higher investment, and significantly smaller current account deficits.

“Increases in government investment and private housebuilding would also help,” said Wolf, parroting UK and US economic policy since the Second World War. But the slaughter of corporate hoarders is new. Because the phenomenon is new, and “highly indebted UK households should not run large deficits again.” Or to quote The Times this Monday, “Consumers cannot lead recovery. Britain needs business to stop ‘stashing the cash’.”

Now “Companies must stop hoarding cash and start investing instead,” says – choke! – Will Hutton in The Guardian, quoting this week’s same press release from the same think-tank, Ernst & Young’s ITEM Club. “David Cameron and George Osborne have still not developed a full-throated industrial policy that would encourage companies to spend money on investment and innovation.”

“Business investment has picked up nicely in the US,” says ITEM’s chief economic advisor, Peter Spencer, apparently missing the $1.24 trillion in US corporate cash piles stacked up by end-2011 – well over half of it outside Uncle Sam’s borders according to Moody’s, as emerging-market growth plus onerous US tax treatment drives businesses to avoid remitting profits back home.

“But UK companies remain extremely risk-averse, which is sapping strength from the economy. Until these companies…start increasing levels of investment and dividends, the economy will remain on the critical list.”

Perhaps if everyone shouts loudly enough, the hoarders will snap out of it? But then, they are trying already, albeit at gun point. US equities have been paying a higher yield than Treasury bonds for the first time in six decades. “Total dividends paid by UK companies hit a record £67.8 billion in 2011 [$110bn] a rise of almost 20% on 2010,” says Hargreaves Lansdowne, the retail-investor brokerage. “Encouragingly, dividend growth was seen across all industry sectors.”

And it’s not like corporate US and Britain didn’t do their bit in fighting the war of debt vs. recession starting in the mid-1990s either. Over the 12 years ending spring 2009, for instance, private-sector UK companies outside the financial sector spent 124 months growing their bank debt net-net. Yes, UK households fought harder (141 out of 144 months), but they began to rein in their borrowing sooner and actually saved money right when the canon fodder were called on for a last “big push” in late 2007.

But so what? “British companies are running a cash surplus of some 6% of GDP, the largest in the world,” says Hutton, gasping at people making a profit and daring to keep it.

[They] are refusing to spend that cash on investment or innovation, preferring to hoard it, preserve profit margins or buy back their own shares.

Oh the monsters! Refusing to spend…stashing the cash…hoarding what should be shared for the good of us all! It must not be allowed. And luckily the financial press began softening up public opinion at the start of the year, when the FT first ran that story about what it called “the $1,700bn problem. Companies in the US are flush with cash and are paying out a smaller proportion of their earnings as dividends than ever before. Much the same can be said for western Europe. Governments and households on both sides of the Atlantic are meanwhile strapped for cash. This cannot persist much longer.”

“Businesses run ‘for cash’, rather than spending in an attempt to boost revenues, do not promote growth,” said the Pink ‘Un. The government should do something to stop it!

The battle front today is against the hoarding of currency. No one will deny that if the vast sums of money hoarded in the country today could be brought into active circulation there would be a great lift to the whole of our economic progress.

So said Herbert Hoover, then US president, in early 1932, and quoted in Murray Rothbard’s America’s Great Depression (Princeton, 1963). “We are making war on depression. War against a lack of confidence. Our people must have something tangible to do in the fight. There is no use to go out and say ‘Have confidence, courage and faith.’ They must have something positive to bite on.

They can bite on the question of hoarding.

Hoover’s war on the hoarders presaged Roosevelt’s war on fear, with a task force of opinion and business leaders enlisted to make hoarding cash – then outside the banks, under the mattress, for fear of default – socially unacceptable. “It [hoarding] began in April last year in consequential amounts,” Hoover told a private White House gathering of newspaper editors and other luminaries that February. “The disturbances in Austria, which finally culminated in the German panic, showed paralleled increases of hoarding in the United States, which rose at one time to about seventy or one hundred million a week…[Then came] the disturbance in Great Britain which finally resulted in the British abandonment of the gold standard.

“Instantly, within 24 hours after the Bank of England ceased paying gold, hoarding jumped in the United States to $250,000 a week.”

This was unsurprising. Because then, as now, people kept hold of their money – hoarded it, if you must – for fear of losing it to one of the catastrophes striking so many others around them. And then, as now, US citizens also had the option of what would soon prove a rare privilege, of hoarding Gold Bullion too. In the early 1930s, however, people kept their cash at home, out of deposit accounts, for fear of banking collapse. Gold meantime really was money.

Keeping gold at home – out of circulation and safely away from bank credit – was therefore bad for the nation. It could not be allowed to persist, and Hoover’s successor, F.D.R., wasted no time in making Gold Bullion illegal for everyone but the State, nationalizing private gold holdings at $26 per ounce, raising the official price to $35 per ounce, and thereby enforcing on the United States the very Dollar devaluation which gold hoarders had feared.

Bite on that. Or to put it another way, just because you hoard gold or fear bank credit today, doesn’t mean you are in need of treatment or tough love.

Buying Gold today? Make it simple, secure and low cost…starting with a free gram of Zurich bullion right now…at BullionVault…

Gold priced in US$ has been declining from its high in August 2011. Wall street has it that it’s because the euro zone debt crisis is now under control, the US economy is recovering, inflation is low and the US unemployment situation is improving. Oh, not to forget there has been no more money printing and the Dow has gained some 20% since gold’s peak. In short, improving outlook has caused investors to move out of gold’s safe haven into riskier assets.

Less demand leads to lower gold prices as reflected in the chart below. Some analysts say the 11-year bull market in gold is over, gold is in a bubble that has or is about to bust.

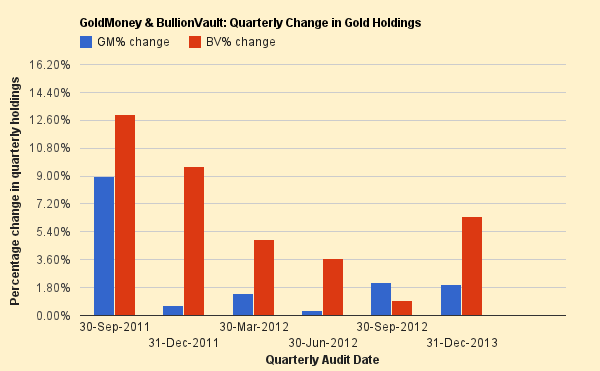

If that be the case, clients of GoldMoney & BullionVault (two of the more established and popular physical gold dealer and custodians) have got it all wrong and hence are “of all men most to be pitied”. Look at how their collective gold holdings have been increasing relentlessly, even during periods of sharp price declines.

This short term chart covering the period since gold’s intermediate top in August 2011 shows steady increase of total holdings from quarter to quarter. The growth at BullionVault is particularly impressive.

-

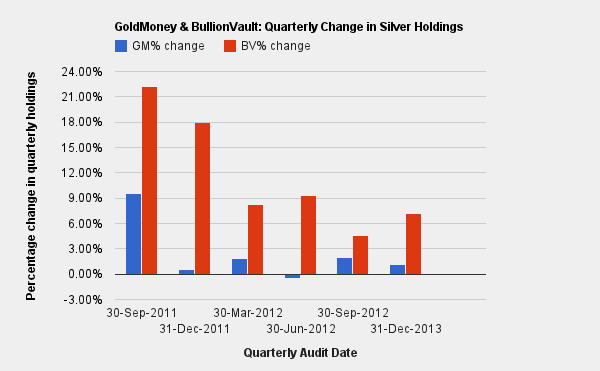

The same goes for silver.

What then can be said of the apparent dichotomy between the declining trend in gold & silver prices and the increasing demand seen in the metal purchases? Just two words:

Paper & Physical

Prices reflected in the charts come about mainly by “traders” trading paper gold & silver. Traders is put between quotes because they are not the normal traders you’d expect to find in a free market. Most of the trades that determine the price trends are placed by very few large bullion banks and High Frequency Trading (HFT) machines. Yes, the prices are greatly influenced by trades initiated by machines preprogrammed with sophisticated algorithms to set the price which ever way the owners wanted them to go. In case you’re wondering, who may be the people on the other side of these trades? It’s people like this, who sets up trades hoping to beat the supercomputers on the other side only to get sucked in and forced to dump when their stops are hit.

On the other hand, real humans are behind the accumulation of physical metals at BullionVault, GoldMoney and many other private vaults. These are the same humans that do not believe the spin of the MSM, but hold on to the view that the financial crisis is not yet behind us. They believe that the worse is yet to come. I’m one of them. We understand that holding our savings and retirement funds in paper assets and paper money is most likely to result in a massive loss of purchasing power through hyperinflation when the real crisis hits.

We’re not 100% sure it will happen, neither can we be 100% sure it won’t happen.

What about you? Paper or physical?

-

Data source

GoldMoney publishes quarterly audit reports, and they are archived here.

by Steve Elwart, IDB Folio Specialist

Republished with permission from Koinonia House

-

This is Part 1 of a three-part series on money: where it comes from, how governments use it to control our lives, and how modern money policy makes the prophecies in the Book of Revelation seem very close to fulfillment.

Everyone reading this article is being robbed. We all use paper money and every day, governments are lowering its value. That value is being stolen from us. To understand how this is happening, we need to get to the basics of money. What is it?

Commodity Money

We learn in Genesis that Abram (renamed later by God to Abraham) was a rich man. How do we know? We are told that “he had sheep, and oxen, and he asses, and menservants, and maidservants, and she asses, and camels.”1 In Biblical times, these things were all media of exchange. No king decided this; he didn’t call in his magi to decide what the medium of ex-change would be. Ordinary people, or “the market” made the decision. Let’s say a king did decree that rocks could be used as money. Would anyone use them? Probably not, because they would not know the value of those rocks. Unless you are building a lot of things (or stoning a lot of adulterers), rocks fail to meet a standard for money: they have no intrinsic value.

If a civilization was to advance though, it had to come up with a convenient way to save and exchange value to buy things. Leather was used in ancient Rome. (Contrary to popular belief, Roman soldiers were not paid in salt. The term salary [from the Latin salārium] was money given to Roman soldiers to buy salt.2) Animal pelts, whiskey, and tobacco leaves were used in the former British Colonies, wampum (strings of beads) was used by the American Indians, dried fish were used in the Canadian maritime colonies, maize or corn was used in Mexico, and salt, iron and farming tools were used in Africa. These things are called “commodity money.” As civilizations became more complex, most forms of commodity money be-came very cumbersome. (Who would want to give or get 300 sheep to buy a car?) Another medium of exchange had to be found.

Over the centuries, the answer came to be the precious metals, gold and silver. These two metals became the basis for money in most of the world. Gold and silver were used as money for very specific reasons and they were chosen by “the market.” People decided that these two metals had all the qualities that made for a good medium of exchange:

They were easily portable. They had high value to weight ratios. (So if you want to buy a car, you only have to bring 16 ounces of gold rather than 300 sheep.)

They are fungible. Every ounce is like every other ounce no matter where they were mined. People didn’t have to worry about the quality of the pure metal.

They are highly divisible. They can be divided into very small parts or coins. The term “pieces of eight” came from the practice of taking a Spanish dollar, a real de a ocho and breaking it up into eight pieces or reales to make change. Diamonds fail the test of being divisible because if you break up a gem-quality diamond, it loses its value. (For that matter, sheep aren’t easily divisible either unless you are very hungry.)

They are highly durable; the thirty pieces of silver paid to Judas are still in existence today.

They are naturally scarce. They can’t be multiplied.

Fiat Money

There is another type of money besides commodity money, called fiat money. (Fiat from the Latin fiat, meaning “let it be done.”) This is an item, usually paper or low value metal coins, that is decreed to have value by a government.

A government puts fiat money into circulation first by connecting it to a gold or silver standard, but then cuts the link and says that gold and paper are no longer convertible, making the piece of paper “legal tender for all debts public and private.” It is obvious that debtors would be very happy if the pa-per money lost its value because they could pay their debts with inflated currency. In a letter to Edward Carrington in 1788, Thomas Jefferson wrote, “Paper is poverty … it is only the ghost of money, and not money itself.” Jefferson died bankrupt because of the early United States money (monetary) pol-icy based on paper.

It is not that fiat currency is a new invention. Fiat currency actually made its appearance over 1,000 years ago. China was the first country to issue true paper money around the 10th century A.D. Although the notes were valued at a certain ex-change rate for gold, silver, or silk, conversion was never allowed in practice. The bills were supposed to be redeemed after three years in circulation, but as more bills were printed with the older notes being refused redemption, inflation became evident. Government measures to prop up the currency were unsuccessful and it fell out of favor.3

In Europe, fiat money came into being around the 12th century. Villagers would store their gold and other valuables in their lord’s castle for safekeeping. But during this time of the Crusades and other European Wars, noblemen were always strapped for cash. When times were particularly bad, the noblemen would confiscate the villagers’ gold and silver and issue notes for it, to be redeemed later. Needless to say, the notes weren’t always honored or if they were redeemed, the holder of the note received less of their gold back than what they were promised. This is an early case of price inflation.

Today, fiat money will always bring on inflation for two reasons: 1) Politicians like to induce inflation because it gives the people the illusion of prosperity and 2) its declared value is much higher than the cost of producing it. Whether it is a $1 or $100 bill in fiat money, it costs only 4 cents to produce. In today’s electronic age, the production cost for new money is zero since money creation is just a keystroke and an entry in cyber-space. On the other hand, in history, if you had a $20 gold piece, the cost of that gold piece, less the cost to produce it, was about $20.

The Gold Standard

If the relative value of gold is tracked over the years, one can see how fiat money loses its value over time.

By the 1400s, most countries that had complex trading systems were using gold and silver for transactions. Prices held relatively steady through the early 20th century, except for lo-cal shortages and wars. In the United States the price of gold and the things it bought held its value with exceptions for war-time when the government printed paper money to cover its war debts. After the emergencies and the country went back on the gold standard, prices went back to about where they were. During the First World War, most countries involved in the war suspended the gold standard so they could print enough money to pay for their involvement in the war. After the war, these countries went back to a modified form of the gold standard, but abandoned it during the “Great Depression.”

In 1941, most countries adopted the Bretton Woods system, which set the exchange value for all currencies in terms of gold. Countries that signed the Bretton Woods agreement were obligated to convert their currencies held by foreign countries into gold valued at $35 per ounce. However, many countries just pegged their currency to the U.S. dollar, thus making it the de facto world currency.

In the 1960s the United States had done something unprecedented in its history. The country fought two wars at once. The United States fought a war halfway around the world in Vietnam and a second war at home, the “War on Poverty.” To do this, the United States started to borrow massively and brought on double digit inflation. To curb the inflation, the United States government started to deflate the dollar. 1963 marked the entrance of the new Federal Reserve notes and the disappearance of the $1 silver certificate. This marked the point that no longer did the U.S. Government have to pay in “lawful money.” Finally, in late 1973, the U.S. government decoupled the value of the dollar from gold altogether and the price shot up to $120 per ounce in the free market.4 Since the United States went off the Gold Standard, a dollar is worth only one-sixth of what it was in 1973. (At this writing, gold is priced at $1,220 per ounce.5)

Inflation Always Follows Fiat Money

The history of price inflation in the United States is repeated in every country that uses paper money. Keep in mind, rising prices are not always bad. If a good becomes scarce, its price will go up and may provide the motivation to introduce a new, better product for the market. The reason petroleum became so popular so quickly was because of the rising cost of whale oil. If governments propped up the price of whale oil to keep whalers and whale oil processors employed, it would have taken decades for the world to embrace petroleum as a substitute. And someday, petroleum will go the way of whale oil as long as market forces dictate the transition.

When a government inflates its currency, it increases prices by reducing the purchasing power of the money. The short-term effects though, can seem to be positive. Like a drug addict, inflated money gives the illusion of prosperity, making people feel good. But like the addict, withdrawal follows the high.

At first, the surge of more money makes people feel good be-cause they can pay off their debts with cheaper money and they seem to have more disposable income. As prices catch up, people then find it more expensive to live. In addition, their tax burden goes up, since many government taxes are progressive in nature, meaning the percentage tax increases as in-come or asset values (houses, cars, etc.) increase. Eventually the market will try to correct itself and a depression will follow.

At this point, people start to feel the pinch of their money buying less. They demand that their government do some-thing. Since studies have shown that voters only have a memory of one year when it comes to politics, politicians will make sure that the economy is good in an election year.6 They will artificially stimulate the economy to give voters the illusion that times are good again and reelect the incumbents. This lasts only so long and inflation, with its problems kick in again. This cycle of increasing the currency supply and price inflation ultimately ends with the collapse of the currency, sometimes preceded by hyperinflation. (Hyperinflation and its cultural effects will be covered in Part 3 of this series.) Surprisingly, the country has not learned its lesson and the devalued fiat currency is replaced with yet another fiat currency. Greece is a perfect example of this cycle.

The Greek drachma was minted in gold and silver in ancient Greece and made its reappearance as a fiat currency in 1841. Since then, the value of the drachma decreased. During the German-Italian occupation of the country from 1941-1944, hyperinflation ravaged the country, ending with the issuance of 100,000,000,000 (100 billion)-drachma notes in 1944. After Greece was liberated from Germany, old drachmae were ex-changed for new ones at the rate of 50,000,000,000 to 1. Only paper money was issued, again a fiat currency. Greece then went on a program of deficit spending for social programs and inflation started once again.

In 1953, in an effort to halt inflation, Greece joined the Bretton Woods system and the drachma was revalued at a rate of 1000 old drachma to one new drachma. In 1973 the Bretton Woods System was abolished; over the next 25 years the official exchange rate gradually declined, from 30 drachmas to one U.S. dollar to a ratio of 400:1. On January 1, 2002, the Greek drachma was officially replaced as the circulating currency by the Euro (again a fiat currency).7

Today, Greece is once again is in trouble. After years of continued deficit spending and the government’s easy monetary policy, Greece’s financial situation was badly exposed when the global economic downturn struck. Very quickly, the government’s “creative accounting” practices were exposed. The national debt, put at €300 billion ($413.6 billion), is bigger than the country’s entire economy, with some estimates placing it at 120 percent of gross domestic product in 2010. The country’s deficit—how much more it spends than it takes in—is 12.7 percent.

This time though, Greece just can’t inflate their way out of the problem. Now that they are on the Euro (in the “Euro-zone”), they have little control over their monetary policy. All their loans are in Euros and they must pay back the loans in Euros. One way to balance the national books is to implement harsh and unpopular spending cuts. Another way is to default on their debt. This would seriously damage the Euro as other countries look at default as a way out of their financial problems. (In fact, financial experts are predicting the demise of the Euro in as early as five years.8) A third way out is to separate itself from the Euro, go back on the drachma (fiat currency again) and then set an exchange rate of the drachma to the Euro at an artificially high number. The cycle of fiat money would then begin again.

As long as a country is on a fiat currency, inflation is sure to follow. Using a fiat currency could well reduce a civilization to work an entire day for a “bushel of wheat.”

In Part 2 of this series we will look at central banking and how the banks can change a society.

Notes:

Genesis 12:16b (KJV).

“The American Heritage Dictionary of the English Language, 4th edition”. Answers.com. Retrieved 2010-06-05.

Ramsden, Dave (2004). “A Very Short History of Chinese Paper Money.” James J. Puplava Financial Sense.

History of the Gold Standard: http://useconomy.about.com/od/monetarypolicy/p/gold_history.htm

5 days ago saw the 150th year anniversary of an event so historic that a very select few even noticed: the birth of US fiat. Bloomberg was one of the few who commemorated the birth of modern US currency: “On April 2, 1862, the first greenback left the U.S. Treasury, marking the start of a new era in the American monetary system…. The greenbacks were originally intended to be a temporary emergency-financing measure. Almost bankrupt, the Treasury needed money to pay suppliers and troops. The plan was to print a limited supply of United States notes to meet the crisis and then have people convert the currency into Treasury bonds. But United States notes grew in popularity and continued to circulate.” The rest, as they say is history.

In the intervening 150 years, the greenback saw major transformations: from being issued by the Treasury and backed by gold, it is now printed, mostly in electronic form, by an entity that in its own words, is “set up similarly to private corporations, but operated in the public interest.” Of course, when said public interest is not the primary driver of operation, the entity, also known as the Federal Reserve is accountable to precisely nobody. Oh, and the fiat money, which is now just a balance sheet liability of a private corporation, and thus just a plug to the Fed’s deficit monetization efforts, is no longer backed by anything besides the “full faith and credit” of a country that is forced to fund more than half of its spending through debt issuance than tax revenues.

At the start of the Civil War, the U.S. didn’t have a national paper currency. Instead, the money supply consisted of U.S. coins and a collection of paper notes issued by private banks. Technically, the federal government began issuing its own paper currency in 1861. That year, the Lincoln administration issued $60 million in demand notes, a variant of a Treasury note that was redeemable “on demand” for gold coins at the Treasury or any sub-Treasury.

These notes were overshadowed in 1862 by the issue of $150 million in a new fiat currency officially known as United States notes and popularly known as greenbacks or legal tenders. By the end of the war, close to $450 million worth of greenbacks were in circulation.

The name greenbacks referred to the reverse of the notes, which were printed in green. The name legal-tender notes referred to the text that originally appeared on the back, which began, “This note is legal tender for all debts, public and private.” This provision made the currency a valid form of payment on par with gold and silver, which was a very controversial action at the time. It made the United States note a fiat currency — meaning its value was established by law alone and wasn’t based on some other unit of value, such as gold, silver or land.

Many Americans during and after the Civil War believed the creation of a fiat currency was unconstitutional. The Constitution explicitly stated that only gold and silver could be considered legal tender. In 1871, in the case of Knox v. Lee, the Supreme Court settled the matter by declaring that making United States notes legal tender was indeed constitutional.

By this time, the greenback was at the center of a countrywide debate on monetary policy. When the post-Civil War economic boom ended in the panic and depression of 1873, many people, especially farmers, blamed the Treasury’s policy of contracting the currency — that is, removing United States notes from circulation in an attempt to go back to the gold standard, which would require that a $1 note could be redeemed for $1 in gold.

As a consequence, there was a call for the expansion of United States note circulation or an inflation of the currency. This belief became joined with a political ideology that opposed big business and banking interests, resulting in the birth of the Greenback Party in 1874.

Opposing the Greenbackers were more conservative interests, sometimes known as “gold bugs,” who found support in the Republican Party and in elements of the Democratic Party. Gold interests proved the stronger contestant in the debate and in 1878, the total circulation of United States notes was fixed at a little over $346 million and the notes eventually became redeemable in gold (at least until 1933, when this provision was removed).

During the 20th century, United States notes became ever less important in the nation’s money supply, though Congress supported their continued circulation. They were increasingly replaced by currency issued by the Federal Reserve System, which came to look almost identical to the United States note. The Federal Reserve note thus became the new greenback.

In 1966, Congress allowed the Treasury to start removing United States notes from circulation. The last delivery of the notes by the Bureau of Engraving and Printing to the Treasury was made in 1971. In 1994, the Riegle Community Development and Regulatory Improvement Act eliminated the issuance of the notes altogether.

So instead of real money, America has an impostor “which came to look almost identical to the United States note” with the full complicity of everyone in charge, just so that when needed, any and all untenable debt burdens can be inflated away. And while the latter is a topic of a whole different discussion, we present another chart which, unlike the 150th anniversary of fiat, should be something discussed far more broadly… Because in a fiat world superpower status is always relative.

-

[Active updates: Developing stories] The South Carolina Treasurer’s Office, acting upon a directive from the state legislature, has recently published a report on the advisability of investing in gold and silver. Basically, the state legislature wanted to know if it’s wise to invest public funds under it’s custody in gold & silver.

Here’s what the Treasurer’s Office has to say about itself:

Our mission is to serve the citizens of South Carolina by providing the most efficient banking, investment and financial management service for South Carolina State Government. Our commitment is to safeguard our State’s financial resources and to maximize return on our State’s investments.

This is a tall order, hence we can assume that the report must be well researched and credible. It concluded that it is not advisable to invest public funds in gold & silver because:-

There’s escalating market speculation

Current value (I think they mean price) is too high

Market possibly in a bubble

South Carolina Code of Laws states that the Treasurer has “ full power to invest” in debt instruments of the US government and corporations, but makes no mention of investments in derivatives of gold & silver. Hence investing in gold & silver derivatives may “create a legal conflict”

While the timestamp of the document was 27 Feb 2012, it can be assumed that the report was prepared soon after the end of September 23, 2011 due to this inclusion. From the perspective of a short term investment, that was a pretty good call, considering the fact that gold and silver have been taken down to $1624 and $31.40 respectively as I write.

However, this piece is not about how good the Treasurer’s Office was at making an investment call based on price. Neither is it about whether gold & silver is in a bubble. These conclusions (2) & (3) are opinions of the Treasurer’s Office, which are subjective. Of greater interest are the facts revealed in the body of the report.

Regular readers of this blog would have noticed that there are several key issues that are repeatedly discussed or highlighted here (through news feeds or third party contributions). They include:-

Gold & silver prices are being suppressed

Central Banks & major bullion banks are suppressing their prices

Naked short selling is one of the price suppression mechanism

Bullion Banks and exchanges practice fractional reserve bullion banking

Stay out of gold or silver bank accounts, ETFs, Certificates, and all forms of derivatives

The safest way to own gold & silver is to hold physical gold & silver

Items (1) to (4) are often disputed by the mainstream media and investors, sometimes referring to them as conspiracy theories. Hence, it is most interesting to see what this government published report has to say about these 6 issues.

Price Suppression is Real

In one short paragraph, this report confirms in no uncertain terms the truth behind the so called “conspiracy theories”. Not only does it confirm the existence of price suppression, it discloses the WHOs and the HOWs!

Risks of holding gold through ETFs, Certificates, Bank Accounts & other Derivatives

It has been repeatedly emphasized here that the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system. Anything else is a derivative - a paper or electronic representation of the real thing.

This report explains the nature of these derivatives and lists the risks associated with each, together with reasons why the Treasury’s Office advised against investing in them.

The full report in pdf is available for download at the South Carolina Treasurer’s website. Text from relevant sections is reproduced below with comments related to the 6 items above highlighted. Most of the remarks are self explanatory. There are, however, two groups of comments that warrant some discussion.

1. Allocated & Unallocated Accounts

Ways to Invest: Certificates

Unallocated gold certiñcates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. Allocated gold certificates should be correlated with speciñc numbered bars, however it is difficult to prove whether a bank is improperly allocating a single bar to more than one investor.

Ways to Invest: Accounts

One of the most important differences between accounts is whether the gold is held on an allocated or unallocated basis. Another major difference is the strength of the account holder’s claim on the gold, in the event that the account administrator faces gold-denominated liabilities, asset forfeiture, or bankruptcy.

The above describes two products offered by banks to clients who want to invest in gold (or silver) without having to deal with the physical metals. For example, when a bank accepts $2,000 from a customer and issues a gold certificate or credits the customer’s gold account under the unallocated system, the bank is not obliged to buy and store 1.2 oz (at current price) of gold on behalf of the customer. It holds only a tiny portion of that amount in gold. Hence when many of its the customers decide to redeem their certificates at the same time, the bank will not have sufficient gold to deliver. This is what’s referred to as a “run on the bank’s gold on deposit”. The same applies when depositing cash in your bank. The practice of keeping only a tiny fraction of what’s rightfully belonging to the customers (gold or cash) is referred to as fractional reserve banking.

When selling allocated gold products, the bank is legally required to hold 100% of the customers deposit in physical metal. For example, if a customer deposits sufficient cash to own a 400 oz gold bar and is assigned a bar bearing serial No: AGR Matthey 156571, how can one be sure that the same bar or a portion thereof is not assigned to another customer at the same time? That’s the issue raised by the report - and the risk is real.

This brings us back to “the only secure means of owning gold & silver is by holding physical coins and bars in your own possession or stored in a private vault outside the banking system”. If you have to use a third party to store your metals, use specialized private vaults instead, because banks operate on a fractional reserve banking system.

There are many companies outside the banking system that offer secure vaulting services. Generally, they have very high transparency, including publishing audited client holdings on the web for public scrutiny (without any login required). Of course clients’ ID are anonymous, and known only to the operator and the client.

2. Reason for not investing in physical gold & silver

The report listed 5 ways to invest in gold & silver - ETPs, Certificates, Accounts, Derivatives and physical coins & bars. Notice how it highlights & explains all the risks associated with ETPs, Certificates, Accounts and Derivatives and the reasons why it is not advisable for the Treasury to invest in these.

Notice also that there are NO risk associated with physical metals. The only reason given for not investing in coins and bars is “South Carolina does not have the capacity to store or funding to secure gold and silver bullion”.

Proviso 89.145 GP:

Gold & Silver Investments

Office of State Treasurer

-

GOLD AND SILVER AS AN INVESTMENT:

Historically, investors have purchased gold as a hedge against an economic, a political, or a currency crisis. A decline in investment markets, a growing national debt, a weak currency, increasing inflation, military conflicts and social unrest are the most common reasons for investment in gold. Currently, gold and silver are at historic highs leading many expert investors to conclude that a bubble has been created in the precious metals market. Since the US recession began, the value of gold and silver has increased as investment markets perform poorly, troublesome economic news is announced, and when uncertainty in international markets intensifies.

Similar to other commodities, the value of gold and silver is determined by supply and demand, as well as speculation. The Federal Reserve, The London Bullion Market Association, JP Morgan Chase, and HSBC Holdings have practiced fractional-reserve banking and engaged in naked short selling causing artiñcial price suppression.

There are several ways to invest in gold and silver: bars, coins, ETP’s, certificates, accounts, and derivatives. If a state were to choose to invest in gold (and silver), it would likely choose to invest by:

1. ETP’s-Exchange Traded Products. This allows the stakeholder to invest in bullion without having to store bars and coins. The ñrst gold ETF (Exchange Traded Fund) was created in 2003 and has been viewed largely as a success, but has also been compared to investing in mortgagebacked securities. The annual expenses of the fund (storage, insurance, and management fees) are charged by selling a small amount of gold represented by each certificate, so the amount of gold in each certificate will gradually decline over time. ETF’s are investment companies that are legally classified as open-end companies or Unit Investment Trusts (UIT), but differ from traditional open-end companies and U]T’s. The main differences are that ETF’s do not sell directly to investors and they issue their shares in what are called Creation Units. Also, the Creation Units may not be purchased with cash but a basket of securities that mirrors the ETF‘s portfolio. The Usually, the Creation Units are split up and re-sold on a secondary market.

2. Certificates- allow investors to avoid the risks and costs associated with the transfer and storage of bullion by taking on a set of risks and costs associated with the certificate itself. Banks may issue gold certificates for gold which is allocated (non-fungible) or unallocated (fungible). Unallocated gold certiñcates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. Allocated gold certificates should be correlated with speciñc numbered bars, however it is difficult to prove whether a bank is improperly allocating a single bar to more than one investor. The US ñrst authorized the use of gold certificates in 1863. By the early l930’s the US placed restrictions on private gold ownership and therefore, the gold certificates stopped circulating as money, but certificates are still issued by gold pool programs for investment purposes.

3. Accounts- Many banks offer gold accounts where gold can be instantly bought or sold just like any foreign currency on a fractional reserve (non-allocated, fungible) basis. Pool accounts, facilitate highly liquid, but unallocated claims on gold owned by the company. Digital gold currency systems operate like pool accounts and additionally allow the direct transfer of fungible gold between members of the service. Different accounts impose varying types of intermediation between the client and their gold. One of the most important differences between accounts is whether the gold is held on an allocated or unallocated basis. Another major difference is the strength of the account holder’s claim on the gold, in the event that the account administrator faces gold-denominated liabilities, asset forfeiture, or bankruptcy.

4. Derivatives- The product symbol for gold futures is GC, and it is traded in a standard contract

size of 100 troy ounces. In the US, gold futures are primarily traded on the New York Commodities Exchange (COMEX). As of 2009 holders of COMEX gold futures have experienced problems taking delivery of their metal. Along with chronic delivery delays, some investors have received delivery of bars not matching their contract in serial number and weight. Because of these problems, there are concerns that COMEX may not have the gold inventory to back its existing warehouse receipts.

ADVISABILITY: There is no statute preventing the State from investing in gold and silver. The various methods of investment in gold and silver each carry different and often significant risks, the foremost being speculation. As the US has experienced the recent bursts in the housing and tech bubbles, it is important to take caution when contemplating an unconventional investment. Taxpayer money (state funds and state pension) across the US has not typically been used to invest in gold or silver bullion.

Recently, with the uncertainty in global markets, the devaluation of the dollar, rising inflation, and a flat US economy, there has been a renewed interest in either moving back to a gold standard, investing in gold or both. The value of gold and silver has significantly increased in the last decade, meaning it would cost a great deal to invest at this time.

Risks: 1. Bars and coins-South Carolina does not have the capacity to store or funding to secure gold and silver bullion. For these reasons the State Treasurer’s Office does not advise investing in gold and silver bars and coins.

2. ETP’s- The armual expenses and costs associated with this type of investment are high. In recent years there have been issues surrounding gold ETP’s. The purchase price provides the investor with a fluctuating amount (in weight) of the metal. Over time, as value increases and more investors participate in the fund, the amount of metal owner by the investor decreases. ETP’s can also be split and sold on the secondary market. For these reasons the State Treasurer’s Ofñce does not advise investing in ETP’s for gold and silver.

3. Certificates- Certificates for allocated gold present an accountability problem. Allocated gold certificates are supposed to be correlated with speciñc numbered bars; however, it is difficult to verify whether a bank is improperly allocating a single bar to more than one investor. Also, unallocated gold certificates are a form of fractional reserve banking and do not guarantee an equal exchange for metal in the event of a run on the bank’s gold on deposit. This is in conflict with S.C. Code of Laws 1976 SECTION 11-9-660. For these reasons, the State Treasurer’s Office cannot advise investing in gold and silver certificates.

4. Accounts- Similar to the risks associated with gold and silver certificates, allocated and unallocated metals held in accounts produce similar accountability problems. The strength of the account holder’s claim on metals is subject to the account administrators liabilities, assets, and/or solvency. Per S.C. Code of Laws 1976 SECTION 11-9-660, the State Treasurer’s Office cannot advise investing in gold and silver accounts.

5. Derivatives- Over the last three years, gold futures traded on the New York Commodities Exchange (COMEX) have encountered significant accountability problems. Holders of COMEX gold ñltures have frequently experienced delivery delays of their metals. Once delivered, there have been many reports of inaccurate weights and serial numbers on bars that do not match the holder’s contract. For these reasons the State Treasurer’s Office does not advise investing in gold and silver derivatives.

-

Gold: April 2012

-

Having read the above, it may now be easier to make sense of the sharp price decline for both gold & silver over the past 2 days. Lets now ask some questions. Was the price action due to:

Market forces or Price Suppression in action?

Falling Demand or Naked Short Selling?

Human Traders or High Frequency Traders (HFTs)?

Historically, investors have purchased gold as a hedge against an economic, a political, or a currency crisis. A decline in investment markets, a growing national debt, a weak currency, increasing inflation, military conflicts and social unrest are the most common reasons for investment in gold

Have any of the issues above that formed the rationale for purchasing gold (and silver) been resolved?

Recently, with the uncertainty in global markets, the devaluation of the dollar, rising inflation, and a flat US economy, there has been a renewed interest in either moving back to a gold standard, investing in gold or both.

The mainstream media attributed this week’s sharp price decline to improving economy, low inflation and no imminent QE announcements following the release of the latest FOMC meeting minutes. Given that the above statement was published just 5 weeks before the FOMC minutes, who is lying?

- Developing Stories

12 Apr: Jason Hommel explains what Blythe Masters actually meant by “the underlying client position that we’re hedging”.

11 Apr:

Ted Butler, the pioneer of silver manipulation investigation finally broke his silence over the Blythe Masters denial video clip. By far, this is THE best, most level-headed, objective rebuttal to Masters’ famous words that they are “not running a large directional position”. Read “JPM’s TV appearance” posted at Silverseek.com.

Keiser Report on the same subject. His solution is the Silver Liberation Army (SLA)

-

7 Apr: Mike Maloney on RT discussing gold & silver manipulation, Blythe Masters denial of JPM’s role in price manipulation, “First government admission of price suppression” & High Frequency Sheering. Must Watch!

More Charts: 1-Month, 1-Year, 5-Year, 10-Year

More Charts: 1-Month, 1-Year, 5-Year, 10-Year More Charts: 1-Month, 1-Year, 5-Year, 10-Year

More Charts: 1-Month, 1-Year, 5-Year, 10-Year